The Office of Industrial Economics Industrial Economic Status Report January 2008

Industrial Economic Status

January 2008

Summary

Industrial Index of December 2007

- The production index (with value added) was 186.50, which was 1.5% higher than November 2007 (183.76), and 14.2% higher than December 2006 (163.29).

- The increase in the production index, compared with November 2007, was the result of the following sectors: manufacture of office, accounting and computing machinery (Hard disk drive), manufacture of sugar, manufacture of refined petroleum products, manufacture of malt liquors and malt, and manufacture of knitted and crocheted fabrics and other articles.

- The average capacity utilization rate was 65.99, lower than November 2007 (67.99), but higher than December 2006 (64.16).

Industrial Economic Situation in January 2008

- Textile and Garments Industry

o Production and exports should rise from last month due to the stimulation of domestic manufacturers who have adjusted their production by focusing on the higher quality production in correspondence to the needs and usability of each product. o The utilization of more advanced technologies in production, such as technical and functional textiles, especially in the Asian markets. o Garment exports should continue to expand to EU markets due to demand for high quality and skillfully crafted products which Thai manufacturers are competent in producing.

- Cement Industry

o For January and February 2008, the production and domestic sales of cement are expected to increase due to the beginning of the construction season together with the recovery of confidence in consumption and investment after the election. o However, rising oil prices are a critical variable which could affect the recovery of the real estate sector.

Page 1 of 18 The Office of Industrial Economics Industrial Economic Status Report January 2008

o It is estimated that exports will increase because of demand from countries in ASEAN, South Asia, Middle East, Europe, Latin America, and Africa even though demand from America has slowed down.

- Electrical and Electronics Industry

o The production of electrical appliances in January should increase slightly by 3.0% due to increases of major products for export to the EU such as air-conditioners and refrigerators. o However, colored television exports should decrease because America, which was Thailand’s major market of this product, has withdrawn Thailand’s GSP (Generalized System of Preferences) status until June 2008; therefore, purchase orders have declined.

Summary

Industrial Index of Quarter 4, 2007

Production Index (with value added)

For the 4th quarter of 2007 (Q4/2007), the production index was 184.0, 5.3% higher than the figure (174.7) for the previous quarter (Q3/2007), and was 12.8% higher than the figure (163.1) for the 4th quarter of 2006 (Q4/2006).

Main industries that caused the index to increase from the previous quarter were manufacture of office, accounting and computing machinery (HDD); manufacture of malt liquors and malt (Beer); and manufacture of motor vehicles.

Main industries that increased compared with Q4/2006 were manufacture of office, accounting and computing machinery (HDD); manufacture of motor vehicles; and manufacture of electronic valves and tubes and electronic components.

The average production index of 2007 increased by 8.1% compared with last year. The industries which caused the increase in the production index were manufacture of office, accounting and computing (HDD); manufacture of sugar; and manufacture of electronic valves and tubes and electronic components.

Page 2 of 18 The Office of Industrial Economics Industrial Economic Status Report January 2008

Capacity Utilization Rate

Regarding the state of industrial production, the capacity utilization rate during Q4/2007 was 67.3, higher than the previous quarter (Q3/2007) which was 66.9, and higher than Q4/2006 (65.5).

Manufacture of motor vehicles, manufacture of basic chemicals, except fertilizers and nitrogen compounds, and manufacture of office, accounting and computing machinery (HDD); and processing and preserving of fruit and vegetables were the main industries that caused the quarter- on-quarter increase.

Compared with the same quarter of the previous year (Q4/2006), manufacture of motor vehicles; manufacture of office, accounting and computing machinery (HDD); and manufacture of basic chemicals, except fertilizers and nitrogen compounds were the main industries that caused the capacity utilization rate to increase.

The average capacity utilization rate of 2007 was 66.1, lower than of 2006 (67.7). The decline in average capacity utilization rate was caused by preparation and spinning of textile fibers, weaving of textiles; manufacture of refined petroleum products; and manufacture of television and radio receivers and related items.

Page 3 of 18 The Office of Industrial Economics Industrial Economic Status Report January 2008

Industrial Economic Situation

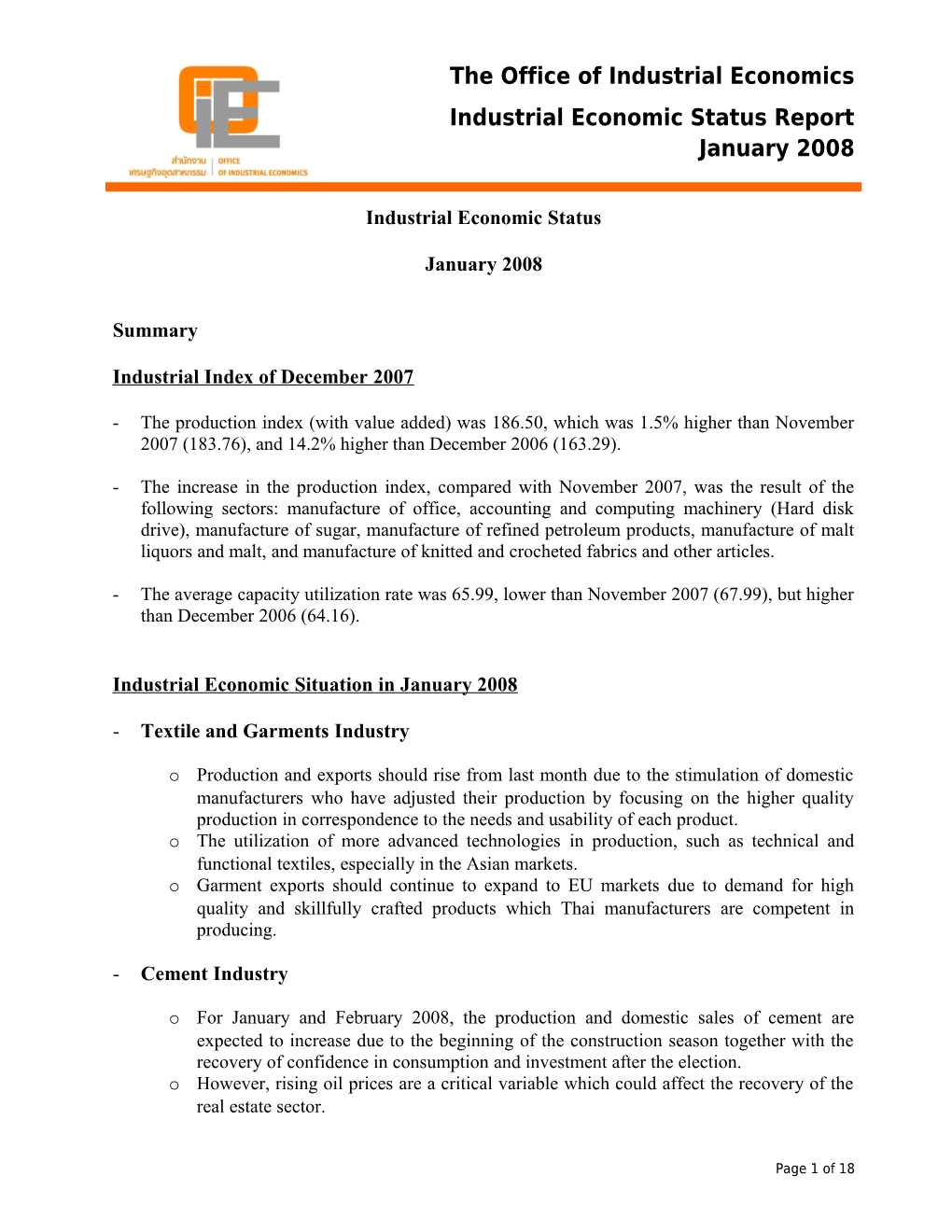

Manufacturing Industrial Index - Manufacturing Production Index 190 (weighted with value added) 185 180 November 2007 = 183.76 175 December 2007 = 186.50 170 165 Main industries that caused the index to 160 increase include: 155 150 o Office, accounting and computing machinery (Hard disk drive) o Sugar o Refined petroleum products

Capacity Utilization Rate - Average Capacity Utilization Rate 70 69 November 2007 = 67.99 68 67 66 December 2007 = 65.99 65 64 Main industries that caused the index to 63 decrease include: 62 61 o Motor vehicles 60 o Preparation and spinning of textile fibers; weaving of textiles o Plastic products

Page 4 of 18 The Office of Industrial Economics Industrial Economic Status Report January 2008

I. Food Industry 1. Production

Overall production (not including sugar) Production and exports of the food in December 2007 increased by 0.1% y- industry in January 2008 should continue to o-y and 4.2% m-o-m. grow from last month. Domestic sales should Products mainly for export, such as decline due to rising product prices. canned tuna, decreased by 14.0% compared with last year and last month due to the strength of the baht and raw material shortages. Production Volume of Major Food Industry Products Products for domestic sales, such as soybean oil and palm oil decreased their T o n s production by 37.6% and 11.8%, m-o-m, 14 0 ,0 0 0 respectively, due to lower raw material 12 0 ,0 0 0 D e c - 0 6 N o v - 0 7 costs and higher demand before price 10 0 ,0 0 0 D e c - 0 7 adjustments. 8 0 ,0 0 0 For sugar, the production volume during 6 0 ,0 0 0 the beginning of the extracting season 4 0 ,0 0 0 increased by 21.1% y-o-y, in accordance 2 0 ,0 0 0 with an increase in raw materials. 0 2. Marketing

1) Domestic Markets

The sales volume of food and Export Major Products of Food Industry agricultural products in December 2007 increased by 4.3% y-o-y due to M i l l i o n ฿ 6 , 0 0 0 an increase in spending as a result of 5 , 0 0 0 1 2 / 0 6 political clarity and the news of rising 4 , 0 0 0 1 1 / 0 7 1 2 / 0 7 product prices which caused 3 , 0 0 0 consumers to spend more for products

2 , 0 0 0 before prices were adjusted.

1 , 0 0 0 2) Overseas Markets 0 The overall export value of the food industry (not including sugar) increased by 19.2% y-o-y; but slowed down by 1.2% m-o-m due to the increased volume in purchase orders. Canned pineapple, canned tuna, and

Page 5 of 18 The Office of Industrial Economics Industrial Economic Status Report January 2008

processed chicken increased by 52.6%, 51.6%, and 41.5%, respectively, compared with last year. However, the strength of the baht and trade barriers caused the export value of other products to decline, such as refrigerated and frozen shrimp, which decreased by 9.0% y-o-y.

3. Trends

It is predicted that production and exports should increase due to a higher volume of purchase orders. Domestic sales should be sluggish due to rising product prices.

Page 6 of 18 The Office of Industrial Economics Industrial Economic Status Report January 2008

II. Textile and Garment Industry 1. Production

…stimulate domestic manufacturers Textile production in December 2007 to adjust their production by focusing on increased by 3.1% m-o-m, and by 6.7% higher quality products and use of more y-o-y, especially synthetic fibers which advanced technologies in production, were needed in Asian markets. such as technical and functional textiles, Production of garments made from which are in demand, especially in the knitted fabric increased by 5.3% and Asian markets… 15.2% compared with last month and last year, respectively. However, production of garments made from woven fabric slightly decreased by 1.7% m-o-m, and Thousan 2.9% y-o-y as a result of the strength of d Pieces Production Volume of Garments (Woven Fabric) 18,00 the baht and the sluggishness of the major 0 16,00 market (America). 0 14,00 0 12,00 2. Marketing 0 10,00 0 8,00 2006 0 Textile and garment products for 6,00 2007 0 domestic sales slowed down compared 4,00 0 with last month. 2,00 0 Exports of most textile products in 0 Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec December 2007 decreased in major markets. American, ASEAN, and Japanese markets dropped by 7.0%, 9.6%, and 5.3%, respectively. Except in the EU markets, garment exports increased by 8.9% m-o-m.

Export Value of Garments 3. Trends 3,5 00 3,0 Jan-Dec 06 00 Jan-Dec 07 Production and exports were expected to 2,5 00 increase from last month due to 2,0 00 stimulation to domestic companies to 1,5 00 adjust their production by focusing on 1,0 00 higher quality products in accordance 50 0 with the demand and usability of each 0 product. Moreover, more advanced Garments Fabrics Synthetic Home Synthetic Other Other Filament Fabrics Fibers Fabrics Textiles production technologies, such as technical Yarns and functional textiles, should be used covering 12 sectors, namely Mobitech, Indutech, Sportech. Garment exports

Page 7 of 18 The Office of Industrial Economics Industrial Economic Status Report January 2008 should continue to grow in EU markets due to demand for high quality and skillfully made products, which Thai companies are competent at producing.

Page 8 of 18 The Office of Industrial Economics Industrial Economic Status Report January 2008

III. Iron and Steel Industry Vietnam, Brazil, Russia, India, etc. Therefore, the volume of semi-finished products decreased, which caused metal Vietnam’s finished steel prices in the world market to increase; consumption in 2007 grew 43% due to the Thai manufacturers, consequently, did not increase of domestic demand as a result of have high volumes of raw materials in foreign investment and the expansion of stock. Flat steel increased in production basic construction projects. by 2.72%. Zinc plates decreased the most by 16.59%; followed by hot-rolled structural coil, which decreased by 16.07% due to one manufacturer reducing Metal Price ($)* its production from last month. Compared with last year, long steel production $700 increased by 12.98%, led by wire rod and Billet $650 wire, which increased by 51.20% and 32.68%, respectively. Flat steel $600 Rebar production increased by 12.0%. Cold- $550 rolled coil increased by 56.92%; and tin Slab $500 plates increased by 40.63%.

HR Coil $450 2. Metal Prices $400 CR Coil $350 The average change in the FOB price in the CIS market at the Black Sea Port in January 2008 of major products increased *CIS Black Sea over last month. The price of billet increased by 11.74%, from US$ 536 to US$ 599 per ton. The price of steel bar increased by 10.87%, from US$ 575 to 1. Production US$ 638 per ton. However, the price of billet in ASEAN markets was US$ 705- The production index in December 2007 710 as a result of the limited product was 139.40, a decrease of 5.83%, m-o-m. volume in the CIS market and high Long steel production decreased by demand in addition to Vietnam agreeing 8.88%, led by wire, wire rod, and pre- to buy at a high price. The price of cold- stressed concrete wire, which decreased rolled coil increased by 4.45%, from US$ by 22.85%, 9.48%, and 8.07%, 637 to US$ 665 per ton. The price of slab respectively due to the decline in increased by 2.83%, from US$ 537 to domestic demand. The raw material price US$ 552 per ton. But the price of hot- of billet increased as a result of Chinese rolled coil decreased by 0.28%, from US$ export tariff rates and the increasing 592 to US$ 590 per ton. demand from the construction sectors in

Page 9 of 18 The Office of Industrial Economics Industrial Economic Status Report January 2008

3. Trends

Long steel production in January 2008 should be stable due to the unchanged situation in the real estate sector. Flat steel is expected to grow slightly due to the demand of global markets, which should cause purchase orders to increase; while domestic demand should be unchanged.

Page 10 of 18 The Office of Industrial Economics Industrial Economic Status Report January 2008

IV. Automobile Industry increase from the previous month by 11.48%.

- Automobile exports were 68,313 Monthly Volume of Automobile Industry units, 24.44% higher than the 54,896 Units units exported in December 2006 due 140,000 to exports of PPV (Passenger Pickup 120,000 Vehicles) to countries in the Asian region; but 2.11% lower than in 100,000 November 2007.

80,000 - The automobile industry in January 60,000 2008 is expected to slow down m-o- m. Sales in January 2008 will be 40,000 broken down into 45% for domestic

20,000 sales and 55% for exports.

0

6 6 7 7 7 7 7 7 7 7 7 7 7 7 -0 -0 -0 -0 -0 -0 0 -0 l-0 -0 -0 t-0 -0 -0 v c n b r pr y- n u g p c v c o e a e a A a u J u e O o e N D J F M M J A S N D

Sales Export Production

Automobiles

In December 2007, the automobile industry grew year-on-year due to exports. However, domestic sales slowed down. Information for the automotive industry in December is as follows:

- Automobile production in December 2007 was 105,024 units, a 14.47% increase from the 91,751 units in December 2006; but a decrease of 16.03% from last month.

- Sales in December 2007 were 64,346 units, a 23.87% decrease, from 84,521 units in December 2006, especially for small passenger cars, but an

Page 11 of 18 The Office of Industrial Economics Industrial Economic Status Report January 2008

- Motorcycle sales were 103,218 units, 36.75% lower than the 163,197 units sold in December 2006, and 20.36% lower than those sold in November Monthly Volume of Motorcycles Units 2007. 180,000 - Motorcycle exports (CBU) increased 160,000 by 105.89% to 9,747 units from 4,734 140,000 units exported in December 2006, and

120,000 were 37.83% higher than the number of units exported in November 2007. 100,000 The increase was caused by sluggish 80,000 exports of existing models in order to

60,000 prepare new models which meet the European quality standards for new 40,000 products. The export markets which 20,000 had high expansions rate were the 0 Canadian, Vietnamese, and Greek markets. 6 6 7 7 7 7 7 7 7 7 7 7 7 0 0 0 0 0 -0 07 0 0 0 0 -0 0 0 - c- n- - r- r - n- l- - - t - c- v e a eb a p y u u ug ep c ov e o D J F M A a J J A S O D N M N - The trend for January 2008 was Sales Export Production expected to slow down when compared to December 2007. Motorcycles

Motorcycle production in December 2007 slowed down, y-o-y, due to a slowdown in domestic sales; however, exports expanded. The information for the motorcycle industry in December is as follows:

- Motorcycle production of 133,039 units in December 2007 was 12.81% lower than the 152,582 units produced in December 2006, and 4.29% lower than the amount produced in November 2007.

Page 12 of 18 The Office of Industrial Economics Industrial Economic Status Report January 2008

V. Cement Industry 1. Domestic Production and Sales

“Domestic production and sales declined The volume of cement production and due to the sluggishness of the real estate domestic sales, which declined for the sector. Domestic demand in cement should fourth consecutive month, in December increase after the election. However, rising 2007 slowed down m-o-m, by 2.10% and oil prices are a critical variable in the 9.57%, respectively. Production and recovery of the real estate sector.” domestic sales decreased by 12.03% and 20.00%, respectively compared with last year. The decline was due to the Production Volume of slowdown of the real estate sector in Million Cement Tons 8 accordance with the sluggishness of consumption and investment. 6

4 2. Exports 2

0 Mont The value of cement exports in Jan Feb Mar Apr May Jun Jul Aug Sep h Oct Nov Dec 2007 December 2007 decreased by 13.42% m- 2006 o-m, due to the exchange rate which Source: Industrial Economics Information Center, Office of Industry Economics caused exports to decline; but that figure increased by 21.13% y-o-y. Domestic Sales Volume of Million Tons Cement 4 3. Trends 3 2 For January and February 2008, it is

1 expected that production and domestic

- sales will increase due to the Month Jan Feb Mar A pr May Jun Jul Aug Sep Oct construction season and the recovery of 200 Nov Dec 200 confidence in consumption and 6 7 Source: Industrial Economics Information Center, Office of Industry investment after the election. However, Economics rising oil prices are a critical variable

Export Value of which could affect the recovery of the Million Baht Cement real estate sector. It is estimated that 2,800 2,400 exports will increase. Although demand 2,000 in America slowed down, demand from 1,600 1,200 neighboring countries in ASEAN and 800 South Asia, including countries from the 400 - Middle East, Europe, Latin America, and Month Jan Feb Mar A pr May Jun Jul Aug Sep Oct Africa continued to grow. 200 Nov Dec 200 6 7 Source: Information and Communications Technologies Center, Department of Trade Negotiations, Ministry of Commerce

Page 13 of 18 The Office of Industrial Economics Industrial Economic Status Report January 2008

VI. Electrical and Electronics Industry Electrical and electronics production in December 2007 increased by 6.39% m- Electrical and electronics production o-m, and increased by 34.39% y-o-y, in December 2007 increased by 34.39%, with the production index at 354.98, as a y-o-y, as a result of a 39.65% increase result of a 39.65% increase in of the electronics production index, electronics. The products that caused the mainly due to HDDs, other ICs, and increase were mainly HDDs, other ICs, semiconductor devices and transistors. and semiconductor devices transistors. The export value of electrical The electronics index was 512.88, which appliances and electronics in December increased by 8.52%, m-o-m, and by 2007 increased by 0.04%, m-o-m, with a 39.65%, y-o-y. The increase was caused total value of USD 4,094.48 million, by HDDs and ICs which increased by and increased by 17.48% y-o-y. The 44.52% and 33.37%, respectively due to highest export value of electrical the high demand of technological appliances was computer components products in global markets. Prices and ICs, which increased by 17.04% dropped quickly due to high competition and 11.35%, respectively. and the fast pace of technology. Therefore, manufacturers offered more Production Index of Electronics & Electrical variety and multiple functions in one unit Appliances to increase prices. 400 2. Marketing 300 2007 2006 200 2005 The export value of electrical appliances 100 2004 and electronics in December 2007 increased by 0.04% m-o-m, and 0 l t r r c b n n g p

y v increased by 17.48% y-o-y, with a total u c a p e e u u e a a o J A O J J F M A S D N M value of USD 4,094.48 million. The highest export value, worth USD 187.31 Table 1 Top electrical appliances and electronic products exports in December 2007 million, in electrical appliances came from air-conditioners for residences and Unit: Million US$ Electrical appliances & Value CPM CPY factories; followed by circuit protection, Electronic products including control board, which totaled Computer products 1,531.86 -2.93 17.04 USD 141.41 million. ICs 688.00 8.43 11.35 While the highest export value of Air-conditioners 183.82 1.90 22.16 electronics in December 2007 declined Electrical appliances 141.41 3.93 15.47 Total of Electrical 4,094.48 0.04 17.48 0.55% m-o-m, it increased by 15.83% y- appliances & Electronic o-y, with a total value of USD 2,681.42 products million due to increases from computer Source: The Customs Department 1. Production components and ICs, with a total value

Page 14 of 18 The Office of Industrial Economics Industrial Economic Status Report January 2008

of USD 1,531.86 million and USD 688 million, respectively.

3. Trends

Electrical appliances production in January 2008 should increase due to a 34.16% increase of electronic products, including a 25.22% increase in HDDs. The growth rate slowed down due to the economic sluggishness of the sector’s major market, America.

Page 15 of 18 The Office of Industrial Economics Industrial Economic Status Report January 2008

The production index (with value added) for December 2007 was 186.50, 1.5% higher than in November 2007 (183.76), and 14.2% higher than the figure (163.29) for December 2006.

o The main industries that caused the manufacturing production index to increase were manufacture of office, accounting and computing machinery (Hard disk drive), manufacture of sugar, manufacture of refined petroleum products, manufacture of malt liquors and malt (Beer), and manufacture of knitted and crocheted fabrics and other articles.

o The main industries that caused the manufacturing production index to increase year- on-year were manufacture of office, accounting and computing machinery (Hard disk drive), manufacture of motor vehicles, manufacture of electronic valves and tubes and other electronic components, processing and preserving of fish and fish products, and manufacture of sugar.

The capacity utilization rate for December 2007 was 65.99, which was lower than in November 2007 (67.99), but higher than in December 2006 (64.16).

o The main industries that caused the capacity utilization rate to decrease from November 2007 were manufacture of motor vehicles, preparation and spinning of textile fibers; weaving of textiles, manufacture of plastic products, manufacture of fabricated metal products, not elsewhere classified (n.e.c), and manufacture of footwear.

o The main industries that caused the capacity utilization rate to decrease from December 2006 were manufacture of motor vehicles, manufacture of office, accounting and computing machinery, processing and preserving of fish and fish products, manufacture of basic iron and steel, and manufacture of plastic pellets.

Industrial activity in December 2007

The Department of Industrial Works (DIW) report from December 2007 recorded 227 start-up plants. This was -18.53% lower than the 340 start-up plants in November 2007. Investment capital totaled 9,391.94 million baht, which was -64.46% lower than the 26,422.95 million baht registered in November 2007. There were 6,859 jobs created, which was -51.12% less than the 14,032 jobs created in November 2007.

When compared with December 2006, the number of start-up plants decreased by -16.82% as compared to the number of plants that started operations in December 2006 (333 plants). The number of jobs created was -15.22% lower than the number of jobs created in December

Page 16 of 18 The Office of Industrial Economics Industrial Economic Status Report January 2008

2006 (8,090 jobs). Investment capital increased by 17.50% in comparison to the total investment capital registered in December 2006 (7,993.25 million baht).

o Industries with the most start-up plants in December 2007 were involved in manufacture of digging or dredging the gravels, sand or soil (35 plants), followed by manufacture of household furnishing from wood, rubber, or other non-metal and not of extruded plastic (25 plants).

o The industry whose startups had the highest investment capital in December 2007 was manufacture of producing ethyl alcohol (exclude production from extracted sulfide for pulp mill), with 2,083.70 million baht; followed by manufacture of mixed food or finished food for feeding animals, with 667.30 million baht.

o The industry whose startups created the highest employment in December 2007 was manufacture of apparels, handkerchiefs, neckties, gloves, socks from fabric and leather, with 988 new jobs; followed by manufacture of repairing motor vehicles or parts, with 482 new jobs.

In December 2007, the Department of Industrial Works (DIW) reported 87 plant closures, which were -55.15% lower than the 194 plant closures in November 2007. The December closures reflected 2,029.97 million baht worth of investment capital, lower than the 3,025.61 registered in November 2007. The 4,707 lay-offs were higher than in November 2007 when there were 4,008 lay-offs.

When compared with the records from last year, there were -39.16% fewer plant closures than the 143 closures recorded in December 2006. The number of lay-offs was higher than what was reported in December 2006, which was 3,909 lay-offs, but the value of plant closures was lower than last year, which was 2,217.11 million baht in investment capital.

o The industries with the most plant closures in December 2007 were involved in manufacture of concrete products, mixed concrete, gypsum products and plaster, with a total of 10 plants; followed by manufacture of making tools, utensils, household furnishings or decorations from plastic, and manufacture of repairing motor vehicles or parts, with a total of 6 plants each.

o Closed-down plants having the highest investment capital in December 2007 were involved in manufacture of smelting, melting, casting, rolling, drawing or iron and steel basic industries (935.60 million baht). The 2nd highest investment capital was from manufacture of apparels, handkerchiefs, neckties, gloves, socks from fabric and leather (259.21 million baht).

Page 17 of 18 The Office of Industrial Economics Industrial Economic Status Report January 2008

o Closed-down plants with the highest lay-offs in December 2007 were involved in manufacture of apparels, handkerchiefs, neckties, gloves, socks from fabric and leather (1,928 lays-offs); followed by manufacture of shoes or parts of shoes that are not made of wood, skimmed block rubber, (extruded rubber or plastic) (1,060 lay-offs).

The Office of Board of Investment (BOI) reported that in December 2007 there were 101 investment projects, -12.17% less than the 115 projects recorded in November 2007. The investment capital recorded 78,300 million baht, a decrease of -5.78%, which was less than the 83,100 million baht in November 2007.

BOI investment promotion in December 2007, when compared with the same month of the previous year, resulted in -39.88% less approved investment projects (168), with 15.66% more investment capital (67,700 million baht) than December 2006.

o Shareholder distribution of BOI approved investment projects in January - December 2007 are as shown in the table below.

Share distribution Number of projects Investment capital (million Baht) 100% Thai shareholding 452 220,400 100% Foreign shareholding 479 238,000 Joint venture 411 286,100

o Investment projects approved in Jan-Dec 2007 were mostly in the fields of services and public utilities, with a total investment capital of 191,700 million baht, followed by chemicals, paper, and plastics, with a total investment capital of 175,100 million baht.

Page 18 of 18