Optimizing the First Pillar of the Social Insurance System1 Jon Eivind Kolberg, consultat of the project

Introduction

The coexistence of a remarkably high contribution rate and strikingly low pensions and other social benefits represents a puzzle to anyone trying to understand the present Bulgarian social insurance system. The reasons for this paradox are complex, yet at one level it is possible to argue that the contradiction is the outcome of an utterly unfavorable dependency ratio, a distorted use of resources for social insurance, and a much too low compliance rate. Currently there are 90 pensioners per 100 employed persons The compliance rate is said to amount to 75%, which means that the collection of contributions for the social insurance system does not mobilize one fourth of what is possible.2 Contributions for unemployment insurance and for the national health insurance come on top of this. This illustrates that the situation for the social security system of the country is difficult and serious and that a wide and consistent specter of measures must be mobilized to address the situation.

This paper shall explore five different possibilities for optimizing the first pillar of the mandatory social insurance scheme in Bulgaria. By ``optimizing`` is meant to have more value for money, i.e. maximizing the core concerns of the social insurance scheme in a cost efficient and effective way. The five different measures for maximizing core concerns while paying due attention to economic constraints have to do with:

Legal design Contribution collection Cash-flow efficiency Controls Social research

Legal design

The legal design of social insurance programs determine coverage, the level and structure of social insurance contributions, the rules governing eligibility, the number and types of risks being covered, replacement levels, duration, and regulations concerning the behavior of benefit recipients. The legal design, involving not only the legal provisions, but decisions and regulations as well, are of large importance because they have a strong bearing on peoples

1 According to the TORs, the consultant should: (a) Prepare an analysis of social insurance benefits which have effect on the pension system as a whole to the extent these benefits are relevant to the pension reform, including an analysis of the existing short-term employment insurance schemes such as for work accidents, and sickness insurance, and the old age, survivor- and other benefit payments through the first pillar; (b) Propose changes as needed, including an analysis and a proposal of changes for the maternity leave scheme; (c) Provide assistance to the NSSI in rationalizing the administration of the various social security and pension programs, recommending changes to design and implement an efficient and effective first pillar.

2 However, some would say that this is an optimistic estimate. The combined effect of an average replacement rate of for example 30%, and a dependency ratio of 90% results in a contribution rate of (3*90)/100= 27% of payroll. However, this applies in a situation where the compliance rate is 100%. If only 75% of the contributions are collected, the contribution rate would have to be added by 25%= (27*1,25)=33,8%.

1 behavior, and hence on expenditure. Restrictive rules bring about low benefit consumption, and changes towards less program generosity indicates that decision makers want costs to be reduced. Increased program generosity, on the other hand, is assumed to have the opposite effect and is assumed to propel expenditures. We can call this the social policy effect; i.e. the idea that program characteristics affect behavior in a strong way. Two comments are warranted here. The first is that, although program characteristics are undeniably significant, they are not the only determinants affecting social security related behavior. Other factors are economic cycles and structural circumstances, working conditions, wage levels, as well as political and cultural determinants. The second comment is that social insurance are not necessarily either fully generous, or uniquely and one-dimensionally restrictive. Several program characteristics can be defined in different ways, bringing about packages of generosity and restriction. Many decision-makers are quite conscious about this, for example when they combine a general rule of full wage compensation in the case of sickness with employer periods, restriction on duration, or waiting days, or the other way around: for example 75% wage compensation, but with few other constraints.

Contribution collection

The issue of contribution collection speaks to the revenue side of the social insurance system. Any given formula for revenue mobilization can be applied more or less forcefully and efficiently. As will be demonstrated, the contribution collection process for the mandatory social insurance scheme in the country can be improved in several different ways, producing revenue increases for the program. In the final analysis, the implementation of the social insurance scheme will depend on the economic development of Bulgaria. Yet, the compliance rate is also of vital importance. There are possibilities for revenue enhancement within the constraints of economic circumstances. These possibilities have to do with both the application of instruments and measures on the one hand side, and with organizational solutions on the other side. The paper will present and discuss the plans for a new unified revenue collection agency which joins the efforts of the General Tax Administration and the NSSI, and it will present a series of ideas to promote collection efficiency, irrespective of organizational solution.

Cash-Flow Efficiency

What happens with the money after collection and up to the point of delivery of payment turns up to be important as well. Today the money is physically moved from the employers who pay both employer- and employee contributions through a series of banks to NSSI bank connection in Sofia and back again to the Postal Office for delivery to the pension and cash- benefit recipients. This process takes time, it is expensive, and the current system makes for little flexibility towards the recipients, and is inefficient in terms of asset accumulation. The improvement of the cash flow process holds promises both for better service vis-a-vis the recipients, for expenditure reductions, and for additions to capital accumulation. The paper will present, explain, and discuss a concrete proposal for the simplification and advancement of the cash flow process.

Controls

2 Optimizing a social insurance system also implies ensuring that those who qualify for benefit receive it and that those who do not will not have benefits. However, controls also mean that nobody appropriates money for improper use, i.e., in violation of the rules of the program. One type of improper use is when money for sickness insurance is claimed on behalf of somebody who is not sick. Such improper use is caused by the fact that employers both pay contributions and can reclaim money paid when they have sick employees without the interference of the NSSI. It is argued that such practices constitute a major source of fraud, yet the argument is not substantiated by solid and systematic empirical research. However, the door is open for irregular practices through the mechanisms being applied, and both the IMF and the World Bank have argued strongly in favor of closing the door of fraud and establish new forms of controls to replace existing and substandard instruments. The paper presents, explains, and discusses four possibilities for changes in the system of controls:

Moving the short term sickness benefits from the NSSI to the NHIF Establishing 3 waiting days and expanding the employer period to 7 days Discontinue the option for employers to reclaim contributions paid for sickness insurance and establish controls at new points of payment in the NSSI Combining the second and third alternatives, and adding a certain number of waiting days

Social Research

Social research is the last of the five contributions towards optimizing the first pillar of the mandatory social assistance scheme in Bulgaria. Informed policy analysis and formulation must rest on solid empirical evidence based on inter-subjective and reproducible methods of social science. This means for one thing that the policy process is seen as a continuous process, where programs are adapted and modified based on correct information about their performance and financial assumptions. A legislative process is much more than the law and the paragraphs. It contains the decisions of the Council of Ministers and the regulations of the NSSI in addition to amendments to the law enacted by the Parliament. The papers contains a presentation of two, we believe important, examples of how social research can contribute in a productive way to a better understanding and to the improvement of social insurance policies. It argues for strengthening the Department for Analysis.

Review and Analysis of Short-term Benefits

Sickness Absence

The menu of short-term benefits offered by the Mandatory Social Insurance Code in connection with sickness is linked to the concept of temporary work incapacity. Such temporary work incapacity is compensated by the social insurance scheme when it is caused by own sickness, or by the sickness of family members. In addition, health authorities can impose sickness absence by quarantine or prescribe the suspension of work activities. Absence from work and domestic presence is compensated through short-term benefits when the sickness, caring needs, or treatment programs of family members dictate such presence.

Eligibility: According to the Mandatory Social Insurance Code, entitlement to short-term benefits in connection with temporary work incapacity requires 6 months of social insurance

3 participation. However, periods of unpaid leave recognized as service as well as childcare leave are counted and included in the qualifying period.3 The average daily minimum wage for the respective period is applied when non-wage participation is included in the qualifying period.4 The eligibility condition of half a year does not apply to temporary incapacity related to work injury.5 Qualifying for short-term benefit is hence easier when the sickness can be traced to a specific location or circumstance. No work- or participation requirements exist in these cases. The same applies to insured persons who have been under quarantine or prescribed job suspension. Eligibility for short-term benefit in connection with temporary incapacity does not stop with the termination of the work contract. The right to short-term benefit remains if the incapacity occurs within 2 months following the termination of the work contract, but the duration of payment is restricted to 75 days in such cases.6 This means in other words that the receipt of short-benefit can extend up 4 1/2 months after the work contract is finished.

Waiting days: Many schemes for short-term benefits in other countries operate with a limited number waiting days to decrease the relative attraction of non-work, and hence as a disincentive mechanism with respect to the consumption of the benefit in question. However, the Bulgarian Mandatory Social Insurance Code is granting short-term benefit in connection with sickness leave from the first day of income loss.7

Employer period: The new Mandatory Social Insurance Code has introduced an employer period of 3 days with regard to cash benefits for sickness absence due to temporary work incapacity during which the employer pays wage continuation.8 In some sickness insurance schemes such employer periods are inserted as a mechanism for reducing sickness absence. It is claimed that employer periods will increase the employer's interest in developing a healthy work environment and in controlling misuse. By international comparison, an employer period of 3 days must be considered as short.

Wage replacement/Compensation: The replacement level for short-term work incapacity due to general sickness is compensated at 80%. The level of compensation in the case of work injury and occupational sickness is 90%. In the case of labor readjustment due to health reasons, all reduction of (averaged) income is compensated.9

Suspension: The short-term cash benefits for temporary incapacity can be suspended for certain periods if the insured person deliberately damages his/her health in order to obtain benefit, or violates the treatment regime determined by the health service. Thus, benefits can be suspended for up to 15 days per year if the insured person has lost working capacity due to substances not prescribed by the medical experts such as alcohol, or due to misdemeanor and other actions violating the public order. And they can be cut by up to 3 days if he/she has lost working capacity due to failure to comply with prescribed labor safety rules.

3 See Mandatory Social Insurance Code, Part I, Chapter 1, Article 10, item 2 4 Regulations concerning wage replacement for temporary incapacity in relation to sickness are included in op. cit, Article 41 5 See op. cit.,Chapter 4, Article 40, item 1 6 See ibid., Chapter 4, Article 42, item 2 7 See op. cit.cit, item 1. 8 See ibid, Chapter 4, Article 40, item 4. 9 See op. cit, Article 47, items 1 & 2.

4 Duration: The rules governing the duration of the different short-term sickness benefits in relation to sickness are summarized below:

Synopsis 1: Rules governing current short-term sickness benefits

Item General provision Maximum duration Sickness absence of insured Until working capacity is re- No limitation with regard to person stored or permanent in-capacity duration; i.e. until recovery or substantiated certification of permanent work incapacity Sickness absence of insured Right continues up until 2 75 days person after job termination months after termination of job contract Job suspension Imposed by health authorities 90 days per calendar year Sickness of family member(s) Care, & escorting to treatment Max. 10 days/year per insured above 18 years family Sickness of family members(s) Care, & escort to treatment Max. 60 days/year per insured below 18 years family Quarantine Imposed by health authorities Duration of the quarantine Labor readjustment due to sick- Difference between old and new 6 calendar months ness wage

Organization: The law stipulates that short-term cash benefits related to temporary work in- capacity in connection with sickness shall be paid through the employers as the insurers, and - as already mentioned - the three first days shall be paid at the account of the employer. In practical terms this means that the employers are allowed to withdraw money from their social insurance account in the bank in order to pay for short-term benefits related to tempo- rary incapacity. The controls of these procedures take place through periodical post-hoc inspections in which assigned inspectors are supposed to audit the appropriate documents relevant for the respective cases. New methods of immediate controls are about to be introduced along with the development of a computerized information system for the NSSI in which the activities of enterprises and individuals can be better identified and described.

Payment schedule: Sickness benefits are paid on a 5-day weekly basis, i.e. actual (potential) working days are compensated.

Two different social insurance funds are providing income maintenance/compensation for temporary incapacity due to sickness in Bulgaria. These funds are:

The Work Injury and Occupational Sickness Fund, and The General Sickness and Maternity Fund

The differences between the funds pertain to the 3 important dimensions: (i) the qualification period for benefit eligibility, (ii) the replacement rate, and (iii) the foreseen cost-shifting between employers and employees.

5 Synopsis 2: Comparison between the Fund for Work Injury and Occupa- tional Sickness and the General Sickness and Maternity Fund

Dimension Fund for Work Injury & General Sickness and Ma- Occupational Sickness ternity Fund Qualification period None10 6 months11 Replacement rate 90% 80% Cost-shifting Not foreseen; employer pays Employee contributions shall 100% of contributions12 increase from 0% in 1999 to 50% in 2007

Below follows a set of 6 different principles to guide potential changes/modifications of the legal design of a scheme for short-term sickness absence. These principles are:

Compatibility with economic level Transparency Promotion of work incentives Contribution to healthy working conditions Connection between contributions and benefits Optimal benefit duration

Although it is difficult to derive a definite course of action based on the first principle, it is nevertheless evident that a public program for income maintenance during sickness must be compatible with the economic level of a country. Compensation levels of 80-90% with few if any controls may seem too generous for a transition economy like the Bulgarian. It is difficult to see why the level of wage compensation should be higher for identical work incapacity depending upon the circumstances or location of the sickness. It is furthermore difficult to understand why the employers should continue to pay all contributions for sickness insurance in this scheme, whereas cost shifting is foreseen in the general sickness and maternity scheme. The existence of two separate funds with different rules covering the same type of risk is difficult to justify and comprehend. Most, if not all sickness insurance schemes have pro- visions to protect the work ethic and thus making it less attractive to receive short-term sick- ness benefit than to engage in paid work. Several instruments can be applied. The most common is the replacement level, but others are often used in addition, such as waiting days and an employer period. Sickness absence is not only a function of program characteristics. The character of working conditions is important as well. Some industries and occupations are more dangerous and prone to ``produce`` sickness than others. It is therefore crucial to design the program in such a way that the interest of employers in improving working conditions is encouraged, and ways are found to distribute the burden of paying for sickness benefits across industries and occupations. The logic of social insurance is risk sharing. However, it is also

10 See Mandatory Social Insurance Code, Article 40, item 2. 11 See op. cit., item 1 12 See ibid., Article 6, item 3.4

6 true that social insurance presupposes a certain, if not perfect correspondence between contributions and benefits. Synopsis 3: Redesigning the Programs for Sickness Absence

Principle Problem Approach Suggested solutions

1 Compatibility with Costs unsustainable in the Reduce generosity See below economic level medium to longer term 2 Transparency Two programs with differ- Make one scheme Discontinue separate fund for ent rules covering identical based on General Work Injury and Occupational risks Sickness & Ma- Sickness ternity fund 3 Work incentives Current instruments for Insert mechanisms to 1. Establish replacement @ upholding work incentives advance work in- 75% throughout the too weak centives scheme 2. Introduce 3 waiting days 3. Expand the employer period to 7 days

4 Working conditions Insufficient promotion of Develop instruments 1. Expand the employer good working conditions to sustain good period to 7 days through the short term working conditions 2. Link level of employer benefits contributions to verified performance 3. Establish small fund for equalization purposes 5 Relation between con- Link is too weak in the Strengthen link Restrict qualifying periods to tributions and benefits national context periods of actual paid work 6 Duration Benefit duration is unre- Shorten benefit du- Encourage active cure and stricted ration rehabilitation be limiting benefit period to maximum 52 weeks

It can be argued that this link is too weak in the Bulgarian case. Thus, there is a qualifying period of 6 months, which might seem quite long. However, it should be observed that periods of non-paid work are favorably counted and included. This may seem too generous under present circumstances. The last issue concerns the optimal duration of sickness leaves. The duration as of today is until recovery or permanent disability is substantiated. This is easy to understand, yet a maximum duration may spur active cure and rehabilitation. Sickness absence programs should not be allowed to justify or legitimize inaction.

These principles and considerations are included in Synopsis 3 above. The recommendations for changes in the legal design are spelled out in the right hand column. A final observation is that the regulations in regard to caring for, and escorting sick family members speak to the warm hearted social concerns that are included in the social insurance legislation. Similar extensions of sickness absence programs are relatively new among the pioneers of social legislation in the rest of Europe.

Maternity and Child Related Benefits

7 Bulgarian social policy provisions for child bearing and rearing are quite extensive. They are described in two bodies of legislation: The Mandatory Social Insurance Code, adopted on December 2, 1999 and published by the State Gazette #110 on December 17, 1999 The Decree on Birth Stimulation, promulgated by the State Gazette #15 on February 23, 1968

The following six benefits are included, the four first of which are contained in the Mandatory Social Insurance Code:

1. Benefits for Labor Readjustment due to Pregnancy or Breast Feeding13 2. Benefits for Pregnancy and Birth Giving14 3. Benefits for the Care of a Small Child15 4. Benefits when the Additional Paid Leave for Care of a Small Child is not Used16 5. Birth-Grant17 6. Monthly child allowances18

These programs are outlined in terms of the following four different dimensions in Synopsis 4 below:

Qualifications General provision(s) Replacement Duration

The assessment of a scheme for maternity benefits - comprising such programs as maternity benefits, and cash benefits in relation to birth-giving, care for small children and child allowances for the compensation of the extra costs of having children - may rest of several criteria. The following assessment applies three main criteria: (i) simplicity & duplication; (ii) the insurance character of the benefits, and (iii) pro- natalist concerns. First programs should be simple and easy to understand, and they should not overlap.It should secondly be clear and logical which of the programs belong to the world of social insurance, and which ones are government programs that should be funded as any other item of public budgets. This criterion

13 The Mandatory Social Insurance Code, Chapter 4, Part II, Article 48 14 Op. cit., Articles 49-50. Included here are also benefits in the Case of Death or Sickness of the Mother (Article 51, as well as Benefits for Pregnancy and Birth Giving in Case of Termination of the Insurance (Article 52) 15 See ibid., Article 53. 16 See ibid., Article 54 17 See Decree on Birth Stimulation, promulgated by the State Gazette #15 on February 23, 1968, Article 1 18 Op. cit., Article 2

8 Synopsis 4: Current legislation with regard to maternity and child related benefits

Benefit General Provision Qualification Replacement Duration Organization 1. Labor Readjust- Compensate loss of 6 month of partici- 100% 6 months NSSI ment due to preg- income due to pation in General nancy or breast change of job Sickness & Mater- feeding nity Fund 2. Pregnancy and Cash benefit in con- See above 90% 135 calendar days NSSI birth giving nection with mater- nity 3. Care of a Small Cash benefit See above Minimum wage 593 calendar days; NSSI Child from expiry of benefit for pregnancy and birth giving until the child is 2 years of age 4. Benefit When the Cash benefit See above 50% of the minimum See above NSSI Additional Paid wage Leave for Care of a Small Child is not Used 5. Birth-Grant Lump-sum Universal entitle- 1st child: one minimum Not applicable MOSP/Decree/Paid by state ment monthly salary; 2nd budget/Operated by the NSSI child: 2 min month sala- ries; 3rd child 2 1/2 min month salaries, 4th and subsequent children: 1 min monthly salary each 6. Child Allowance Wage supplements/ Employees and pen- Monthly allowances: 1st From birth until the MOSP/Decree/Paid by state addition to pensions sion recipients child: 15 leva; 2nd child: child is 16 years of budget/Operated by the NSSI 30 leva; 3rd child: 55 age, or if a student leva; for 4th and subse- supported by parents quent children: 15 leava until the age of 18 for each

9 speaks to the eligibility through actually having carried out the required extent of paid work, as well as to type of income loss. Last, but not least: both demographic context and prospects are relevant in any assessment of child related benefit package. Under present circumstances it is difficult to recommend restrictions in this field. Making it more problematic to have and raise children might have very negative consequences, also in terms of the future of the social insurance system of the country.

The overview shows that the scheme could be improved along these dimensions. The suggested revision and simplification of the scheme is included in Synopsis 5 below.

Synopsis 5: Redesigning the Programs for Maternity and Child Related Benefits

Criterion Problem Solution I. Complexity & 1. Birth grant and Pregnancy & birth giving 1. Restrict birth grant as lump Duplication benefit in the case of employed women sum at birth for non-working 2. Care of Small children & Child Allowance mothers overlap 2. Take program for care of small 3. Different compensation levels for Labor children out of the social in- Readjustment and Pregnancy & birth giv- surance scheme and unify it ing benefit with child allowance at same 4. Benefit awarded when the additional leave benefit rate for care of small children is not used 3. Establish uniform replacement level at 100% of wage loss 4. Discontinue program II. Insurance charac- 1. Care for small children is hardly an in- Discontinue as a NSSI-program but ter of programs surance risk insert into Child Allowance pro- 2. Non-paid work recognized as work in gram relation to qualifying period Reserve Pregnancy & Birth giving 3. The birth grant is universal benefit for women who qualify in terms of paid work Restrict Birth Grant to non-working mothers and discontinue program as social insurance scheme III Pro-natalist con- Disturbingly low fertility rate with potential 1. Maintain duration of Pregnancy cerns future demographic misfortune for social in- and Birth giving benefit and surance raise compensation to 100% 2. Increase Child Allowance with Additional payment for care of small children 1/2-2 years

Analysis of the Pensions of the First Pillar of the Bulgarian Social Insurance Code

10 General overview

The pension scheme of the first pillar of the mandatory social insurance code is described in Chapter 6. The law distinguishes between on the one hand side pensions related to employment as described in Parts I through III, and on the other hand pensions not related to employment (Part IV). The employment related pensions are the most important in terms of number of beneficiaries and expenditure. They include:

Old Age and Length of Service Pension, described in Articles 68 to 70 Disability Pensions outlined in Articles 71 to 79. Survivor Pensions specified in Articles 80 to 84.

The menu of pensions that not being related to employment comprises:

Military Disability Pension spelled out in Articles 85-86 Civil Disability Pension identified in Articles 87-88 Social Pension for Old Age defined in Article 89 Disability Social Pension characterized in Article 90 Special Merit Pension encircled in Article 91 as well as: Individual Pensions explained in Article 92

The Old Age Pension

Description

Entitlement for the employment related old age pension is currently established when a male is 60,5 years of age and provided he has been insured for at least 37,5 years. A woman qualifies at the age of 55,5 years provided she can document participation in the pension system for 32,5 years. However, persons may qualify for old age pension well below the already strikingly low ages of 60,5 and 55,5. Eligibility is dependent both upon a specific (pensionable) age, and on defined length of service. These two requirements are added into a certain defined number of eligibility points, calculated as:

Points = Age + Years of participation

Currently, men need 98 points (60,5+37,5 in the example above), and women need 88 points (55,5+32,5 in the example above) to qualify for old age pension. The years of participation are a core issue here. They are differently calculated for different occupational categories, or differently put: one year of actual work may be more than one year in terms of social insurance participation. Article 104 of the Mandatory Social Insurance Code rules that the workforce shall be divided into 3 occupational categories according to the nature of the working conditions.19 Three years of service for workers belonging to worker category I (for 19 A list of occupations published by the Council of Ministers describes the actual existing jobs in terms of the worker classification in every company of the country. This document covers a total of 80 pages and has not been translated into English. See ``Regulations for Labor Categorization upon Retirement`` first published in 1967, with subsequent amendments; the latest version being promulgated October 23, 1998 and put into effect as from January 2000. Labor category I is meant to cover the most demanding blue collar occupations, such as for example miners, metallurgical work, machine building, metal processing, and construction. But it also contains some surprises, such as pilots, stewardesses, bus- train-, and tram-drivers. Labor category II covers management-

11 example a miner) count as five years of social insurance contribution, and a four year service in worker category II add up to five years of membership. In other words: workers with

Table 1: The minimum pensionable age for the PAYG system in Bulgaria for different categories of workers under the current and planned system. By sex20

Labor Category I Labor Category II Labor Category III Men Age Service length Points Age Service length Points Age Service length Points 2000 52 46 (27,6) 98 57 41 (30,75) 98 60,5 37,5 98 2001 52 47 (28,2) 99 57 42 (31,50) 99 61,0 38,0 99 2002 52 48 (28,8) 100 57 43 (36,00) 100 61,5 38,5 100 2003 52 48 (28,8) 100 57 43 (36,00) 100 62,0 38,0 100 2004 52 48 (28,8) 100 57 43 (36,00) 100 62,5 37,5 100 2005 52 48 (28,8) 100 57 43 (36,00) 100 63,0 37,0 100 2006 52 48 (28,8) 100 57 43 (36,00) 100 63,0 37,0 100 2007 52 48 (28,8) 100 57 43 (36,00) 100 63,0 37,0 100 2008 52 48 (28,8) 100 57 43 (36,00) 100 63,0 37,0 100 2009 52 48 (28,8) 100 57 43 (36,00) 100 63,0 37,0 100 2010 63 48 (28,8) 100 63 37 (27,75) 100 63,0 37,0 100 2011 63 48 (28,8) 100 63 37 (27,75) 100 63,0 37,0 100 Wome Age Service length Points Age Service length Points Age Service length Points n 2000 47 41 (24,6) 88 52 36 (27,00) 88 55,5 32,50 88 2001 47 42 (25,2) 89 52 37 (27,75) 89 56,0 33,00 89 2002 47 43 (25,8) 90 52 38 (28,50) 90 56,5 33,50 980 2003 47 43 (25,8) 90 52 38 (28,50) 90 57,0 33,00 90 2004 47 43 (25,8) 90 52 38 (28,50) 90 57,5 32,50 90 2005 47 44 (26,4) 91 52 39 (29,75) 91 58,0 33,00 91 2006 47 45 (27,0) 92 52 40 (30,00) 92 58,5 33,50 92 2007 47 46 (27,6) 93 52 41 (30,75) 93 59,0 34,00 93 2008 47 47 (28,2) 94 52 42 (31,50) 94 59,5 34,50 94 2009 47 47 (28,2) 94 52 42 (31,50) 94 60,0 34,00 94 2010 60 34 (20,4) 94 60 34 (25,50) 94 60,0 34,00 94 2011 60 34 (20,4) 94 60 34 (25,50) 94 60,0 34,00 94 presumably tougher jobs reach pensionable age or pension rights faster than their nominal years of service/participation would indicate. The current and planned eligibility requirements for the three occupational categories, and for men and women respectively are shown in Table 1 above.

In addition to the differentiated character of regulations with regard to social security partici- pation comes the fact that (formal) non-work is also counted as participation, in a strikingly liberal fashion (Article 10). Important examples of non-work being included as service are un- paid leave for raising a small child, unpaid sickness absence, and unpaid leave for up to 30 days per calendar year.21 supervisory work, and support functions in the difficult industries plus skilled manual work and some blue collar occupations (examples are stone-cutting, crane operators, canteen staff, textile- and shoe production). The large residual of occupations belongs to Labor category III.

20 Figures in parenthesis refer to the adjusted length of service required. 3 years of service count as 5 years in category I, and 4 years of service add up to 5 years in category II. 21 For the full list of non-working periods being recognized as length of participation, see Chapter 1, Article 10, paragraphs 5 through 8 of the Mandatory Social Insurance Code.

12 If a person does not have the required number of points to qualify for the old age pension at ages 55,5, and 60,5 respectively, he/she will nevertheless receive such a pension at the age of 65. The condition is that 15 years of service can be documented, of which a minimum of 12 years must be derived from paid work.22

The mechanism for determining the pension amount includes the following steps: 23

The potential old age pension recipients, i.e. the member of the scheme/the participant each year accrues pension points,24 which is calculated as insured income over average insured income

These annual pension points are averaged when the pension is claimed

Previous year's income is multiplied by the averaged pension points and the pensioner will receive 1% of this sum for each year of social insurance participation. Thus, a person who has worked 40 years will receive 40% of the last year's income times the individual co- efficient

If the old age pensioner continues to work after receipt of the pension, and many do, he/she will continue accumulating new pension points, and the pension will consequently have to be recalculated.

It is estimated that the fraction of working pensioners today constitutes roughly 15%-20% of all pensioners.25 Three different mechanisms have been used in the period 1992-1995 for the regulation of the relationship between the receipt of pension benefits while at the same time having earned income:

The first of these was in effect from 1992-1995. It reduced the pension with 35% against earned income. Thus, if the pension was 35 leva and the salary 100 leva, the pension would be taken away.

The second mechanism, in place from 1995-1997, established a floor of two times the minimum wage. Earnings up to this amount did not affect the pension. The pension was reduced leva by leva for earned income above this floor. With a minimum wage of 75 leva, and thus a ``free amount`` of 150 leva, plus a pension of 35 leva, the pension would be taken away at a salary of 185 leva.

The third solution to the issue of the working pensioners was to do away with the work test. This approach was initiated after the decision of the Constitutional Court in 1997, which ruled that restrictions on the right to employment were unconstitutional. The Court stressed that pension benefits represented earned rights Consequently, no work test is currently applied by which pension amounts are reduced if the pension recipient has earned income.

22 See the Mandatory Social Insurance Code, Chapter 6, Article 68, Item 4 23 See description in the Mandatory Social Insurance Code, Chapter 6, Article 70. 24 Called individual coefficients in the available English translation of the Mandatory Social Insurance Code 25 This figure, provided in a conversation on June 23, 2000 with previous NSSI General Director Mr. Nikolov, includes disability pensioners and survivor's pensioners. The NSSI is currently working with statistical informa- tion on the number of working pensioners, but data is not available as of ultimo June 2000.

13 Insurance contributions for pensioners are paid on the basis of the minimum wage, and at the account of the state budget.26

Assessment

Since several of the considerations and recommendations below are of a particularly delicate nature, one should prepare changes carefully and implement reform softly, for example by phasing out older regulations and apply new rules gradually where appropriate.

A national social insurance scheme should address the real social insurance needs of ordinary citizens. This would require:

The establishment of a clearer line of demarcation between social insurance and social assistance: Programs that are not of the social insurance type27, but are non-contributory, be- long under social assistance legislation.

Moving out merit-pensions from the national social insurance scheme: So-called merit pen- sions28 for outstanding services for the state do not belong in the national pension scheme. They might, eventually, be retained as special programs under special legislation outside of the national social insurance scheme. Hence, under a new system, military officers would receive pension benefits under the national social insurance just like any other occupational category. It is their eventual privileges that do not belong in a scheme that is national and general in scope.

Doing away with worker categorizations: A national social insurance scheme addressing the normal and real pension needs of the population should not be based on occupational categorization. The current system with three categories of workers is essentially a compensatory mechanism. It is true that bad working conditions can translate into pension problem in empirical terms, and that pension needs differ in the population. However, bad working conditions should first and foremost be approached as problems of bad working conditions and not as pension problems. And the disability pension is established to take care of permanent working incapacity based on medical, and potentially, occupational and labor market assessment based on individual circumstances. There is no reason to believe that all workers in occupational category I are worn out at 47 respectively 52 years of age. Taking this as given is a categorical assumption, or a proxy, unsubstantiated by convincing empirical observation.

Development of a life course logic to the pension system: Discontinue all other types of pen- sion at the normal age of retirement when all eligible persons receive the old age pension.

The avoidance of duplication wherever possible: This would imply the integration of the fund for Work Injuries and Occupational Sickness and the fund for General Sickness into one con- solidated program. It is true that the first of these programs as of today provide the more generous benefit package. But it is difficult to see why temporary or permanent incapacity

26 See op. cit., Chapter 1, Article 6, Item 7. 27 I. e., the Social Pension for Old Age (defined in Article 89), and the Disability Social Pension (characterized in Article 90) 28 Merit pensions in this context include: Military Disability Pension (Articles 85-86); Civil Disability Pension (Articles 87-88); Special Merit Pension (Article 91); and Individual Pensions (Article 92).

14 caused by specific events in a particular location should warrant preferential treatment and treatment by other authorities than the general population.

Establishment of a definite and uniform pensionable age: This means that the old age pension under no circumstances can be granted before the uniform pensionable age. The potential and real age of old age retirement in the present-day first pillar does not address real pension problems of the population. It is for instance meaningless to grant old age pensions to still fertile women. It is important to keep in mind that the Mandatory Social Insurance Code in- cludes a timetable for a definite pensionable age, which is common to all the current occupa- tional categories. This is certainly positive, but this definite pensionable age is first imple- mented in 2010. And the pensionable age will still be low, namely 63 years for men and 60 years for women. The pensionable age in one of the richest countries in Western Europe, Nor- way, is 67 years, for both men and women. It is difficult the see why a transition country with considerable economic problems and a clearly unfavorable demographic profile can afford to let men retire 4 years earlier, and women 7 years earlier.

Discontinue the differential regulations concerning length of service for the three occupa- tional categories: Present arrangements allow for a remarkable flexibility in the age at retire- ment. Persons having worked in occupations defined as demanding receive an old age pension after 15 years of service when they have reached the age of 47 years (women) and 52 years (men). It is of course true that the need for early retirement is different for different individuals and aggregates of individuals. That does not dictate a differentiated age of retirement for certain categories of people. If there is a need for early retirement due to permanent working incapacity, then entitlement for a disability pension exists. This is the raison d´étre of the disability pension. Current regulations obscure the relationship between the disability pension and the old age pension. The current determination of eligibility for the receipt of old age pension makes for a considerable flexibility in the pensionable age in the country, and for a remarkably low retirement age. To an outsider it is contradictory to call the old age pension ``length of service pension``. It is more accurate to describe the arrangement as a non-medicalized early retirement scheme.

Re-introduction of a work test: The number of working pensioners is striking.29 It is en- couraged through the continued accumulation of pension points and by the state's payment of insurance contributions for pensioners. It is strongly recommended to re-introduce either the first or the second mechanism mentioned above for regulating the relationship between pension receipt and earned income. A work test is necessary because a pension or a social insurance benefit is essentially income replacement. It is not some extra bonus on the top of paid work, or part of the process of wage formation. A possible argument against a work test might be that this violates the right to work. However, it is totally misplaced to argue that it is a human right to engage in paid work while simultaneously receiving a pension, which is meant as wage replacement. A series of countries apply a work test in pay-as-you-go schemes. It must be perfectly legitimate for national authorities to decide that the receipt of a pension rules out paid work either fully, or over a certain specified minimum labor input. The implicit and probably unintentional function of the current pension system is the subsidization of low wage labor, eventually subsidization of black market economic activity. Prime aged individuals on old age pension are taking jobs that young people might fill. However one relevant aspect here is that earnings are required to add to inadequate pensions. We are thus

29 Precise empirical data on the number of working pensioners by age and type of pension was not available in the NSSI by late June, 2000. Relevant detailed, but unanalyzed data are included in the Integrated Household Survey carried out by the World Bank in 1995.

15 confronted with a vicious circle. The core of the problem is however that small and possibly shrinking resources for pension purposes is spread much too thinly and unfocused in the Bulgarian population.

Disability Pension

The disability pension scheme included in the Mandatory Social Insurance Code has been al- ready described and analyzed in the paper: ``The Purification, Simplification, and Con- solidation of the Disability Pension Scheme``, of February 2, 2000, published by the USAID Pension Reform Project. Here, only the main points are recapitulated. The disability pension provides a pension when the health condition of a person is diminished in relation to a healthy person. The health reduction, which is classified into three categories from 50%, is determined by medical expert commissions under the authority of the Ministry of Health. The disability determination process is thus uniquely medicalized. The paper suggests changes in this process by:

Locating disability determination within the NSSI Expanding the types of relevant expertise in the commissions, Reintroducing occupational criteria and adjoining labor market considerations in addition to the medical ones.

The paper shows that rehabilitation is not inserted as a legal and operational requirement in the disability determination process, and it is strongly recommended to include rehabilitation efforts in this process.

The paper furthermore introduces the idea, repeated in the present paper, of imposing a-life course logic upon the pension system of the country. This would imply the establishment of a unique pensionable age at the time of which all eligible persons whatever their pension status, receives the old age pension.

It is recommended to abandon the two different sets of disability pension regulations of the funds for Work Injury and Occupational Sickness and for General Sickness respectively, by generalizing the rules of the latter.

It is finally argued that disability pension programs that are not of the social insurance type, be moved out of the mandatory social insurance scheme and, eventually included in either a social assistance program, or in legislation on merit pensions.

Survivor's pension

Description30

The general rule is that children are entitled to a survivor's pension up till the age of 18, how- ever eligibility can be extended if the survivor is a full time student till the age of 26. The sur- viving spouse is entitled to a survivor's pension 5 years earlier than her (specific) entitlement to the old age pension. Surviving parents who qualify for old age pension and who have lost

30 See Mandatory Social Insurance Code, Articles 80 through 83 for a description of the Survivor's pension

16 their child/children receive a survivor's pension. The survivor's pension is established as a percentage of the individual pension of the deceased person as follows:

One survivor receives 50% of the pension of the deceased Two survivors get 75% of the pension of the deceased divided equally among the survivors Three and additional survivors obtain 100% of the pension of the deceased, also divided equally among the survivors.

When the deceased person was not a pensioner, the survivor(s) will be granted a pension corresponding to what the deceased would have received as a disability pension at 90% re- duced working capacity.

Assessment

It is possible to argue that the survivor pension essentially belongs to history, when women's income and rank in society were determined by the breadwinner's station in life and when the breadwinner was the male spouse by definition. A basic point of departure for modern thinking about the issue is that a single woman should be able to care for herself and her children through own paid work, however. However, the chances of a woman of finding a job to make her and her family self-reliant shrinks with increasing age.

It is possible to argue that the inheritance of a pension runs contrary to the idea that women are independent and self-reliant labor market actors. It is also in opposition to the individual character of social insurance, which stipulates a link between (own) contributions and benefits. It is interesting to observe that two of the Scandinavian countries, Denmark and Sweden, have abolished the survivor's pension for these reasons. In these countries, widows receive means-tested social assistance cash benefits outside of the national social insurance scheme if their social and economic circumstances dictate this.

The foundation of the survivor pension is the idea that the family is an economic unit, and that the death of a spouse involves a loss of income for the family. The survivor pension seeks to reduce that income loss for the remaining spouse and eventual children.

The basic argument in this paper is that the inheritance approach to the survivor pension must be supplemented by a series of other relevant considerations. The following components should be taken into consideration:

The current regulations concerning income replacement mentioned above and expressed as percentages of the deceased pension should be kept as a point of departure.

The survivor's pension should be tested against the eventual wage income of the surviving spouse, and tapered off according to some agreed mechanism, for example along the lines of the work test of the old age pension being discontinued in 1997 (see pages 14-15). The arguments for a work test are essentially the same as those pertaining to old age pensions and wage income. The 1997-ruling of the Constitutional Court is based on the misunderstanding that somebody has the unlimited right to engage in paid work, while at the same time receiving a pension as income replacement.

17 The survivor's pension should also be tested against assets the survivor may have or receive, because it is unreasonable to use scarce resources in a deeply difficult situation irrespective of the economic situation of the surviving spouse

The duration of the marriage should count, and it is proposed to restrict the survivor's pension to survivors who have been married at least 5 years, or who have children below the age of 16 together.

The age of the surviving spouse should be above 50 years when chances of finding new employment start to decrease.

The survivor's pension is discontinued when surviving spouse reaches pensionable age and receives the old age pension.

A unique feature of the Bulgarian survivor's pension is that parents on old age pension receive a survivor's pension when their child/ren die.31 This is a graceful reflection of the strength of family ties in Bulgaria. However, one issue here is if children are liable to support their parents economically when they have reached pensionable age. If family liability goes so far as to dictate children to support their parents economically in their pensionable age according to the family law of the country of the country, this regulation makes sense. However, if this is not the case, this is a reason for why it should be discontinued. Another, and more straightforward reason for discontinuation is that it represents an addition of pension, which should be terminated as a matter of principle.

The survivor's pension is terminated if the surviving spouse remarries or if she/he initiates regular and stable cohabitation with a person of the other sex.

The entitlement to a survivor's pension must presuppose that the deceased was insured. If the deceased were not insured, the only available option would be non-contributory social assistance benefits from funds outside of the social insurance scheme. It would be meaningless for the survivor's pension to compensate any income loss of non-insured persons.

Individual pensions

The individual pensions mentioned under non-employment related pensions are granted by the Council of Ministers upon the proposal of the MOLSP or the MOF as prepared by the NSSI. These pensions can be regarded as a safety net for those who do not fully qualify according to the criteria of the Mandatory Social Insurance Code. The individual pensions are granted for life, and they are not means-tested. This implies that the pension is not affected by other income or assets, or significant changes in income and assets. Making up approximately 2,000 recipients, the individual pensions are not important in numerical terms, nor are they a liability to the NSSI, since they are funded by the state budget.

However, the individual pensions are important in three different respects:

31 See the Mandatory Social Insurance Code, Article 83, Items 3 & 4.

18 The individual pensions convey a deeply controversial message, namely that paying or not paying contributions to the social insurance scheme according to the rules of the game does not necessarily make that much of a difference.

The individual pensions perforate the already disturbingly lenient eligibility criteria applied by the Bulgarian social insurance scheme.

The other problem is that the individual pensions undermine the development of a proper social assistance scheme. Instead of using available resources allocated by the central government for social assistance purposes, majors of municipalities to some degree try to export their local social assistance problems to the central level and have them transformed to individual pensions

For these three reasons it is strongly recommended to discontinue the individual pensions. They are not pensions in any meaningful definition of the term, but rather life-long, not means-tested social assistance benefits granted by the state. The money for this pension should eventually be allocated for a modernized social assistance program.32

The Fund for Work Injury and Occupational Sickness

Description

The Fund for Work Injury and Occupational Sickness is a new institution in the social in- surance set-up of Bulgaria. It was established with the enactment of the Mandatory Social In- surance Code implemented as from January 1, 2000. The fund for Work Injury and Occupa- tional Sickness provides short-term benefits and disability pensions to persons who qualify. Eligibility essentially depends on the location and the circumstances of the event producing either temporary or permanent work incapacity or death. These events must be linked to the work place and be caused by circumstances at work. As has been shown, the benefits provided by this fund are more generous than corresponding benefits provided by the General Sickness and Maternity Fund (short-term benefits) and the Pension Fund (Disability- and Survivor's pensions). The replacement rates are higher, and the employers cover all contributions. The possibility of combining pensions and thus receive more than one pension simultaneously still exists with regard to recipients of benefits from the fund for Work Injury and Occupational Sickness.

No separate staff or structure have been assigned or set up to work with the fund for Work Injury and Occupational Sickness. The Department for Short -Term Benefits is responsible for contributions and benefits at central level on a temporary basis, until foreseen staff and structures are in place. The Department of Short-Term Benefits gives direction to the territorial offices of the NSSI concerning registration, investigation, and reporting. The Labor

32 According to the law, social assistance is organized and financed by the municipalities, but the responsibility has recently been taken over by the National Social Assistance Service under the Ministry of Labor and Social Policy. The program is subsidized by the central budget, yet no adequate mechanism is in place to ensure that money is used according to purpose. As of today, this means that financial responsibility and operational responsibility are split. A core problem is that the rules about who pays how much and who is responsible are less than clear. It is fair to say that the central/local division of labor and authority is not adequately institutionalized.

19 Inspectorate was responsible for these tasks until 1999; the NSSI was only obliged to pay the benefits. This has changed, and the problem for the NSSI is that the NSSI staff at the territorial offices is university-trained economists who lack the general and specialized competence to assess work injuries and occupational sickness. There is need and also plans to hire technical experts with general and specific knowledge, but such competence profiles are not easy to find. The NSSI tries to bridge the gap by synchronizing activities with the Labor Inspectorate and to engage the Labor Inspectorate in the training of NSSI staff at territorial level.

The justification for the establishment of a separate fund was that it would draw attention to the issue of bad working conditions and the improvement of such conditions. A core idea was to use differential contribution rates to be paid fully by the employers as an incentive mechanism for the improvement of bad working conditions. The starting point would be a contribution rate of 0,7% of payroll, but to this rate are the actual costs of temporary and permanent work incapacity as well as survivor pensions. This post-fact modification of the contribution rate will be replaced by a fixed pre-fact differentiated contribution rate in 2004 when enough empirical evidence has been gathered to establish such differentiated contribution rates. The critique against the temporary arrangement until 2004 being voiced by some employers has been that they are required to pay twice. The response of the NSSI to these understandable misgivings has been that they so far have little experience to set pre-fact contribution rates.

Assessment

This paper has argued that the fund for Work Injury and Occupational Sickness should cease to exist. It represents duplication of effort, and it provides better benefits than parallel pro- grams that speak to similar risks. One argument against the discontinuation of this fund might be that it contains a mechanism for encouraging employers to take working conditions seriously by the introduction of differentiated contribution rate. But three caveats should be kept in mind:

The suggested mechanism might have another, and not intended effect by encouraging employers to recruit a healthy selection of workers, and thus export the health problems of the enterprise to the social insurance- and health insurance systems. The point here is that we have little evidence to conclude either way, but experiences from Western Europe are less than conclusive.

Social insurance means sharing of risks. A system whereby each firm pays for its work injuries and occupational sicknesses would not be in perfect agreement with the principle of risk sharing. It is important to note that the major units in the fund for Work Injury and Occupational Sickness are the firms, and that too little thought has been devoted to how risks can be shared in a way that is conducive to good working conditions.

Having a separate fund financed uniquely by employer contributions is not the only mechanism to promote employer responsibility for adequate and healthy working conditions. Alternatives exist to sustain the same purpose, such as for example the employer period. This is the suggested functional alternative to the fully employer financed fund for Work Injury and Occupational Sickness. The expanded employer period recommended in this paper (see the section on Controls) is likely to increase the employers interest in controlling sickness absence as well as to improve working conditions. But also here, there is a certain danger that

20 differential recruitment of healthy persons may occur. It is possible to insert some flexibility in the length of the employer period according to performance regarding working conditions. Or one could imagine a certain amount of money reserved within the General Sickness and Maternity Fund to advance and encourage improvements with regard to working conditions.

The Contribution Collection Process

Description

The current understanding is that a new revenue raising authority should be established to control the collection and use of both taxes and social insurance contributions. The main argument is that a modernized unified agency would be more efficient, and that present arrangements imply too much duplication of similar work with regard to controls. More pre- cisely, it is maintained that the new unified collection agency would:

Improve service to insurers and insured as well as taxpayers Decrease staff Increase collection efficiency Reduce the tax/insurance burden

The project of establishing the new unified collection agency involves:

Redesigning business processes Creating integrated collection processes Establishing tripartism Developing coordinated controls and information systems Harmonizing income concepts

A Working Group headed by the Deputy General Director of the Tax Administration (GTA), Mr. Angel Savov prepares the unified collection agency. The Working Group consists of representatives from the GTA (3), the NSSI (3), and the NHIF (1). A concept paper has been prepared and is submitted for approval by the Steering Committee of the Working Group. Approval by the Council of Ministers is planned for June 2000. Further work in 2000 will consist in preparation of legislative changes, the development of business processes, and the design of unified IT-systems. The ambition is to start a pilot project as from primo 2001 to test technical solutions, and to have the new agency operational as from the beginning of 2002.

Currently, the General Tax Administration conducts its operations in 5 regional directorates, 25 regional offices, 5 large taxpayer offices, 130 divisional offices, and some 106 bureaus. The NSSI (and the National health Insurance Fund) conducts its operations in only 28 regional offices. 33 The issue of the geographical network of the new unified collection agency is as yet not decided. Relevant but also undecided in this respect is the issue of municipal taxation. Although no formal decision has been taken concerning decentralization or centralization of the new unified revenue agency, it should nevertheless be observed that the concept paper of May 17, 2000 argues in favor of centralizing the Unified Revenue Agency

33 Information is taken from the above mentioned concept paper ``Creation of a Unified Revenue Agency``. Sofia: Ministry of Finance. Paper for the URA Steering Committee, May 17, 2000.

21 (URA). The URA shall be ..``structured regionally, with one office in each of the the 28 regions of Bulgaria, each responsible for all administrative functions, processing service, audit etc, in respect of its regional taxpayer and contributor client base``. The arguments mentioned in favor of centralization are that it will help overcome the present fragmentation of the organization, that communication and control consequently is difficult, that duplication of tasks prevails, and that many buildings (82%) are sub-standard. The claim is furthermore that the centralization approach will ease necessary and significant IT investments as well as suitable accommodation for staff and clients. It is acknowledged that centralization will have ``some (negative) impact on clients``, but the positive consequences of centralization is more compelling than the negative consequences according to the argument.

There is furthermore the issue of compatibility between the new unified collection agency on the one hand side and the requirements of the second pillar on the other hand. The second pillar needs fast cash flow processes with high periodicity of payments. The contributions for this pillar are supposed to be invested, and the faster this occurs, the better is the performance in terms of generating assets and thereby income. Fast cash flow processes can also offset the impact of inflation in inflationary environments. The second pillar private pension funds also need money with no delay because they live on the fees received for handling the allocation of the contributions for the capital market.

Box 1: The Chilean experience

That the issue of the speed of the cash flow is potentially important is illustrated by the Chilean case: The result of 18 years of social insurance reform in that country is a fund of USD 35 billion, 60% of which is contributions, whereas 40% is derived from investments

The issue of controlling the payment of short-term benefits is one complicating element in this situation, and there is agreement among the parties involved that a solution to the control problem must be found before new agency becomes operational.

The idea of the new super-agency has been criticized for a number of reasons:

The tax administration and the insurance administration have different time-logics. The tax administration works with a time frame of one year, whereas the right to health in- surance is discontinued if payments have not been made during the last 3 months.

The tax administration and the insurance administration have different concepts of in- come: Insurance has the narrower definition and restricts itself to earned income, whereas the tax administration operates with earned income, capital income, and income derived from real estate.

A unified agency will also be required to produce two documents: one tax document and one unified describing the contributions to the insurance system, so what is the point in unifying the administrations? The establishment of a new agency will be a waste of

22 money since a working system already exists in the field of social insurance. There is therefore no need to invest in new machinery, new buildings, and a new controlling body.

The information system of the NSSI devotes 20% of its capacity and energy to the issue of collection of contribution. The resulting 80% are used for the calculation of pension, operations related to the issue of safety in the enterprises, and record keeping. The new agency would be unwilling to carry out these major functions.

The idea behind the establishment of a unified revenue-raising agency is in part based on an outdated conception of audits and controls of enterprises. With a new comprehensive computerized information system and true collaboration between agencies, a much more intensive control of current activities would be possible, for example checks on firms that withdrew money for short-term benefits but did not pay social insurance contributions, or firms whose contributions suddenly dropped.

To the extent that the physical presence of auditors is required or desirable, the question becomes who shall control the short-term benefits. The tax administration argues that it cannot do this, and the consequence is that we still need the 2 auditors.

Assessment

The most productive approach would be to take the new collection agency for given. The issue has been decided at the political level. The unified collection agency is also strongly advocated by the IMF, and recommended by the World Bank as well. It is however also im- portant to stress that the new agency will be a new organization, and not some addition to the General Tax Administration. It is true that such unified and efficient agencies exist in other countries, for example in Norway. The problems with the different time-logics, and the differ- ent conceptions and types of income can be solved. It would be possible to produce the two different documents within the framework of one organization as well, and the NSSI might continue to use its computerized information system for tasks that are not related to the col- lection of contributions. However, it is also vital that the NSSI is established as a separate institution and that its contributions have a unique status as earmarked money for a uniquely specific purpose. It is also important to observe that the NSSI has advanced productively along the road towards a modern and computerized information system with new and unprecedented possibilities to carry out controls. The collaboration between the NSSI and the General Tax Administration concerning the introduction of identification numbers has so far been less than optimal and the NSSI seems to have made more progress in its development of identifiers and information system than the GTA. It is important to keep in mind that the new unified collection agency is not meant to be the GTA in a new form. It is meant to be a new institution. It is furthermore crucial that the World Bank has already invested large sums of money for the improvement of NSSI operations and one must avoid redoing everything and waste the money already invested. The process of establishing the new agency should be developed through a series of well conceived and prepared steps to bring the different actors to identical technical levels with a shared understanding of both the common and the different tasks ahead. Inter agency conflicts are not a productive baseline for unification. Concrete collaboration between the agencies should be encouraged. The common identification system of enterprises and individuals should be a priority area and implemented before the new agency is launched A satisfactory solution to the issue of payment and control of short-term benefits must come before the new agency is established.

23 It is recommended to carry out a series of roundtables and a large conference concerning the centralization-decentralization issue. All points of view should be solicited, and foreign experiences should be presented and analyzed. The results of the seminar should be summarized in a written document, and presented to the Parliament in the form of a White Paper for discussion before a final conclusion is drawn. Since the arguments for centralization are known, the assertions in favor of decentralization, which are supported by the NSSI, should be spelled out, explained, and assessed.

A core concern underlying the work with the new unified collection agency is the need for revenue enhancement. It is however important to specify the different ways by which an increase in the compliance rate can be achieved. And as far as possible, these methods should be applied irrespective of organizational solution. The USAID Pension Reform Project has identified five different instruments for the increase of revenue efficiency.34 These instruments are summarized in Synopsis 6 on the next page.

34 The discussion of problems and possible measures and instruments is derived from Wayne Vroman. 2000. ``

24 Synopsis 6: Methods of revenue enhancement

Problem Solution Results Requirements

1 Payment delays & non-compliance 1. Monitoring of 30 largest debtors on monthly basis, Increased arrears collection of arrears. Arrears Allocate additional staff resources and of 100 largest debtors on quarterly basis collection increased from 29.7 mill. leva in 1998 2. More frequent payments for selected large employers to 57.6 mill leva in 1999. Prospects for 2000 are Visit samples of interorises, prioritize 3. Institutionalize non-scheduled site visits promising non-scheduled visits; reallocate staff 2 Untargeted contributions collection Focus collection efficiency efforts to districts with high Increase total volume of contributions Geographical reallocation of staff average wage level, low unemployment, and high rates of labor force participation, i.e Sofia and the 4 eastern districts 3 Absence of asset & cash flow 1. Hold assets deriving from revenue/ expenditure Maximize contributions income Statutory authorization to include management surpluses in the form of short term government debt forgone interest earnings instruments 2. Receive timely payment from the state budget for groups serviced by the NSSI but not covered by the Mandatory Social Insurance Code 3. Late payment of contributions required to include forgone interest earnings

4. Insufficient collection of 1. Clarify the concept of self-employment to reduce 20% of all self-employed persons (120,000 out of contributions from small postulated number, and introduce fines for erroneous 600,000) pay social insurance contributions at an enterprises classification average of 2.1 times the minimum wage adding to 2. Create proxies for contribution liabilities for farmers, 72.6 mill. leva in 1999. The contribution of all introduce seasonal payments when appropriate, as self-employed at 3 times the minimum wage well as payment at points of market transactions as would bring in 518.4 mill. leva. This means that required revenue forgone amounted to 446 mill. leva in 3. Require payment of contributions in connection with 1999, which is equal to 20% of total social license renewals in service sector insurance revenue 5. Insufficient collaboration with the 1. Introduce common tax identification number for Increase the collection of contributions tax administration individualo workers & from the self-employed 2. Alignment of policies concerning presumptive taxes

25 Cash-Flow Efficiency

The idea here is the establishment of a new, cheaper, more flexible, and efficient cash flow involving all the transaction from payment of contributions and on to payment of pensions and benefits. As of today, money is transferred from enterprises through local banks, to the national bank, back again to the local banks, and then onwards to the post offices for payment. 95% of all social insurance benefits is paid out in cash. The postal service receives 0.85% of the total social insurance payments for its payment function. The postal service of the country is subsidized by the state budget. Payment takes place on specific dates from the 7 through the 20 each month according date of birth of the recipient and to lists provided by the NSSI in specified post offices. The benefit recipient is obliged to show up in person. Those who fail to do so have to wait one month. They get no interest of delayed payments. This creates problem for the recipient and also for the post office, which is supposed to return money to the NSSI that is not picked up

This system of physical transfer of money is time-consuming, expensive, and essentially unnecessary. The dispersed system of postal services is not utilized to its full and productive potential and can be used to simplify the cumbersome process as of today. There are 3,600 post offices in the country as of today. The buildings are there, however the level of automation is low. The plan is to retrain and involve the available staff of the postal service in a simplified operation in which employers pay and deposit contributions in their respective local banks, which then transfer the money to the postal service for payment to the pensioners and clients. In this way the money remains on the territory where it is supposed to be spent. Any surplus in the form of unused money is transferred to the central bank of the NSSI to be allocated for districts with shortages.

A difficulty with regard to the implementation of this idea has to do with the low technical capacity of the post offices and the low level of skills of their staff. The banks earn money on the current transmission of money, and the success chances of the idea will therefore also depend on the strength of the banking lobby. Likely support for this reform will come from the NSSI, which can service its pensioners and clients better. The government will be positive because it will no longer need to subsidize the postal service. The postal service may recommend the idea because it will be able to use its resources to full capacity and receive money for its services.

A meeting was arranged during week 21 with General Director, Mr. Kratsev of the Post Office (PO), the General Director of the NSSI, Mr. Hristostov, former General Director of the NSSI, Mr. Nikolov and several experts from the PO and the NSSI. It was agreed to start the work at expert level with the further preparation and implementation of this A Working Group was appointed The Friday May 26-meeting decided to begin with the issue of contributions collection. In the second stage, the PO will become a body from which money will be paid out. The General Director of the Tax Administration supports the plan. It has also been substantiated that the Minister of Labor and Social Policy supports the idea.

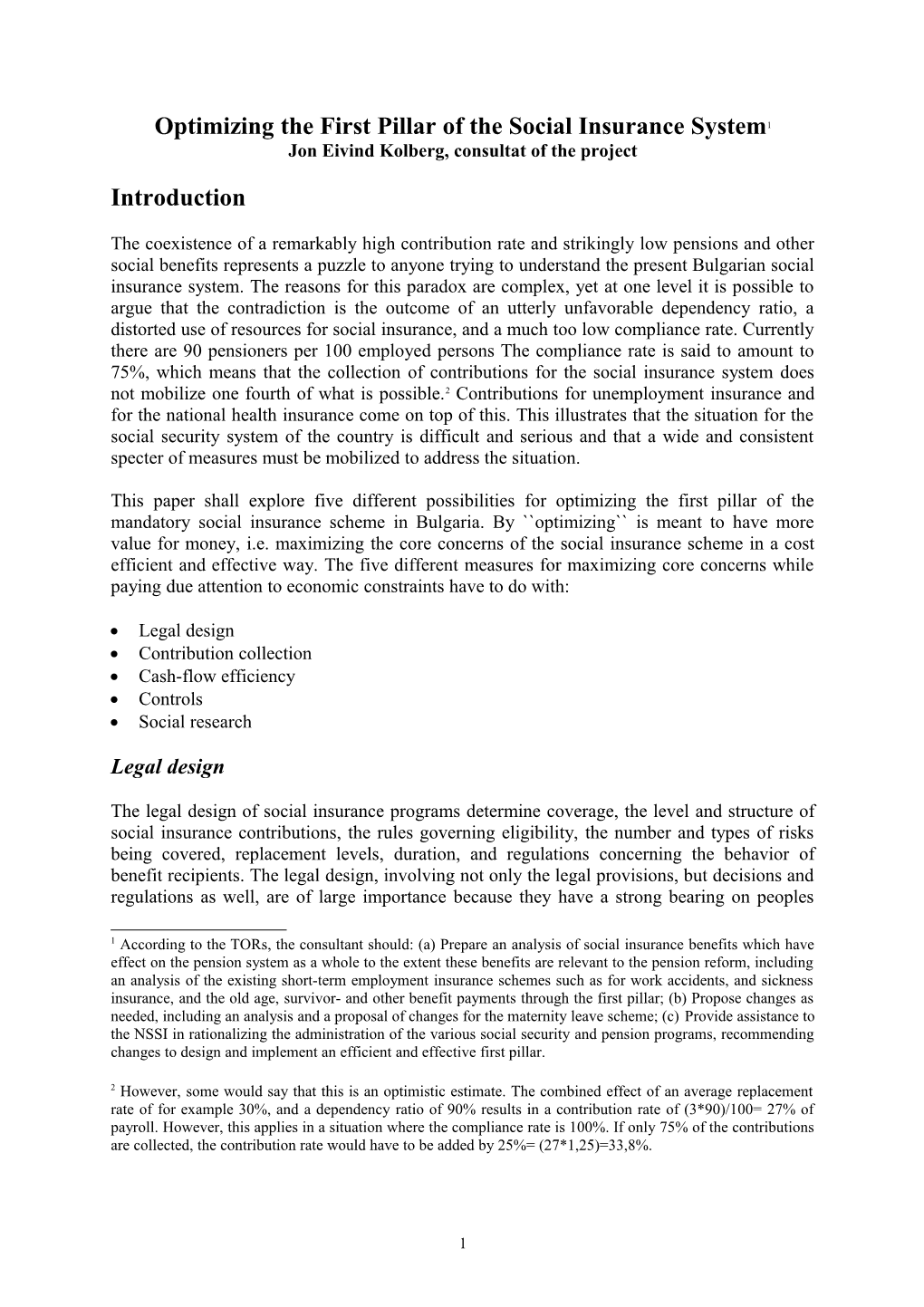

26 Figure 1: The current cash-flow system

NSSI Employer's NSSI local Employer Headquarter's bank bank bank

Post Office

Benefit recipients

The new system (see below) would involve money to come from the employers through their local bank to the PO, eventually from the employers and directly to the PO for those employers who have no bank account. Surpluses will be sent from the PO to the central account of the NSSI in the National Bank of Bulgaria to form an equalization fund to be used to pay for benefits where there is not enough money. A rough estimate is that the new system would imply savings amounting to 2% of monthly pension expenditure, which is currently 182 mill. leva. This would correspond to between 40 and 45 million leva on an annual basis.

Figure 2: A simplified, flexible, and inexpensive cash-flow system

Employers

Post bank/Post NSSI office

Benefit recipients

The new system will improve the collection of contributions. The POs will make better controls. The control bodies of the NSSI today are headquartered at the regional level. The POs know the people who are supposed to pay contributions by name. The NSSI will be present in every locality, and the idea will thus bring the NSSI closer to the

27 community.People will have a better chance to see with their own eyes the logic of paying contributions and getting benefits. It will also be cheaper to deposit money. There are areas today where self-employed and smaller employers have no banks to which they can pay their contributions. The PO will charge no commission. Private banks charge a commission. Only the large banks benefit by today's system. Using the POs will also improve the service for the clients. They can come on any day, take out the whole amount or some of the money and thus save, the can go to any PO. But the program assumes computerization of the POs and the training of staff.

The first stage can be operational as from July 1, 2001. Then comes the payment side.

Plans for further steps are:

1. Working out a draft for a pilot project. Great interest for a pilot project has been expressed by the Major of Sofia

2. Working out draft regulations, and draft decree or legal changes

3. Implementation of a nation-wide system by the end of 2001.

Controlling Short-Term Sickness Benefits