DGIII/DCS (2005)

FORUM 2005

RECONCILING LABOUR FLEXIBILITY WITH SOCIAL COHESION

CONCILIER FLEXIBILITE DU TRAVAIL ET COHESION SOCIALE

17 & 18 November – novembre 2005 Conseil de l’Europe/Council of Europe Strasbourg, Palais des Droits de l’Homme ______SESSION II

The effects of labour flexibility and possibilities for reconciliation Effets de la flexibilité et enjeux de la conciliation ______

For the discussion in workshop 1

Labour Market Flexibility and security: The Russian Way

Vladimir GIMPELSON European Trade Union Institute (Brussels)

In his paper on Russian employment and unemployment written in the mid-90s, Richard Layard coined the term: “the Russian way in labour market adjustment”. He used this term to point to specificities of the Russian model of labour market adjustment where wages are very flexible while employment is rigid. Since then much has changed in Russia but the labour market has not left this pathway.

The institutional core of this model is a “cocktail” containing very rigid formal rules, as they are fixed in labour legislation, poor law and contract enforcement, and the wage-setting machinery linking individual wages to the enterprise’s financial performance. This type of the labour market absorbs external shocks by extreme downward wage flexibility, and hence smoothes employment and unemployment fluctuations. Each of the three macroeconomic crises (1992, 1994, 1998) in Russia throughout the nineties has cut a big slice of an average worker’s real wage while affecting the aggregate employment very little. Russia has come out of this turbulent period as a good performer in employment and unemployment.

Accepting «the Russian model» as an angle of view explains various dimensions of labour market and social policy development, including high inequality and proliferation of poverty among the working population. In the «standard» case, being a long-term unemployed, low-skilled and non educated person increases the likelihood of being in poverty. On the contrary, the Russian model proliferates poverty among the most educated part of the labour force, including teachers, healthcare doctors, or scientists. Stimulating inequality and individual adjustment destroys cohesion and solidarity in the society. Neither the recent economic growth, nor the new labour legislation that was enacted in 2002 has changed the systemic core of the Russian model in labour market adjustment.

The paper is structured in the following way: I. The first paragraph shows how flexible the Russian LM actually is and what the major properties of this particular flexibility style are. II. The second section presents the normative and regulative framework giving an insight into how rigid the Russian LM is expected to be. III. The third paragraph discusses tentative reasons of why the gap between the actual performance and normative framework exists and is so large. IV. The fourth section sums up the major implications of this style of flexibility as a tentative balance sheet for socio-economic gains and losses. V. The paper concludes with policy recommendations..

1. Labour Market Adjustment: “The Russian Way”

We can start the discussion with looking at the evolution of the labour market in Russia from the turmoil of the earlier 90s throughout the transition.1

The complete story of the labour market adjustment since the early 90-es can be divided into two distinct phases. At the first phase that lasted till the end of 1998, the deepest transformational recession brought the aggregate GDP down by 40%. The labour market reacted to this fall only with a slight reduction in employment (14% less employment with a fall of 40% (!) in GDP). The increase in open unemployment was modest, but working hours shortened significantly and real wages decreased drastically. At the second phase (since 1999), when the economy entered the post-transformation recovery growth, most of the key labour market indicators began to improve modestly while the increase in real wages was rapid and impressive in its magnitude.

These unconventional properties of labour market adjustment in Russia (and the CIS countries in general) are in contrast to those observed in the Central and Eastern European or Baltic (CEE) countries.2 The labour market in the CEE and Baltic countries has been behaving more or less conventionally though with some regional variation. That is, the employment side usually takes the brunt of adjustment while wages do not. In Russia and the CIS, flexible wages stand against inflexible and robust employment trend.

Let us take a short trip through major dimensions of the labour market adjustment in Russia.

The economic activity of the Russian population has been remaining high. The participation rate (in Russia, it is conventionally measured for the 15-72 years old) decreased from 70.3 per cent in 1992 to 61.1 per cent in 1998, but then it went up to 66 per cent in 2002-2003 following the wage recovery in the post-crisis period. Cumulatively, the decline in participation over the whole period was less than 5 percentage points (pp) and had no gender-specific bias. For women, the magnitude of decline was of the same size as for men. Despite the deep economic recession, Russia managed to avoid large-scale outflow from the labour market what was the case in some CEE countries (for example, in Hungary). If recalculated for the more conventional age of 15-64, the participation rate in Russia makes up 70 per cent and can be considered one of the highest among all transition economies. If recalculated given the legislated retirement age of 55/60, the labour force participation becomes one of the highest in the world.

1 Vladimir Gimpelson & Douglas Lippoldt (2001) The Russian Labour Market: Between Transition and Turmoil, Rowman and Littlefield, 2001. 2 See, e.g., The World Bank (2005), “Enhancing Job Opportunities in Transition Economies of Europe and Central Asia”. The employment/population ratio (the employment rate or e/p ratio) in Russia has also been staying stable and has been low insensitive to the multiple exogenous demand shocks. Throughout the reform period, the aggregate decline of the employment rate has never exceeded 15 pp (compared to the initial pre-transition level) and has obviously been disproportionately small given the almost halved GDP. The e/p ratio is currently at about 65% for the population as a whole and stands at around 70% for the working age population(age group 15-64). This is a surprising performance, since in most of the countries in the CEE region, the employment followed closely the GDP trend. It fell when the latter was in fall and then stabilized when the GDP started to grow again. The obvious divergence between the evolution of the GDP and that of employment testifies a sharp drop in productivity in the first half of the 90s, that most of the CEE countries have avoided.

The economic recovery following the 1998 financial crisis brought the resumption in employment growth. Various estimates suggest an increase in the aggregate employment with the magnitude of 3 to 5 million persons. Most of these jobs have been created in the service sector, including small firms, non-corporate entrepreneurship, and self-employment. Therefore, the Russian economy did not experience the "jobless growth" typical for many CEE countries, as a whole but only the corporate sector largely did. Large and medium sized firms lost 2-3 millions of jobs while small noncorporated businesses and self-employment gained, off-setting this loss and driving the total employment up. Significant lead in GDP growth rates over employment growth rates resulted in rapidly growing productivity during this recovery period.

Given the unprecedented scale of the transformational recession in Russia, one could expect to see this country as an unemployment “leader.” The combination of initially high proportion of industrial employment and relatively low proportion of rural population increased the likelihood of this scenario.3 However, neither at the earlier stage of the market transition, nor at its later stage the Russian labour market has been close to any explosion of joblessness. In this sense, the market response has also been atypical.

The Russian unemployment growth was gradual and stretched over a rather long time period. It took five years of the market reforms and the GDP to fall by 40% for the rate of unemployment to exceed 10 per cent of the labour force. The maximum point of around 14 per cent of the labour force in the unemployment was reached at the beginning of 1999 or on the 8-th consecutive year of the transition. Since then the unemployment has been on a gradual downward trend and is now under 8 per cent of the labour force. This outcome can be considered a very good performance, if other things are not taken into account.

There are a few reasons making us think that the evolution of unemployment looks atypical if compared to other transition countries:

а) the unemployment trend was gradual without any steep ups and downs caused by mass layoffs; b) its rate never reached peak levels typical for other post-socialist countries; c) it decreased faster than in other transition economies when the economic recovery began; d) the current (LFS based) rate (around 7,5 per cent of the labour force) makes Russia one of the best performing transition economies; the registered unemployment is almost negligible with 2 per cent of the labour force; e) the long-term unemployment is smaller in its size and shorter in duration than in the CEE countries.

In Poland, which is usually considered one of the best economic performers in the CEE region, the unemployment is coming close to 20 per cent. Slovakia and Bulgaria are close to this level. The alternative labour market indicators confirm the picture. The long-term unemployed account for a third of all unemployed in Russia, while in the majority of the CEE countries long-time job seekers make over half of the stock. Consequently, Russia enjoys now a long-term

3 Subsistence agriculture can absorb the labour slack from the downsizing of the overmanned industry. unemployment rate of 2.7 per cent , which is also one of the lowest among all the transition economies.

Atypical adjustment also manifests itself in the flexibility of working hours throughout the period. In the first half of the 1990s, the average annual number of working days in industry decreased by nearly a month. Since the mid-1990s, the number of annual average working hours per worker in the Russian economy has somewhat increased, but they are still shorter than before the start of the reforms. This hints on the fact that quasi-fixed costs seem to be lower than firing costs. In the CEE countries in contrast, the working time figures have been stable enough and have not much changed as compared with the pre-reform period.

There is also a remarkable variation across employees in actual working hours. Both shorter and longer working weeks (compared to the weekly 40 hours standard) are widespread. About 15-20 per cent of all employees work longer hours. Working hours reacted flexibly to fluctuations in labour demand, easing the adjustment.

However, the most peculiar feature of the Russian labour market model concerns wage behaviour. The observed magnitude of wage fluctuations within short-term periods seems to be unprecedented. This flexibility has emerged as the opposite side of employment rigidity. Wages proofed to be flexible at macroeconomic as well as micro level, hence violating the economists’ standard belief in their downward rigidity. During the nineties, the average worker’s wage lost two thirds of its real value. This “loss-making” was not gradual over time but strongly concentrated around three particular time episodes associated with major macro-shocks. The price liberalization in January 1992 cut real wages by one-third, the financial crisis of October 1994 took away approximately one-fourth, and finally the financial crisis of August 1998 devalued the real wage by over 30 per cent once again.

The wage flexibility was further enhanced by use of wage arrears and various forms of informal off-the–book payments. The concealed part of the total labour remuneration was typically the first to react to any changes in the economic situation. Such large-scale wage adjustment allowed to over-compensate the pre-shock rise in total labour costs and it also eased the market pressure on the employment. Each shock was followed up with an immediate and partial wage recovery. In 2000-2003, annual real wage growth reached 10-20 per cent and, as a result, real earnings nearly doubled.

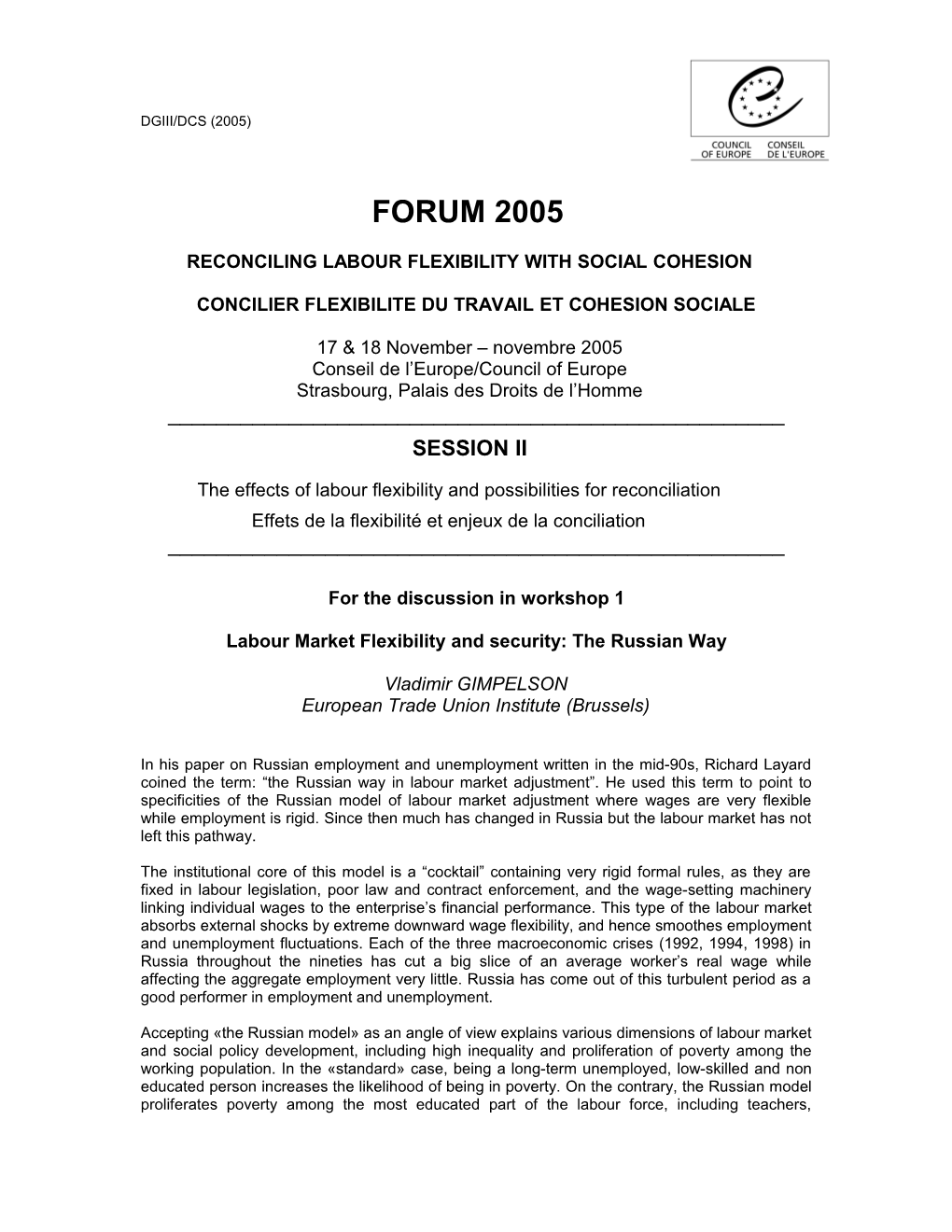

The Fig. 1 illustrates the dynamics of employment and wages throughout the period under consideration. We can clearly see how insensitive and inertial the employment is and how flexibly and reactively wages behave.

In all the former socialist countries, the systemic change has brought a rise in earnings inequality. In Russia, this increase was exceptionally large. The Gini coefficient jumped from 0.32 in 1991 to the level of 0.40-0.45 within a decade. This suggests significant flexibility in relative wages and the link between earnings inequality and wage-setting rules (discussed below).

However, a considerable portion of the inequality is a function of the size of the Russian territory and of the enormous diversity in economic structure across the country. The inter-regional (between regions) component of the inequality explains around one fifth of the total inequality. In fact, most of the intra-regional Gini coefficients for earnings are much smaller in their magnitude and are similar to the CEE values. The notable exceptions are oil- and gas extracting regions in the Siberian part of the country, which are much less equal. However, none could expect raw materials extracting economies to generate low-inequality wage distribution.

Throughout the transitional period, the Russian economy experienced an intensive labour turnover. If defined as the sum of hirings and separations rates, it reached 43-55% for the entire population of large and medium sized enterprises and 45-60% for the industrial sector. These turnover rates were noticeably higher than in the majority of the CEE countries. Remarkably, layoffs played a minor role and new hirings remained buoyant throughout the period. Even in the most critical years, the hiring rate in Russia was steadily high. This could mean that employers were quite confident that, if necessary, they would be able to contain labour costs.

The domination of voluntary quits in the structure of labour turnover looks no less paradoxical, while involuntary separations contribute very little to the total turnover. Layoffs accounted for not more than 1-2.5 per cent of enterprises’ workforce, or 4-10 per cent of the total separations rate. Meanwhile, (voluntary) quitting rates reached 16-20 per cent of the workforce, or 65-74 per cent of the total separations. Even admitting that a certain proportion of lay offs was disguised as voluntary quitting does not change the major conclusion too much. Still, it is hard to believe that majority of quits are hidden layoffs.

High rates of labour turnover resulted in proliferation of short job tenures and high proportion of short-tenured workers on the Russian labour market. The average tenure in the late 90-es was under 9 years and the proportion of workers with the tenure under 1 year was 17 per cent of all employees. This induced H.Lehmann and J.Wadsworth to entitle their paper on job tenures in Russia as “Job Tenures that Shook the World”. Both indicators (average tenure and % of short- tenured workers) clearly differentiate Russia from other CEE economies and tend to confirm the status of Russia as a high mobility country.

High labour turnover was associated with large-scale cross-sectoral reallocation of employment. If in the early 90-es the service sector accounted for about 40 percent of all jobs in the economy, this proportion reached 60 per cent within 10 years. This 20 pp structural shift caused massive occupational change and was called “the Great Human Capital Reallocation”.4 According to K. Sabirianova, 42 per cent of all the employed changed their occupation in the period between 1991 and 1998, and two-thirds of them did so at the initial stage of the reform period in 1991-1995. This may mirror the fact that the Russian population enjoys significant stock of general human capital, while the skill-specific component of the human capital has become obsolete or strongly depreciated. Mass labour reallocation supports the point that the Russian labour market allows for remarkable external flexibility.

Use of a variety of "non-standard" forms of employment reflects another dimension of labour market flexibility. This relates to the both external and internal flexibility.

As non-standard, one usually understands various forms of employment assuming either part- time or short-term labour contracts. Self-employment, or contracting with TWA, or various types of individual subcontracting, or combinations of all the aforementioned also belong to the non- standard employment. Additionally, in the 90-es Russian employers used widely other non- standard forms of labour like part-time work and forced administrative leaves, wage arrears and pay-in-kind, which were not explicitly legislated but emerged as an outcome of non-enforcement of the law.

Taken altogether, the non-standard employment has brought a great help in adjusting labour costs in hard times.

In some years nearly 25 per cent of the personnel of large and medium-scale enterprises worked shorter hours or were on administrative leave. Informal (undeclared and therefore not taxed) payments made up to 50 per cent of official remuneration. In some moments wage arrears affected almost three-quarters of the country’s working population. Though various “non- standard” forms of adjustment have become much more rare since the beginning of the recovery period (for example, the rate of involuntary part-time employment has gone down below 1%), they are still used and they embrace not a negligible part of Russia’s labour force.

4 Sabiryanova K. (1999). Most of the “non-standard” adjustment mechanisms have one important feature in common: they are informal or semiformal. They allow bypassing the laws and other formal restrictions or act against them. Delayed and hidden wages and salaries and part-time and secondary employment led to personalization of employer-employee relationships, which resulted in a substitution of informal relations for formal labour contracts.

To sum up, the Russian labour market was characterized by relatively stable employment and moderate unemployment, flexible working time and super flexible earnings, intensive labour turnover and high incidence and variability of “non-standard” labour relations. In consequence, it proved as capable to absorb numerous negative shocks that had accompanied the systemic transformation.

2. Labour Market Flexibility: The Normative Framework

The picture presented above may lead to the conclusion that this particular labour market hardly has any regulations. However, this conclusion would be a wrong one. Moreover, a closer look at the legislative framework within which the Russian labour market operates reconstructs an absolutely opposite picture. The Russian labour market emerges as one of the most regulated markets in the modern world. These regulations are restrictive in all major components and, if strictly enforced, allow little space for any flexibility.

From the institutional standpoint, the scope for flexibility is largely determined by the employment protection legislation (EPL). The Code of Laws on Labour (KZOT) that was in force in Russia throughout the 90-es was adopted in the Soviet times (1971) and, though with multiple partial amendments, acted until 2002. It was born within the central planning system, fitted its needs and its spirit, and had little to do with the market economy.

The KZOT required employers to hire employees on open-ended contracts with working week of the standard and fixed duration. It provided very high level of formal employment protection for regular workers. Under the law, the trade unions enjoyed veto power on any layoffs due to economic reasons. Even if the trade union did not object to laying-off redundant personnel, firing costs incurred by employers were prohibitively high. The law stipulated 2 months of advance notice to trade unions and local authorities and the severance pay equal up to 3 monthly average wages regardless of their actual job tenure. In case of employees working in the Northern part of the country (around 10% of the total employment) the total severance pay could make up to 5 average monthly wages. Thus, for the core workers the total duration of advance notice and severance pay was equal 8 months.

The KZOT put serious constraints on use of non-standard labour contracts, e.g. fixed-term contracts were allowed in exclusive cases only. Overtime was formally permitted but with the duration strictly limited to annual 120 hours. Additionally, the labour legislation was overloaded by various requirements of social benefits and guarantees, which were to be funded by employers. During the 1990-es multiple amendments to the labour code were introduced but they did not change the principal nature of the legislation. The legislation remained very rigid but full of internal contradictions.

The new Labour Code adopted by the legislature in 2001 came into the effect in early 2002. Though many contradictory and obsolete requirements were abolished, the EPL part of the Code changed very little. Having emerged as a political compromise it basically inherited all major rigidities from the old KZOT. Unsurprisingly, the Labour Code contains norms reflecting realities of the market economy as well as it preserves constraints inherited from the Soviet past. 5 This conclusion relates to the labour legislation, in general, and to the EPL component, in particular.

5 The major positive change was in abolishing trade unions’ veto power on mass lay-offs. Firing costs remain prohibitive as much as they have been, while the use of temporary contracts is still over-regulated. The Labour Code includes a closed list of reasons allowing temporary contracts. In Spring 2004, the RF Supreme Court issued special directives warranting against more liberal interpretation of this part of the Labour Code and calling for a more restrictive use of the temporary contracts. Fixed-term contracts if signed illegitimately must be treated as an open- ended. Courts usually treat all labour contracts related cases in favour of employees.

In 2002-2003, we surveyed 900 industrial firms in order to understand employers’ attitudes to the changes brought by the new EPL. The major conclusion was that enterprise managers did not see any significant affect from the EPL change on firm’s labour market behaviour.

High unionization rate, centralized bargaining, and significant tax wedge add to the likelihood of labour market rigidity as it should emerge from the formal institutions.

We can put the Russian EPL in the cross-country comparative context using a family of integral indexes of the EPL stringency. Such indexes designed by various international economic organizations (the World Bank, OECD, ILO) differ in methodology and vary in coverage of countries. However, they all unambiguously point at the fact that the formal labour market regulations in Russia are among the most rigid in the world.

On the World Bank (2003) EPL scale, Russia has 61 score against 45 scores on average for the OECD countries. The higher score means a more protective and rigid labour market. If only regulations on firing are considered, the Russia – OECD gap becomes even larger with a score of 71 compared to an average of 28.

The OECD EPL scale gives Russia 3,2 scores against 2,0 scores for the OECD countries on average, 2,4 scores for the old EC countries, and 2,5 for the transition economies. 6 These estimates refer to the year 1999 and do not account for changes in the labour legislation, which were introduced in Russia, Poland, and Slovenia later. But if in the two latter cases the EPL was softened significantly, the new Labour Code in Russia changed the country standing on the general EPL scale very little. This means that the gap between Russia and other transition countries in this respect should even grow. It would be fair to remind here that the flexible labour market is among the most important factors shaping favourable investment climate.

3. Why Do Normative and Actual Patterns Differ?

As we can easily see, the actual flexibility pattern contrasts with the normative framework. This raises the question of how to reconcile them. How can labour market perform as flexible as it does if all the labour market regulations are so rigid as they look like?

The answer seems quite obvious. This is possible only if these regulations are poorly enforced and employers and employees do not consider formal norms as credible and binding. In the 90- es, the Russian state was not only unable to enforce labour laws but itself was the first in violating them, thus transforming constraints and incentives for all labour market agents. 7 The recent World Bank study specially underlines that the labour market flexibility in the CIS countries comes basically from “flexible” enforcement of stringent EPL rules.8

This part of the story goes, however, far beyond simple non-enforcement. The actual “rule of law” is selective and varies across regions, sectors, old and new firms, and also across various

6 S.Cazes, A.Nesporova. Balancing flexibility and security in Central and Eastern Europe. ILO, Geneva, 2003, p.100. See also: Employment Outlook for Russia. Volume 1 (1991-2000), Annex 3. 7 V.Gimpelson. “The Politics of the Labor Market Adjustment (the Case of Russia)”, in J.Kornai, Haggard S., and R.Kaufman, “Reforming the State: Fiscal and Welfare Reform in Post-Socialist Countries”, Cambridge UP, 2001. 8 The WB Study “Enhancing Job Opportunities in Transition Economies of Europe and Central Asia”, 2005. segments of the EPL9. In large and unionized firms (making roughly 2/3 of the total employment in Russia) the EPL is enforced relatively better but in small firms it hardly holds at all. All this increases general uncertainty and differentiates firms in terms of their mandatory labour costs. Firms that enjoy discretion in applying the EPL may deprive some of all workers of any social protection, those firms that follow the rules prefer not to create new jobs and try to keep low wage policy. Formally law obeying large and medium sized firms often use small firms as flexible suppliers of labor.

This selective flexibility is reflected in aggregate employment dynamics and employment to output elasticity for the period 1999-2004 (or for the post-1998 crisis period). Since 1999, the aggregate GDP has grown by over 40% while the total employment has added around 9% or 5 mln. Meanwhile, the regulated segment of large & medium sized firms (the main driving force in the GDP recovery) has lost 2-3 millions of jobs. This means that in this segment the response of employment to the output growth was negative, while all the employment growth (including the compensation for the loss of corporate jobs) took place outside the regulated segment.

The perverted flexibility is also facilitated by specific public and private sector wage setting institutions and policies. The standard case assumes that the ongoing market wage reflects marginal productivity of labour and depends on the worker’s human capital. The prevailing wage principle links salaries of the public sector employees to the private sector wages. All wages are downward robust and low sensitive to exogenous shocks, etc. In Russia, wages are not sticky and react flexibly to any fluctuations in financial performance.

Let us start with wage setting in the private sector. In the Russian case, the wage setting machinery allows individual wages to fluctuate with significant magnitude. One of the major reasons for this is in their linkage to the financial performance of firms. The basic (tariff) part of individual wage, which is in fact downward rigid, makes on average about half of the total, while the rest of the pay constitutes a kind of bonus or wage premium that indirectly reflects financial performance of firm. Since the performance is variable over time (and across firms) and the employment is sticky due to inertia, the wage premium can grow in good times (and good firms) and shrink in bad times (and bad firms). In the best performing companies, the wage premium component may make a multiple of the basic (tariff) component. Moreover, these wage gains are not allocated across workers reflecting relative differences in their human capital only but they mirror largely differences in workers’ individual bargaining position. Meanwhile, workers’ bargaining power comes from multiple sources, including their firm specific skills, demand and supply factors, outside job opportunities, some social considerations, informal relations, etc. All this generates not only remarkable wage flexibility but significant intra-firm inequality as well.

As it should be said here, firms are absolutely free in selecting a wage setting system. However, many firms in the old corporate sector prefer to use a kind of tariff scale, which is implicitly linked to the national minimum wage. Minimum wage defines a lower bound for any tariff scale but the latter may be much higher than the minimum wage itself. Since the national minimum wage is set at a low level, the rigid part of the total individual wage is relatively small while the flexible or variable part of it is, on the contrary, quite large and depends on the firm financial performance.

Private sector and public sector labour markets are not fully autonomous. They clearly interact and affect each other. Now let us take a look on the public sector, which is still pretty large in Russia. The public sector has particularly large employment in education, health care and public administration. So does this mean that the government is the ultimate wage setter to the public sector? Does the public sector wage setting affect the private sector wage setting and how? What are the implications for the labour market flexibility?

The public sector pay is based on the so-called Uniform Tariff Scale (UTS) directly linked to the minimum wage. However, the UTS system providing the lower bound for pay does not exclude

9 For example, the layoffs related regulations are enforced better than the regulations on overtime work. any upward salary adjustments if financial opportunities for this exist. Public entities (public schools, hospitals, museums, research institutions, etc) receive mandatory budgetary funds based on the UTS system. Any additional – non-budgetary – funds, if available, can be translated into further wage increases. Access to additional sources is not evenly distributed across public sector entities and is much better in large cities and economically well-off regions. Additionally, many of them are engaged in commercial activities proceedings from which can be used for funding wage premium. How this premium is distributed across entities and within entities results from decentralized decisions in regions and in particular entities. Therefore, resulting wage differentiation comes from several sources: the UTS-based wage setting, region-specific funds, entity-specific funds, and the individual’s bargaining position. All this partially explains the significant wage differentiation that prevails even within the public budgetary-funded sector.

As an illustration we can cite results from our survey of 400 secondary public schools conducted by our Centre in 2004. Public schools are quite homogeneous entities; they are subject to the same uniform regulations and the same wage schedule. However, the ratio of maximum average wage in the surveyed schools to the minimum average wage (in the surveyed schools) exceeds 4 times, while all 6 regions in the sample are in the middle of the distribution and are not among the most affluent or depressed territories. Simple econometric exercises show that being in a particular region is the most important factor determining wage level in a school since it reflects regional fiscal position. The max/min ratio in average wage in the educational (dominantly public) sector between regions makes 5 times. The same wage differentials we see for other public sector economic activities. This also questions the tentative argument that the wage system is strongly centralized.

The legislatively set minimum wage and the Uniform Tariff Scale are not differentiated across regions despite the enormous interregional heterogeneity. Having regionalized minimum wages would probably increase wage differentials in the public sector. But even the uniform minimum wage does not bring all regions to the same actual wage level. Since setting of the minimum wage level should account for regional labour market conditions in order not to disemploy critically laggard regions, the minimum is usually set at the level that is affordable for the most depressed regions. For all others regions (which are relatively better off) this level appears to be too low for any upward spill-over effects. The contrary is more likely. Higher alternative private sector wage may drive the public sector wage upward while regional budgets are forced to accommodate this additional demand as much as they can. As a result, public sector entities differ in terms of wages actually paid and in proportion of salary determined by the centralized UTS.

In Russia (as well as in the CIS countries), the public sector pay is much lower than the private sector wage. Low relative wages in the public sector can hardly have a disemployment effect but may lead to expansion of the private sector low wage jobs. There is a strong empirical regularity that public sector employment across Russian regions is negatively correlated with the per capita GDP and the regional fiscal position. The most depressed regions have a very large chunk of employment in public education, health care etc. In some regions the educational institutions make up 20% (!) of the total employment. This turns the public sector into the major employer in some regions and a principal wage setter. In this sense, private sector firms are “wage-takers” with the downward directed pressure. Therefore, the public sector “works” as a wage anchor contributing to general earnings inequality.

One of the questions that may arise here concerns the role of trade unions in this wage setting and the EPL enforcement story. As the story goes so far, one may assume that we are discussing an economy where there are hardly any trade unions. Again, formally this is an opposite case since the old corporate sector and the public sector have very high unionization rate and quite high coverage by collective agreements. Nevertheless, these agreements are in reality not binding and have the same enforcement problem as the EPL has. This makes the collective voice barely heard while workers are left with individual voice and exit options only. Sure, the high flexibility and adaptability of the Russian labour market are provided by non- enforcement rather than by flexible institutions, and particular wage-setting institutions acting across the economy.

4. What Are Major Implications for Social Protection and Social Cohesion?

What is the resulting pay-off generated by this model? What are ultimate gains and losses produced by this type of labour flexibility? What are particular implications for social security and social cohesion? Based on the discussion presented above we can come up with the following balance sheet. Clearly, this is a very approximate list of outcomes and much remains to be explored. i) On the positive side, the labour market performs unexpectedly well if to judge looking at all major quantitative employment and unemployment indicators. These gains are largely short-or medium run.

The Russian style flexibility helped to weather the storm of the early transition and to avoid mass disemployment. It allowed keeping employment and participation rates high enough while the unemployment has never approached any dramatic levels. This had both economic and social advantages. From the macroeconomic point of view, this helped to ease fiscal pressure; from the social perspective, this stretched adjustment time for individuals and households, allowed them to avoid joblessness, helped to retain social ties and guaranteed minimal income, etc. ii) On the negative side, there are multiple losses, including medium- and long-term. The “Russian style” labour market flexibility does not stimulate economic growth and does not facilitate enterprise restructuring. It proliferates poverty and generates inequality among employed and educated, deprives people formal/institutional social protection, and destroys social cohesion in the society.

The major price paid for maintaining high level of employment is in low average wage. Keeping a low wage employment works as a device that protects formal employment and substitutes for formal unemployment benefits. Low wage job can be supported by moon-lighting activity and engagement into low productivity employment in the informal sector. All this leads to inefficient utilization of the human capital..

Low transparency in the labour market and strong asymmetry in information on jobs and individual productivity turns this information from public good into a private good. Searching for a job or entering a paid employment in this type of the labour market an individual faces high uncertainty since he/she cannot foresee future earnings. This increases individual search and adjustment costs, including moral costs associated with search behaviour, generates voluminous and inefficient churning (short-term job matches), and affects negatively efficiency of labour reallocation.

This type of flexibility devalues formal contracts, which are crucial for the modern economy. The devaluation generates low trust behaviour and creates strong disincentives for investments into specific human capital. Instead of investing in specific human capital, employers prefer to hire job candidates with better general human capital, which is often considered the only reliable labour market signal. This, in its turn, creates wrong incentives for the education system. Linking wages to financial performance and individual bargaining power stimulates high earnings inequality. It clearly rewards individual adjustment and lowers propensity for collective actions, leads to segmentation and atomisation of individuals, and destroys values of solidarity and cohesion. Low tenures and high turnover assume destruction of social cohesion and low solidarity.

The model is bad for achieving economic efficiency as well as for providing social cohesion. It impedes job creation in the formal sector and preserves of obsolete and low productivity\low wage jobs. The total balance-sheet suggests that the partial positive implications of the model have already been exhausted or are close to exhaustion, while the negative ones are going to be at work in the future as well. This means that the acting model has to be replaced or radically reformatted what assumes a strong demand for the comprehensive labour market reform. Such reform is unlikely to be popular and cannot be adopted in a shock therapy style but requires politicians to have strategic vision and long-term horizon.

5. Conclusions: Major Policy Implications

The institutional equilibrium shaping the “Russian style” labour market flexibility is not friendly to economic growth. It allocates major outcomes of the growth with significant social costs. I believe that the institutional framework supporting this style of flexibility deserves to be radically redesigned despite all political costs and risks associated with this reform.

Clearly, much that has to be done is outside the labour market per se. First of all, the economic growth and the restructuring of the economy are crucial preconditions and are conditional upon a wide set of policies and particular measures. The same is true in relation to job creation in the formal sector. At least, the investment climate should be radically improved and this concerns all its multiple dimensions (tax policy and administration, antimonopoly policy, administrative barriers, property rights, etc.).

The major idea of the labour market reform could be in replacing the institutional foundations of pro-low wage - rigid employment policy with institutions that support robust wages – flexible employment policies. The EPL needs further deregulation, while the law and contract enforcement must be radically improved and strengthened. The later assumes strengthening workers’ voice, including activating the role of trade unions, the judicial reform, among other measures. Wage-setting machinery needs to be reformed in order to allow competitive labour market to set wages while individual employers should become price takers but not wage-setters. The minimum wage legislation needs to go through significant reshuffle too. The minimum wage setting should be regionalised and depoliticised, and then minimum wage could be raised in most of the regions. This will bring needed rigidity into wage setting and will contain extra wage flexibility. The wage setting reform will require radical reforms in the budgetary funded sector of the economy, which has been working so far as a wage containing anchor. All this will also bring more transparency into the labour market functioning.

The public employment service (PES) could improve the transparency of the labour market signals but it should focus mainly on collecting and disseminating job vacancies information, and on job brokering and counselling, while emphasis on job training and subsidized employment cannot be efficient under very low job creation and low PES targeting capacity. Given all administrative and financial constraints it would be wrong to expect the PES to deliver much more.

The radical labour market reform involving the EPL deregulation and far going changes in the wage-setting machinery across the economy present a very ambitious agenda. It cannot be realized in one jump and requires well thought-off politics and thoroughly phased policy. However, the urgent need in this type of reform is the major conclusion I can draw from the short analysis presented above. % Fig. 1. Monthly dynamics of employment and real wages in Russia, 1991-2002, January 1991 = 100%

160

150

140

130

120

110

100

90

80

70

60

50

40

30

20

10

0 0 0 1 2 0 1 2 0 1 0 0 1 2 1 2 1 2 0 2 0 1 2 0 1 2 1 2 0 1 2 0 1 2 0 1 2 1 2 3 4 5 6 7 8 9 1 2 3 4 5 6 7 8 9 1 2 3 4 5 6 7 8 9 1 2 3 4 5 6 7 8 9 1 2 3 4 5 6 7 8 9 1 2 3 4 5 6 7 8 9 1 2 3 4 5 6 7 8 9 1 2 3 4 5 6 7 8 9 1 2 3 4 5 6 7 8 9 1 2 3 4 5 6 7 8 9 1 2 3 4 5 6 7 8 9 1 2 3 4 5 6 7 8 9 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1991 1991 1992 1992 1993 1993 1994 1994 1995 1995 1996 1996 1997 1997 1998 1998 1999 1999 2000 2000 2001 2001 2002 2002

Employment in large and mediun size enterprises Real wage