April 2003

INVESTMENT OUTLOOK

Contents

JSE Over/Undervalued Industries

The War in Iraq and your Off-Shore Investments

The Intrinsic Value of JSE Blue Chip Companies

Anglorand Model Portfolio

Dr Gad Ariovich, editor and Chief Investment Officer Contributors: Desmond Esakov, Charl Marais JSE Over/Undervalued Industries

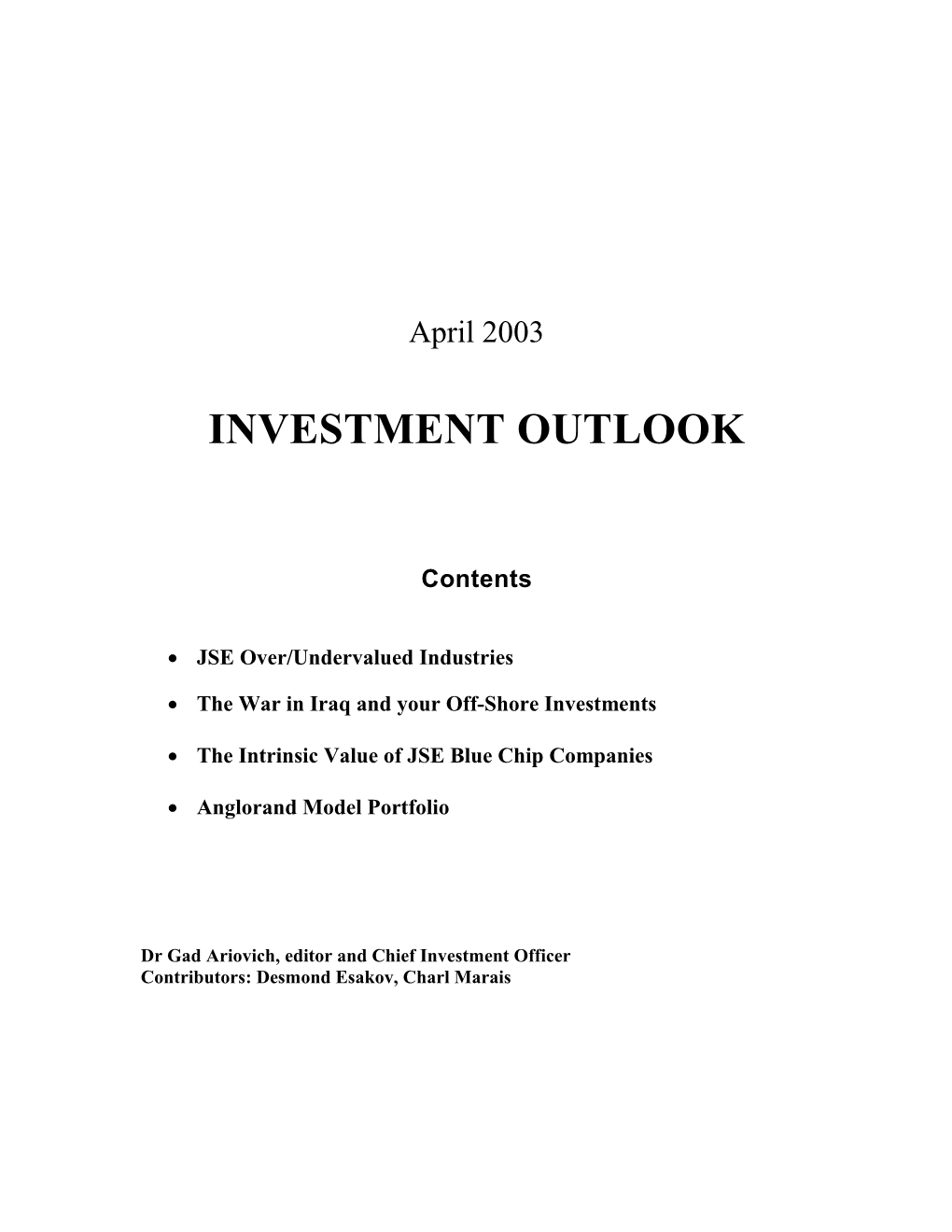

About our models for revealing Over/Undervalued Models on the JSE A series of explanatory factors determining the movements of various JSE sector indices have been selected by statistical analysis. The combined effect of the explanatory variables is defined as the simulated line. The simulated line is then compared to the actual values of the corresponding share price index. If the simulated line is above the actual line, the share index is considered to be undervalued and v.v. (In academic terminology – we have devised factor models for various share price indices)

ALSI Over/Undervalued Situation Industrial Over/Undervalued Situation 20 25

15 20

10 15

10 5 5 0 0 -5 -5 -10 -10

-15 -15

-20 -20 95 96 97 98 99 00 01 02 95 96 97 98 99 00 01 02

According to our proprietary model the JSE - ALSI is The industrial sector is also significantly undervalued. extremely undervalued. This view is also supported by many Fundamentally all looks fine and we believe that it is other indicators (see our Jan/Feb 03 newsletter). We believe negative sentiment that has driven the index down. We from a historical point of view the JSE is at least the most therefore believe that it is now an excellent opportunity to undervalued it has been since the beginning of 1995. start accumulating blue chip industrial companies.

Resources Over/Undervalued Situation Gold Over/Undervalued Situation 60 140

50 120 100 40 80 30 60 20 40 10 20 0 0 -10 -20

-20 -40

-30 -60 95 96 97 98 99 00 01 02 95 96 97 98 99 00 01 02

Resources are also undervalued. With continued negative Gold too is undervalued. Although it remains a little bit of sentiment towards global equity, the JSE resource index has anomaly, the gold price in dollar terms has remained fairly not escaped either. However such tough times can provide stable during the last few months while gold shares have excellent buying opportunities if an investor is prepared to been hammered. It is our opinion that gold shares are adopt a 3 to 5 years investment horizon. It should also be currently offering good value. noted that the resource sector has also been hard hit by the proposed money bill. However we feel that all the bad news is

2 probably discounted in the share prices.

3 Platinum Over/Undervalued Situation Mining Over/Undervalued Situation 50 80 40 60 30

40 20

20 10

0 0 -10

-20 -20

-40 -30 95 96 97 98 99 00 01 02 95 96 97 98 99 00 01 02

Despite the proposed money bill, the strike at Implats and a Like the other resource based industries, the mining industry sharp fall in the palladium price, our proprietary model is also undervalued. We therefore recommend accumulating indicates that the platinum index still remains undervalued. the blue chip shares in the sector such as Anglos. We therefore feel it’s a good opportunity to start accumulating blue chip companies such as Amplats and Implats.

Retail Over/Undervalued Situation Food Over/Undervalued Situation

40 40

30 30

20 20 10 10 0 0 -10

-10 -20

-30 -20

-40 -30 95 96 97 98 99 00 01 02 95 96 97 98 99 00 01 02

The retail industry, in line with many other JSE industries is The food industry is also extremely undervalued. Even also extremely undervalued. It is probably the purchasing during tough and recessionary periods food stocks remain a power of the up and coming black middle class, which will be good defensive play. For the long term investor, one can the engine of growth for the sector. Long term investors can start to accumulate food shares. Our preferred entries are start accumulating retail shares. AVI and Tigerbrands.

4 The War in Iraq and your Off-Shore Investments

The outbreak of the war reduces the degree of uncertainty Financial markets do not like uncertainty and therefore the higher the uncertainty the higher the risk premium demanded by investors. It is therefore no wonder that the outbreak of the Iraqi hostilities have resulted initially in the appreciation of equities around the world.

Figure 1: The behaviour of world equity prices over the last three months

FT World Equity Index

290

270

250

230

210

190 start of war 170

150 2002/03/22 2002/05/21 2002/07/20 2002/09/18 2002/11/17 2003/01/16 2003/03/17

We anticipate a fair degree of price volatility during the war, perhaps in line with the ups and downs of military developments.

The oil price is the single most important global economic factor of the war The single most important business factor of the war from a global point of view is the oil price. It appears that the coalition have already successfully secured major Iraqi oil fields in the south of the country (either Iraq did not have time to destroy its oil installations or it was not its policy to set alight its main source of national wealth). Consequently, the oil price dropped from far above the $30 to around $26 per barrel after the fourth day of the war. It later rebounded to around $27/28 per barrel when the initial euphoria of a very short victory by the allies evaporated.

5 Figure 2: The behaviour of world oil prices over the last three months

Brent Oil: Spot Price Last 3 Months 36

34

32

30

28

26

24 start of war 22

20 2002/12/20 2003/01/09 2003/01/29 2003/02/18 2003/03/10 2003/03/30

Lower oil prices, in the vicinity of $24 to $28 per barrel, will eliminate an important impediment to world economic growth and should reduce negative expectations. If the coalition forces succeed in controlling the major oil fields and maintaining the Iraqi oil production, the oil price will probably drop below $24 per barrel. If the coalition forces maintain regular oil supply to world markets, the price of crude oil may even drop below $20 per barrel. It is worth indicating that many energy experts believe that under normal political and economic conditions, the oil price equilibrium should be around $24 per barrel. As with equities, the oil price will probably fluctuate during the war according to the success of the military developments and the ability of the allied coalition to maintain the oil fields.

Swift victory for the coalition is still probable. No body can predict with any certainty the outcome of a war but it is still probable that this one will end with a swift victory by the coalition forces. We suggest three main scenarios for the outcome of the war in Iraq:

Scenario A: A quick victory for the coalition forces. Under such a scenario, we suggest a war that may take at most 4 to 5 weeks with the coalition forces having less than 500 casualties. By the end of the war, Iraq will go to a rebuilding phase with the assistance of the Americans and the British (who will be keen to show the world what good they can do for the Iraqi people). Lower oil prices plus the intensive rebuilding of Iraq with its oil revenues will be very positive for the health of the world economy, especially, over the next 12 months or so. We attribute a more than 50% probability that this scenario of a quick war will materialize.

Scenario B: Quite a hard won victory for the coalition forces. In line with this scenario the war may take about three months or so with casualties by the coalition forces numbering less than a 1000 soldiers. By the end of the war there will still be a relatively low level of hostile activities but at a bearable rate (of say, between 30 to 50 casualties per year). There will probably be higher tension between most Muslim countries and the West and with the coalition countries in particular. The fear of terrorism in the West and the world in general may be higher. However,

6 should the Iraqi oil supply keep flowing to world markets such a scenario may be at most slightly positive or just neutral to the world economy. In such a case, the oil price will probably not drop below $20 a barrel and it is likely that there will be a premium on the suggested equilibrium price of $24 per barrel. Hence, under such a scenario, world oil prices may be, on the average, in the range of $25 to $30 per barrel. The above war/oil scenario should also be more or less neutral for world equity prices. We attribute about 30% probability to such a scenario,

Scenario C: A long and dirty war which will last for a long time. The strategy of the Iraqi regime is to prolong the war by digging itself in and around Baghdad and having another “Stalingrad type battle” – the famous Russian city which held out against the German onslaught for a lengthy period during the Second World War. Should such a scenario materialize, the current Iraqi regime will probably raise a lot of sympathy among the Arab countries, the Muslim world, big groups of non alliance countries and even support from France, Russia and China . In such a case the war may end in a stalemate and the impact on the world economy will be very bleak, indeed. World equities may take a tumble and so to the US dollar. We attribute a probability of less than 20% to such a scenario.

Implication for your offshore investment The OMG/Anglorand Fund is built for all seasons. The lion’s share of our investment is in certain hedge funds, which tend to weather tough times well. The rest of our money is in cash, which is often regarded as “the king of assets” during financial storms.

Hedging activities enable fund managers to protect investors against risks of price falls of equities, commodities and other financial assets. Certain hedge funds therefore provide diversification and a significant level of capital protection in falling markets. The most common strategy is long/short positions, which involves equity investing on both the long and the short side of the market. Such funds can actually benefit handsomely from bear markets, provided the portfolio managers read the market developments well. Other products, of the so called alternative investments, tend to profit from volatility – some indifferent to the ups and the down trends in prices.

The OMG/ANGLORAND OFFSHORE FUND invests into multi-strategy hedge and alternative funds which provide prudent diversification. The current fund structure provides private clients with access to top performing hedge funds which traditionally are only accessible to institutional clients.

As mentioned several times in our newsletters, we intend gradually building a long equity position in line with the first scenario of a quick end to the war and the very cheap world equity prices now prevailing (with the exception of US equities which we believe are still too expensive).

We also wish to purchase BBB rated bonds of blue chip companies with maturities of 3 to 5 years and a dollar yield of above 6%.

In summary, our fund is well constructed to face the current turmoil. Exceptional times can present exceptional investment opportunities. We will try and turn the current world situation from a threat into an opportunity.

7 The Intrinsic Value of JSE Blue Chip Companies Top Companies Analysis

Forecast Prices Actual Prices * premium /discount %

Anglo 130.67 114.00 -12.76

Billiton 35.75 40.00 11.90

Richemont 8.10 10.56 30.40

Remgro 68.71 52.00 -24.32

Amplats 362.64 240.00 -33.82

Implats 764.85 420.00 -45.09

Sasol 108.51 90.00 -17.06

SAB 62.56 49.55 -20.80

Anglogold 328.32 235.00 -28.42

Goldfields 75.33 83.60 10.98

Old Mutual 21.05 9.90 -52.97

Sanlam 10.53 6.30 -40.16

Standard Bank 41.55 27.30 -34.30

Firstrand 9.80 6.55 -33.15

* Prices as of 1 April 2003

8 Anglorand Model Portfolio Anglorand Model Portfolio - April 2003 JSE Weights Anglorand Sector Shares JSE Weighting Adjusted Weighting

Anglo 16.3 31.8 10.0 Mineral Extractors & Mines Billiton 9.7 18.9 6.0 Mining Finance JCI 0.1 0.2 4.0 Gold Anglogold 4.7 9.2 5.0 Platinum Implats 2.6 5.0 6.0 Oil & Gas Sasol 5.6 10.9 7.0 Chemicals, Oils etc Afrox 0.4 0.8 4.0 Investment Companies Remgro 2.5 4.8 5.0 Banks Firstrand 3.4 6.6 6.0 Insurance Alexforbes 0.4 0.7 3.0 Life Assurance Sanlam 1.6 3.1 4.0 Real Estate Grayprop 0.3 0.5 7.0 Beverages ABI 0.7 1.3 3.0 AVI 0.4 0.8 4.0 Food Producers Illovo 0.2 0.4 3.0 Retail Nuclicks 0.2 0.4 3.0 Household Goods Steinhoff 0.5 0.9 3.0 Pharmaceuticals Aspen 0.2 0.5 4.0 Support Services Bidvest 1.2 2.4 5.0 Electrical Equipment Reunert 0.3 0.7 4.0 IT EOH 0.0 0.0 4.0 Total 51.1 100.0 100.0

Senior Staff David Lewis, CEO; David Palmer, Director, Head Dealer; Adriaan Kamper, Financial Director; Yulindi Taljaard, Compliance Director and Settlements Manager.

The Investment Committee Harold Bernstein, Chairman; Dr Gad Ariovich, Investment Manager; Dr Richard Bonnichsen; Charl Marais; Desmond Esakov.

Anglorand Securities www.anglorand.co.za;

Tel: 011 - 484 7440 Fax: 011 – 484 6647; 3rd Floor, Werksman Chambers, 22 Girton Road, Parktown, 2193.

9