BOARD OF DIRECTORS’ QUALITY INDEX, LARGEST SHAREHOLDER, FIRM CHARACTERISTICS AND VOLUNTARY DISCLOSURE INDEX OF PUBLIC LISTED COMPANIES IN THAILAND Jakkravudhi Chobpichien1 Accounting Curriculum, Faculty of Management Science, Suan Dusit Rajabhat University

ABSTRACT

The study investigates whether board of directors’ quality index (BOQI) as a set of corporate governance characteristics, the largest shareholder, and firm characteristics influence voluntary disclosure index (VDI) of public listed companies in the Stock Exchange of Thailand. The findings suggest that VDI is influenced by the BOQI, the largest shareholder, and firm characteristics of the firm. The higher the BOQI, the higher is the VDI. This relationship is moderated by the largest shareholder controlling ownership as a pure moderator variable. In addition, this relationship appears to be weaker for companies with the largest shareholder who is family member compared to the largest shareholder who is not family member. Finally, firm characteristics comprising return on equity ratio, debt-equity ratio and firm size are found to have a positive significant influence on VDI and that the voluntary disclosure is used a means to reduce information asymmetry and agency problems.

Key words: Positive Agency Theory, Board of Directors, Ownership Structure, Firm Characteristics, Voluntary Disclosure, Thailand.

1. INTRODUCTION The disclosure orientation of companies in Thailand is also greatly influenced by the form of ownership and management structure (Limpaphayom, 2000). Thailand’s listed companies are usually controlled by a family group whose staffs are in the senior positions and also function as the largest shareholder. Thai ownership is highly concentrated and most of the shares are owned by executive directors. As a result, managers and owners are of the same person (Wiwattanakantung, 2000).

1 Corresponding author: Address: 295 Ratchasima Road, Dusit, Bangkok 10300, Thailand. Tel.: +66-0-2244-5780. E-mail address: [email protected]. 2

The board of directors (BOD) of the companies is chosen as it is an important tool to protect shareholders’ assets and to control the management of the company. The board of directors is also the main policy making body, strategic planner, and acts as the authority of the company. In Thailand, the board of directors of most the listed companies on the SET are controlled by the largest shareholders. As a result of this, the interests and participation of the minority shareholders are being undermined. An important tool for the protection of the minority shareholders is the ownership structure in the companies (Limpaphayom, 2000). The pattern of family business persisted even after the firms were listed in the Stock Exchange of Thailand (SET), where neither foreign ownership nor state ownership has ever been prominent since the SET was established in 1975 (Dhnadirek & Tang, 2003). Consequently, family members were often insiders, meaning that they were major shareholders, managers and members of the board of directors, as well as the ones who nominated outside directors. The role of independent directors per se is minimal; usually only two persons are nominated to the board committee simply to fulfill the requirement of the Securities and Exchange Commission (SEC). Furthermore, as firm ownership was dominated by inside shareholders, the outside shareholders (those who did not hold management positions in the firm) would find it difficult to garner sufficient votes to influence or oust incumbent management, hence restricting the role of the market in corporate control (Limpaphayom, 2000). The main objective of this study is to examine the relationship between the board of directors’ quality index (BOQI) and the voluntary disclosure index (VDI) of listed companies in Thailand. The other objective of the study is to investigate whether ownership structure affects the relationship between the level of board of directors’ quality and the level of voluntary disclosure. Under the implicit assumption of positive agency theory, this study hypothesized that improved BOD and ownership structure of Thai public listed companies leads to more voluntary disclosure practices, and the voluntary disclosure practices is used as a means to reduce information asymmetry and agency problems. To examine the relationship between BOD and corporate disclosure behavior in Thailand, with its unique regulatory and relatively non-stringent disclosure requirements as compared to the U.S. and the U.K. However, the findings of Thailand can be generalized to other countries or economies with similar institutional backgrounds as Emerging Capital Markets is understood to mean a stock market located in a developing country. At present, there are 47 countries whose capital markets that are considered ECMs by the International Finance Corporation (IFC, 1994, as cited in Saudagaran and Diga, 1997). 3

The rest of this paper is organized as follows. Section 2 reviews the related literature and proposes hypotheses being tested in Section 3. In Section 4, research design, discusses the sample and data design. Section 5 presents the empirical results and discussion is presented in Section 6. Finally, Section 7 draws some conclusions on the issue.

2. LITERATURE REVIEWS 2.1 Positive Agency Theory, Board of Directors and Corporate Disclosures Positive agency theory as theoretical explanations the relationship between corporate governance mechanisms and voluntary disclosure, under the implicit assumption of Jensen and Meckling’s (1976) positive agency theory, the study hypothesized that an improved quality of the board of directors would lead to more voluntary disclosure practices, and that voluntary disclosure practices are used as a means to reduce information asymmetry and agency problems (Balachandran & Bliss, 2004). Fama and Jensen (1983) found that a higher proportion of independent non-executive directors on the board should result in more voluntary corporate disclosure. They have suggested that once the firm’s capital is widely held, the potential of conflicts between principal and agent is greater than in family-controlled firms. To reduce these conflicts some shareholders, especially institutional ones have forced managers to disclose more corporate information for the accurate evaluation of the firm’s performance. As a result, information disclosure is likely to be more intensive in widely held firms. The prevalence of family- controlled firms listed on a stock exchange, which is the case in the SET, may result in less demand for corporate disclosures (Dhnadirek & Tang, 2003). Consequently, Chau and Gray (2002) found that prevalence of insiders and family-controlled firms is associated with low levels of voluntary disclosures. Jensen (1993) argued that board composition and board leadership structure are associated with voluntary disclosure. Furthermore, Ho and Wong (2001) indicated that the independence of the audit committee has also been found to be a determinant of the level of voluntary disclosure and the percentage of family members on the board do affect the level of voluntary disclosure. In addition, Willekens et al. (2004) in their studies found that governance mechanisms introduced by companies can increase the disclosure of both the financial and non-financial information.

2.2 Agency Theory, Major Shareholder Ownership, and Monitoring The conflict of interest between managers and shareholders (Jensen, 1986) focus on the major shareholder ownership. The study focuses on the role of the largest shareholder 4 controlling ownership rather than that of family, or a major shareholder ownership because not all family or major shareholders are part of the executive management. This means that the family or major shareholders who are not the part of the management may have less influence on the firm’s policies than the insiders. Accordingly, the strength of the relationship with financial reporting will be less (Dhnadirek & Tang, 2003). To reduce the conflict of interest, Jensen (1993) suggested that managers should receive a significant, ownership of shares in their companies, so that they would act more as owners and not use their discretion to maximize their interest at the expense of shareholders. However, Morck et al. (1988) argued that up to a certain level managers with substantial stakes and hence control will become entrenched (pursuing self-interest), because they found it worth while to generate privileges that are not shared, and without being under pressure of monitoring from outside shareholders. In a different context where ownership is coupled with control (that is, ownership is concentrated in the hands of shareholders), the agency problem addresses another type of conflict of interest, that is between the controlling (major) and non-controlling (minor) shareholders. Ownership concentration can be an efficient monitoring mechanism because it is an incentive for major shareholders to bear monitoring costs since they are likely to obtain substantial benefit from active monitoring (Shleifer & Vishny, 1986). However, the problem of minority expropriation may arise when the ownership is concentrated in a specific group, particularly individual/family (Shleifer & Vishny, 1997). Large shareholdings of the major shareholders usually enable them to hold high management positions (they become insiders), in which they can use their positions to exploit corporate assets in order to enhance their self- image and business empire through sales maximization at the expense of profits (Davis & Harveston, 1998), pay themselves excessive salaries and dividends (DeAngelo & DeAngelo, 1985), and recruit family members into management regardless of their professional expertise (Chandler, 1990).

3. HYPOTHESES DEVELOPMENT 3.1 Board of Directors’ Quality and Voluntary Disclosure The relationship between the quality of board of directors and the level of voluntary disclosure of companies has been examined in previous research is as shown in Table 1. “Insert Table 1 about here” 5

According to Willekens et al. (2004) created a corporate governance index which measures the overall the strength of a company’s corporate governance system and that they suggested that higher scores indicate stronger corporate governance systems and predict a positive coefficient on level of corporate governance. This study would like to examine the relationship between the board of directors’ quality index which is associated with the quality of the board’s leadership structure, composition, meetings, controlling system, committees, the audit committee and the remuneration committee and the level of voluntary disclosure and predict the direction of this relationship. Thus, this study hypothesized that:

H1: There is a positive relationship between the level of board of directors’ quality and the level of voluntary disclosure.

3.2 Board of Directors’ Quality, Ownership Structure and Voluntary Disclosure Largest Shareholder Controlling Ownership On the one hand, Black (1992) has noted that the primary value of institutional investor monitoring is in improving corporate boards. Wright (1996) argued that board members with higher levels of shareholdings may be associated with greater levels of influence in the operations of the firm in order to protect their investments. Furthermore, Fan (2004) argued that institutional investors like pension funds (e.g. CULPERS), fund managers and mutual trusts. As their holding is relatively large, they have incentives to monitor and exercise influence over managers of firms they invest in. On the other hand, Berle and Means (1932) and Fan and Wong (2002) as cited in Hope (2003) found that ownership is highly concentrated, the nature of the agency problem shifts away from manager-shareholder conflicts to conflicts between the controlling (major) shareholders and non-controlling (minor) shareholders. Consequently, it is not clear whether on average one would expect the largest shareholder controlling ownership to increase or to reduce the monitoring is in effectiveness of improving corporate boards. This study would like to examine the role of the major shareholders controlling ownership on the relationship of the board of directors’ quality to the level of voluntary disclosure but do not predict the direction of this relationship. Thus, this study hypothesized that:

H2.1: The largest shareholder controlling ownership will moderate the relationship between the level of board of directors’ quality and the level of voluntary disclosure.

The non-executive director, largest shareholder 6

According to Dhnadirek and Tang (2003) argued that the relationship with financial reporting will not necessarily be the same between major shareholder ownership who are not part of management will help to enhance the quality of financial reporting and managerial ownership will be less inclined to provide quality of financial reporting. Furthermore, Albrecht and Sack (2000) found that the growth in pension funds and other institutional investors with a resultant increase in their power to influence businesses. Elliott and Elliott (2005) argued that influence of institutional investors as major shareholders; there are the principles, the governance documents produced by the various institutional investor organizations, e.g. the Association of British Insurers (ABI). The ABI has published a statement of voting policy and corporate governance good namely; ABI members fully support the Principles of Cadbury, Greenbury and Hampel Committees. Furthermore, they are concerned to ensure the appointment of a core of non-executives of sufficient number and of appropriate caliber, experience and independence to identify where there may be undue concentrations of decision-making power not formally constrained by appropriate checks and balances. This study would like to examine the role of the major shareholders who are not part of the management on the relationship of the board of directors’ quality to the level of voluntary disclosure and predict the direction of this relationship. Thus, this study hypothesized that:

H2.2: The non-executive director, largest shareholder will positively moderate the relationship between the level of board of directors’ quality and the level of voluntary disclosure.

The family member, largest shareholder The study by Shleifer and Vishny (1997) found that the problem of minority expropriation may arise when ownership is concentrated in a specific group, particularly individuals/family. Chen and Jaggi (2000) suggested that independent non-executive directors’ independence in family controlled firms may become impaired and consequently their influence on disclosure of comprehensive financial information may be weaker than in non-family controlled firms. In Thailand supported by Dhnadirek and Tang (2003) argued that the business sector has been dominated by Chinese and most companies in Thailand are family owned and family members were often insiders, meaning that they were major shareholders, managers and members of the board of directors, as well as the ones who nominated outside directors. This study would like to examine the role of the major 7 shareholders who are members of a family on the relationship of the board of directors’ quality to the level of voluntary disclosure and predict the direction of this relationship. Thus, this study hypothesized that:

H2.3: The family member, largest shareholder will negatively moderate the relationship between the level of board of directors’ quality and the level of voluntary disclosure. 3.3 Firm Characteristics as Control Variables There has been extensive empirical work relating firm-specific characteristics to the extent of voluntary disclosure based on a number of theoretical arguments for structure- related characteristics which include agency theory, information and political costs, proprietary costs, and capital need such as debt-equity ratio (e.g. Hossain et al., 1995) and firm size (e.g. Cooke, 1989; Haniffa & Cooke, 2002; and Hossain et al., 1995); performance- related characteristics which include legitimacy theory such as liquidity ratio (e.g. Hossain et al., 1994), support continuance and compensation such as rate of return (e.g. Singhvi & Desai, 1971), and signaling theory such as profit margin (e.g. Singhvi & Desai, 1971); and market-related characteristics which include capital need, foreign exchange listing requirements such as scope of business operations (e.g. Hossain et al., 1994), reputation costs and signaling agency costs such as audit firm size influence (e.g. Singhvi & Desai, 1971). In Thailand, there has been extensive empirical work relating firm-specific characteristics to the extent of voluntary disclosure, capital structure, and firm performance namely, structure-related characteristics for example, debt-equity ratio used by Priebjrivat (1992), SET (2001a), and Wiwattanakantang (1999); firm size used by Priebjrivat (1992), SET (2001a), Wiwattanakantang (1999), and Yammeesri and Lodh (2002). Performance- related characteristics for example, profit margin, earnings return, and liquidity ratio used by Wiwattanakantang (1999) and Yammeesri and Lodh (2002). Market-related characteristics for example, scope of business operations used by Wiwattanakantang (1999); audit size influence used by Priebjrivat (1992). Thus, the study used firm-specific characteristics as control variables include the theoretical framework.

4. RESEARCH DESIGN 4.1 Sample This survey covers all of companies (i.e. 456 companies) listed on the Stock Exchange of Thailand (SET) as at 2005 i.e. included 391 listed companies such as Agro and Food Industry Sector 47 companies, Consumer Products Sector 43 companies, Financials Sector 66 companies, Industrials Sector 69 companies, Property and Construction Sector 87 8 companies, Resources Sector 24 companies, Services Sector 84 companies, Technology Sector 36 companies, and excluded 65 listed companies come from data needed for the study not available (example data such audit committee and/or board of directors, and/or ownership or control variables not available and new listed companies).

4.2 Voluntary Disclosure Checklist The study initially combines both the checklist of Meek et al. (1995) and Chau and Gray (2002). Whenever an item appears in either of the study, it will be included in the study’s checklist. Upon completion of this, the study ended up with a total of 115 items in its voluntary disclosure checklist. After this stage, the study then eliminated the items that were mandated by the regulatory requirements of Thailand. This resulted in a voluntary disclosure checklist comprising of 70 items (see Appendix 1). To validate that the checklist did include only voluntary disclosure items, the checklist was subjected to the evaluation of a few Certified Public Accountants in Thailand. They confirmed that the 70 item checklist can be used for the purpose of the study.

Scoring the Voluntary Disclosure Items and Disclosure Index Voluntary Disclosure Index is based on the 70 disclosure items. Scoring and disclosure indexes of the voluntary disclosure items under the unweighted voluntary disclosure index were adopted from Cooke (1989). The additive model used here is unweighted. The implied assumption is that each item of disclosure is equally important. This study is to use a dichotomous procedure in which an item scores one if it is disclosed and zero if it is not disclosed. The total score of voluntary disclosure (Vj) for a company j is additive:

70 Vj = ∑ dij i = 1 Where, j = 1 to 391; i = 1 to 70; dij = 1 if the voluntary disclosure item di is disclosed and 0 if the voluntary disclosure item di is not disclosed for company j; Once all items have been scored an index is created to measure the relative level of disclosure by a company. The index is a ratio of the actual scores awarded to a company to the scores which that company is expected to earn. Consequently, a company is not penalized for those items that are not relevant to it. Thus, the maximum score (Mj) companies can earn varies: 9

nj Mj = ∑ dij i = 1 where, dij = the maximum possible number of voluntary disclosure items expected to be disclosed by a company j; nj = the number of items which a company j is expected to disclosure, i.e. n ≤ 70 for a company j.

The relative the voluntary disclosure index (VDIj) by each company j is measured by an index which is the proportion of the total score of voluntary disclosure (Vj) awarded to a company j to the score which that company j could at most be expected to disclose as the maximum score (Mj). Thus, the voluntary disclosure index score can range from zero to one

(0 ≤ VDIj ≤ 1) to be used in the statistical analyzes.

4.3 Board of Directors’ Quality Index The 11 characteristics of board of directors are used to measure the board of directors’ quality index (BOQI). This study assigns a score of “1” if the characteristic is present and “0” if the characteristic is absent. The study assumes that the higher the score (or the BOQI), the higher is the quality of BOD. The measurement of each of the characteristic is as shown in Table 2. “Insert Table 2 about here” 4.4 Ownership Structure Table 3 provides a summary of the operationalization of the moderating variables selected as well as prior studies. “Insert Table 3 about here”

4.5 Control variables Table 4 provides a summary of the operationalization of the control variables selected as well as prior studies. “Insert Table 4 about here”

4.6 Source of Information Unit of analysis of this study is cross sectional survey research by data collection from secondary data. Secondary data for this study was compiled through annual reports (Form 56- 2), report on the disclosure of additional information (Form 56-1) for the year of 2005, Fact 10

Book of the SET (2005), and listed company information from www.setsmart.com of the Stock Exchange of Thailand (SET).

4.7 Data Analysis A four-step hierarchical regression is used to test the hypotheses. The first step is to test the control variables, the second step 2 is to test the independent variables, the third step is to test the moderating variables and the fourth and final step is to test the interaction terms of BOQI and the moderating variable. The model can be stated as follows:

VDIij = β0 + β1BOQIj + β2MVij + β3BOQIj_MVij + β4PPMj + β5ROEj + β6CRj + β7DEj + β8LSALj + β9LMKTj + β10CONGj + β11BIG4j + εj ………(1) Where: j = Firm indicator (1 – 391); Dependent Variables VDIij = dependent variables (i = 1, 2, 3 and 4); VDI1 = strategic information = DVIA, VDI2 = non-financial information = DVIB, VDI3 = financial information = DVIC and VDI4 = all of voluntary information = DVIT;

Voluntary disclosure index, 0 ≤ VDIij ≤ 1 for company j; Independent Variables

BOQIj = the board of directors’ quality index, 0 ≤ BOQIj ≤ 1 for company j; Moderating Variables

MVjk = moderating variables (k = 1, 2 and 3); MV1=LCON, MV2=LCNE and MV3=FCON for company j;

LCONj = 1 as the largest shareholder controlling ownership if more than 25 percent of their outstanding common shares were held by the largest shareholder, and 0 as the largest shareholder non-controlling ownership if at most 25 percent of their outstanding common shares were held by the largest shareholder for company j; LCNEj = 1 as the largest shareholder who is not an executive director, and 0 as the largest shareholder who is an executive director for company j; FCONj = 1 as the largest shareholder who is a family member, and 0 as the largest shareholder who is not family member for company j; Interaction Terms of Independent variables and Moderator variables (MV)

BOQIj_MVij = Interaction term of BOQI and MVi for company j; Control Variables

PPMj = Income before extraordinary items over net sales for company j; ROEj = IBEX over book value of equity for the beginning of the period for company j; CRj = Current assets over current liabilities for company j; DEj = Long-term debt over book value of common equity for company j; LSALj = Natural logarithm of net sales for company j; LMKTj = Natural logarithm of market capitalization for company j; CONGj = 1 if company is a conglomerate firm; = 0 if company is a non- conglomerate firm for company j; BIG4j = 1 if audit firm size is Big 4; = 0 if audit firm size is non-Big 4 for company j; 11

Parameters β0 = Constant; β1-11 = Coefficients of variables 1 thru 11; and εj = Error term for company j.

5. RESULTS 5.1 Level of Board of Directors Quality Table 5 presents the frequency of board of directors’ quality is first measurement in compliance with the SET’s Code of Best Practice for Directors of Listed Companies, Best Practice Guidelines for Audit Committee, and The Fifteen Principles of Good Corporate Governance of non-financial listed companies in the Stock Exchange of Thailand (SET) 391 companies for the year 2005. “Insert Table 5 about here” 5.2 Descriptive Statistics Table 6 provides descriptive statistics of dependent, independent, control, and moderating variables. “Insert Table 6 about here” 5.3 Correlation Matrix Table 7 provides correlation matrix of control, independent and dependent variables. “Insert Table 7 about here” 5.4 Goodness of Measures In this section describe the study’s voluntary disclosure checklist and provide evidence supporting its reliability. The reliability of measurement in this study was tested using the Cronbach’s alpha (Cronbach, 1951). The instruments, voluntary disclosure checklist items, used in the study were reliable, with coefficients ranging from .64 to .80, which exceeded the minimum acceptance level of .60. According to Liouville and Bayad (1998) used the threshold of .60 to determine strong scale reliability.

5.5 The Hierarchical Regression Results and Discussion Hierarchical Regression Results Table 8 to Table 11 provides hierarchical regression results using control variables, independent variable, and moderating variables in model 2.1, model 2.2 and model 2.3 on the relationship between the board of directors’ quality index and the voluntary disclosure index adjusted for items that are not applicable to the firm. “Insert Table 8 to Table 11 about here” 12

Effects of Control Variables As shown in Table 8 to Table 11, when the eight firm characteristics as control variables were entered into the regression equation in the first step, the coefficient of determination (R2) was found to be .16, .24, .07 and .23 indicating that 16, 24, 7 and 23 percent of the DVIA, DVIB, DVIC and DVIT is explained by the firm characteristics, respectively. It can be observed that control variables such as ROE, DE, LSAL and LMKT (Maximum of Std. Beta = .11, .10, .26 and .34, respectively) showed a significant and positive relationship with VDI at the .05, .05, .01 and .01 level, respectively. These results provided support for ROE, DE, LSAL and LMKT and not support for PPM, CR, CONG, and BIG4 of the study.

Effect of Board of Directors’ quality index (BOQI) In step 2, by adding the one independent variable, R2 increased to 18, 24, 7 and 24 percent, respectively. This R2 change (.02, .01 and .01) is significant for DVIA, DVIB and DVIT. This implies that the additional 2, 1 and 1 percent of the variation in DVIA, DVIB and DVIT is explained by BOQI. BOQI (Std. Beta = .16, .10 and .11) was found to have a significant and positive relationship with DVIA, DVIB and DVIT at the .01, .05 and .05 level of significance, respectively. These results provided support for Hypothesis 1 of the study.

Moderating Effects of LCON, LCNE, and FCON In the third step of Model 2.1, 2.2 and 2.3, LCON, LCNE and FCON were entered into the equation in order to gauge its impact as an independent predictor. The maximum R2 increased from 18, 24, 7 and 24 percent to 19, 25, 7, and 25 percent indicating a change of 1, 1, 0, and 1 percent respectively, which is significant (p < .05) for FCON. In the fourth and final step of Model 2.1, 2.2 and 2.3, when the interaction term was entered into the Model 2.1, 2.2 and 2.3, it can be seen that it yielded a significant F Change of 4.20, and the additional variance explained by the interaction term is 1 percent for LCON. This indicates that only one type of ownership structure namely, the largest shareholder controlling ownership moderate the relationship of board of directors’ quality index and voluntary disclosure index. The type of ownership is a Pure Moderator Variable2. The results derived from the final step provided support for Hypothesis 2.1 of the study which predicts that the largest shareholder controlling ownership will moderate the relationship between the

2 A pure moderator variable; that is, psychometrically, a moderator variable should enter into interaction with predictor variables while having a negligible correlation with the criterion itself (Cohen & Cohen, 1975 as cited in Sharma et al., 1981). 13 level of board of directors’ quality and the level of voluntary disclosure as non-financial information. The result of the significant interaction is presented in Figure 1. “Insert Figure 1 about here”

6. DISCUSSION 6.1 Level of the Board of Directors’ Quality The study found that the level of the board of directors’ quality is 40%. Using SET’s Study (SET, 2003) on good corporate governance characteristics of public listed companies in Thailand’s rating as a guideline, that is “very high” to be more than 80 percent, “high” to be between 70 to 80 percent, “medium” to be 60 to 70 percent, “low” to be between 50 to 60 percent and “very low” to be less than 50 percent, the level of BOD’s quality found in this study can be said to be at a “very low level”.

6.2 Level of Voluntary Disclosure From Wallace (1988) rate the levels of voluntary disclosure as “ high” if score is more than 50%, “medium” if score is between 30% and 50% and “ poor” if score is less than 30%. The study found that the level of voluntary disclosure such as strategic information was 44%, non-financial information was 20%, financial information was 40% and all of voluntary information was 33%. Using Wallace’s study as a guideline, the level of voluntary disclosure in Thailand can be said to be at a “medium”, “low”, “medium” and “medium” level, respectively.

6.3 Board of Directors’ Quality Index and Voluntary Disclosure Index The study found that the higher the level of board of directors’ quality is the higher the level of voluntary disclosure such as strategic information, non-financial information and all of voluntary information. The results are consistent with Willekens et al. (2004) that internal governance mechanisms as board of directors can aid in enhancing corporate voluntary disclosure, and that voluntary disclosure is used as a means to reduce information asymmetry and agency problems.

6.5 Moderating Effect of Largest Shareholder Controlling Ownership (LCON) The study found that LCON moderate the relationship between BOQI and VDI. However, in step 4 of Table 9 of this study shown that BOQI not significant but interaction term between BOQI and LCON significant at .05 level. This finding that LCON can would be effect to positive and negative on BOQI. This finding is supported by Shleifer and Vishny 14

(1986) that ownership concentration can be an efficient monitoring mechanism because it is an incentive for major shareholders to bear monitoring costs since they are likely to obtain substantial benefit from active monitoring. This means that major shareholders who are not the part of management may have less influence on the firm’s policies than insiders (Jensen, 1986). This means that the problem of minority expropriation may arise when ownership is concentrated in a specific group, particularly individual/family (Shleifer and Vishny, 1997). In this study, controlling ownership is said to exist if more than 25% of their outstanding common shares were held by the largest shareholder. Thus, the largest shareholder controlling ownership has effect on the relationship of BOQI and VDI.

6.6 Moderating Effect of the non-executive director, largest shareholder (LCNE) The study found that LCNE not moderate the relationship between BOQI and VDI. This finding is supported by Shleifer and Vishny (1986) and Dhnadirek and Tang (2003) that the relationship with financial reporting will not necessarily be the same between major shareholder ownership and managerial ownership (Dhnadirek and Tang, 2003) that the study found that major shareholders who are not the part of management may have less influence on the firm’s policies than insiders (Jensen, 1986). This means that the problem of minority expropriation may arise when ownership is concentrated in a specific group, particularly individual/family (Shleifer and Vishny, 1997). Thus, the largest shareholder who is not an executive director would not help the managers to better manage the company and thus will not have a positive impact on the relationship of BOQI and VDI.

6.7 Moderating Effect of the family member, largest shareholder (FCON) This study found that family members as executive directors and outside non- executive directors have a direct negative effect on the all of voluntary information. This finding is supported by Limpaphayom (2000) that family members were often insiders, meaning that they were chairman, managers and members of the board of directors, as well as the ones who nominated outside non-executive directors. The role of outside non-executive directors per se is minimal as firm ownership was dominated by family members, the outside non-executive directors (those who did not hold management positions in the firm) would find it difficult to garner sufficient votes to influence or oust incumbent management, hence restricting the role of the market in corporate control. This finding is supported by Shleifer and Vishny (1997) and Chen and Jaggi (2000) that the ratio of independent non-executive directors on corporate boards is positively associated with the corporate disclosures, and this association appears to be weaker for family 15 controlled firms compared to non-family controlled firms. Further, Hill (1999) argued that no one single mechanism is a governance panacea and suggests that it is desirable to have a system of overlapping checks and balances for the behaviors of controlling shareholders and at least one family member is related to an executive director. Thus, the largest shareholder who is a family member, it becomes more difficult for shareholders to control who is their family member and thus can has the negative effect on the voluntary disclosure index.

6.8 Impact of control variables on the level of voluntary disclosure Return on equity ratio, debt-equity ratio and firm size influence as expected are positively significantly associated with disclosure levels. This higher return on equity ratio, higher debt-equity ratio and higher firm size tend to exhibit higher disclosures. This might indicate that increased level of voluntary disclosure is driven by increased return on equity ratio, debt-equity ratio and firm size. This finding is consistent with Chen and Jaggi (2000), Cooke (1989), Haniffa and Cooke (2002), Hossain et al. (1995) and Singhvi and Desai (1971).

7. CONCLUSIONS This study extends the previous literature by examining voluntary disclosure in a developing country, namely Thailand. The study investigates whether board of directors, ownership structure, and firm characteristics influence the voluntary disclosure index in the annual reports of 391 public listed companies on the SET in 2005. These are the study highlights of the overall contribution on the whole body of research in positive agency theory which this study contributes to practice in voluntary disclosure checklist for the extent of level of voluntary disclosure. Thus the proposed framework was ownership structure moderate the relationship between board of directors and voluntary disclosure substantially validated. These results supports that the major shareholders who are family members and executive directors are of the same person, ownership is highly concentrated, and the board of directors of most listed companies in Thailand are mostly controlled by the largest shareholder. When, ownership is highly concentrated, the nature of the agency problem shifts away from manager-shareholder conflicts to controlling-non-controlling shareholders conflicts and type of shareholder conflicts between the family-non-family members, largest shareholder. Furthermore, this study assists Hill’s argument (1999) that no one single mechanism is a governance panacea and suggests that it is desirable to have a system of 16 overlapping checks and balances for the behaviors of companies with the family member, largest shareholder. Finally, the control variables comprising return on equity ratio, debt-equity ratio and firm size were found to have a significant influence on the level of voluntary disclosure.

REFERENCES

Albrecht, W.S., & Sack, R.J. (2000). Accounting education: Charting the course through a perilous future. Accounting education series, Volume No. 16. Sarasota, FL: American Accounting Association. Balachandran, J., & Bliss, M. (2004). Board independence and voluntary disclosure: Evidence from Malaysia. Working Paper, Department of Accountancy City University of Hong Kong. Berle, A.A., & Means, G.C., Jr. (1932). The modern corporation and private property. Macmillan, New York. Black, B.S. (1992). Agents watching agents: The promise of institutional investor voice. UCLA Law Review, 39, 811-893. Chandler, A.D. (1990). Scale and scope: The dynamics of industrial capitalism (Cambridge, MA: Harvard University Press). Chau, G.K., & Gray, S.J. (2002). Ownership structure and corporate voluntary disclosure in Hong Kong and Singapore. The International Journal of Accounting, 37, 247-265. Chen, C.J.P., & Jaggi, B. (2000). The association between independent non-executive directors, family control and financial disclosures. Journal of Accounting and Public Policy, 19(4-5), 285-310. Cohen, J., & Cohen, P. (1975). Applied multiple regression/correlation analysis for the behavioral sciences. Hillsdale, New Jersey: Lawrence Erlbaum Associates. Cooke, T.E. (1989). Voluntary corporate disclosure by Swedish companies. Journal of International Financial Management and Accounting, 1(2), Summer, 171-195. Cronbach, L.J. (1951). Coefficient alpha and the internal structure of tests. Psychometrika, 16(3), 297-334. Davis, P.S., & Harveston, P.D. (1998). The influence of the family on the family business succession process: A multi-generational perspective. Entrepreneurship Theory and Practice, 22, 31-53. DeAngelo, H., & DeAngelo, L. (1985). Managerial ownership of voting rights: A study of public Corporations with dual classes of common stock. Journal of Financial Economics, 14, 33-69. Dhnadirek, R., & Tang, J. (2003). Corporate governance problems in Thailand: Is ownership concentration the cause? Asia Pacific Business Review, 10(2), 121-138. 17

Elliott, B., & Elliott, J. (2005). Financial accounting and reporting. Ninth Edition, Prentice Hall Financial Times. Eng, L.L., & Mak, Y.T. (2003). Corporate governance and voluntary disclosure. Journal of Accounting and Public Policy, 22, 325-345. Evans, M. (2004). Board characteristics, firm ownership and voluntary disclosure. Working Paper, Fuqua School of Business, Duke University, Durham, NC. 27708, October. Fama, E.F., & Jensen, M.C. (1983). Separation of ownership and control. The Journal of Law and Economics, 26(2), 301-325. Fan, J.P.H., & Wong, T.J. (2002). Corporate ownership structure and the informativeness of accounting earnings in East Asia. Journal of Accounting and Economics, 33(3), 401-425. Fan, P.S. (2004). Review of literature & empirical research on corporate governance. MAS Staff Paper No. 29, The Monetary Authority of Singapore. Field, A. (2000) Discovering Statistic Using SPSS for Windows. London: Sage. Gul, F.A., & Leung, S. (2004). Board leadership, outside directors’ expertise and Voluntary corporate disclosures. Journal of Accounting and Public Policy, 23, 351-379. Haniffa, R.M., & Cooke, T.E. (2002). Culture, corporate governance and disclosure in Malaysian corporations. ABACUS, 38(3), 317-349. Hill, J.G. (1999). Deconstructing sunbeam-contemporary issues in corporate governance. University of Cincinnati Law Review, 67, 1099-1127. Ho, S.S.M., & Wong, K.S. (2001). A study of the relationship between corporate governance structures and the extent of voluntary disclosure. Journal of International Accounting Auditing & Taxation, 10, 139-156. Hope, O.K. (2003). Analyst following and influence of disclosure components, IPOs and ownership concentration. Asia-Pacific Journal of Accounting and Economics, 10(2), 117-141. Hossain, M.A., Perera, M.H.B., & Rahman, A.R. (1995). Voluntary disclosure in the annual reports of New Zealand companies. Journal of International Financial Management and Accounting, 6(1), 69-87. ____., Tan, L.M., & Adams, M. (1994). Voluntary disclosure in an emerging capital market: Some empirical evidence from companies listed on the Kuala Lumpur Stock Exchange. The International Journal of Accounting, 29(4), 334-351. IFC (International Finance Corporation). (1994). Emerging stock markets factbook 1994. Washington, D.C.:IFC. Jensen, M.C. (1986). Agency costs of free cashflow, corporate finance, and takeovers. American Economic Review, 76, 323-329. ____. (1993). The modern industrial revolution, exit, and the failure of internal control systems. The Journal of Finance, 48(3), 831-880. ____., & Meckling, W.H. (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3, October, 305- 360. 18

Karamanou, I., & Vafeas, N. (2005). The association between corporate boards, audit committees, and management earnings forecasts: An empirical analysis. Journal of Accounting Research, 43(3), 453-486. Limpaphayom, P. (2000). Corporate governance in Thailand before the crisis: Issues and implications. Accountants’ Journal, 47(1), 10-20. Liouville, J., & Bayad, M. (1998). Human resource management and performances: Proposition and test of a casual model. Human Systems Management, 17(3), 183-193. Mangena, M., & Pike, R. (2005). The effect of audit committee shareholding, financial expertise and size on Interim financial disclosures. Accounting and Business Research, 35(4), 327-349. Meek, G.K., Roberts, C.B., & Gray, S. (1995). Factors influencing voluntary annual report disclosures by US, UK and continental European multinational corporations. Journal of International Business Studies, 26(3), 555-572. Morck, R., Shleifer, A., & Vishny, R. (1988). Management ownership and market valuation: An empirical analysis. Journal of Financial Economics, 20, 293-316. Priebjrivat, A. (1992). Corporate disclosure: A case of Securities Exchange of Thailand. Unpublished Doctoral Dissertation, New York University, School of Business Administration. University Microfilms International, Order No. 9220538. Saudagaran, S.M., & Diga, J.G. (1997). Financial reporting in emerging capital Markets: Characteristics and policy issues. Accounting Horizons, 11(2), June, 41-64. SET (Stock Exchange of Thailand). (1999a). Best practice guidelines for the audit committee. Internet site: http://www.set.or.th/en/regulations/corporate/ download/bestace_upd.doc. ____. (1999b). Code of best practice for directors of listed companies. Internet site: http://www.set.or.th/en/regulations/corporate/download/code2e.doc. ____. (2001). The 15 principles of good corporate governance. Internet site: http://www.set.or.th/en/regulations/corporate/download/CG15-ENG.pdf. ____. (2001a). The determinants of audit committee independence: Evidence from audit committee formation in Thailand. Internet Site: http://www.fma.org/zurich/ papers/140140.pdf. ____. (2003). Good governance assessment of listed companies. Corporate Governance Center the Stock Exchange of Thailand, October, Internet Site: http://www.set.or.th/en/regulations/corporate/download/bj46_48_e.zip. ____. (2006). The stock market in Thailand: Fact book 2006. Bangkok: JST Publishing, June. Sharma, S., Durand, R.M., & Gur-Arie, O. (1981). Identification and analysis of moderator variables. Journal of Marketing Research, XVIII, August, 291-300. Shleifer, A., & Vishny, R.W. (1986). Large shareholders and corporate control. Journal of Political Economy, 94, 461-488. ____., & Vishny, R.W. (1997). A survey of corporate governance. Journal of Finance, 52, 737-783. 19

Singhvi, S.S., & Desai, H.B. (1971). An empirical analysis of the quality of corporate financial disclosure. The Accounting Review, 46(1), January, 129-138. Vafeas, N. (1999). Board meeting frequency and firm performance. Journal of Financial Economics, 53(1), 113-142. ____., & Theodorou, E. (1998). The relationship between board structure and firm performance in the U.K. The British Accounting Review, 30, 383-407. Wallace, R.S.O. (1988). Corporate financial reporting in Nigeria. Accounting and Business Research, 18(72), Autumn, 352-362. Willekens, M., Vander Bauwhede, H., Gaeremynck, A., & Van de Gucht, L. (2004). The impact of internal and external governance mechanisms on the voluntary disclosure of financial and non-financial performance. Working Paper, Internet site: http://www.business.uiuc.edu/accountancy/research/vkzcenter/ conferences/gottingen/papaers/willekens.pdf. Wiwattanakantang, Y. (1999). An empirical study on the determinants of the capital structure of Thai firms. Pacific-Basin Finance Journal, 7, 371-403. ____. (2000). The equity ownership structure of Thai firms. Unpublished Working Paper, Institute of Economic Research, Hitotsubashi University, Japan. Wright, D. (1996). Evidence on the relation between corporate governance characteristics and the quality of financial reporting. Working Paper Series, University of Michigan. Internet site: http://papers.ssrn.com/sol3/Delivery.cfm/ 99042606.pdf. Yammeesri, J., & Lodh, S.C. (2002). The effects of ownership structure on firm performance: Evidence from Thailand. Hawaii International Conference on Business. 20 20

Table 1 Summary of the literature relating corporate governance mechanisms to extent of voluntary disclosure No. Author Respondent Used Location and Other Independent Variable Dependent Variable Items Main Results Independent Variable Items (s) and Control Variable (s) 1. Balachandran & Bliss Annual reports Malaysia, Control Variables Voluntary disclosure Index Significant influence (2004) (2001) 3 items such as: (7 items) such as: (66 items) such as: (p-values less than the .05 (1) CEO duality, 1. Audit size influence 1. General corporate cutoff) such as: (2) Proportion of 2. Current ratio information (10 items) (1) CEO duality, independent non-executive 3. Assets-in-place ratio 2. Financial overview (2) proportion of directors on the audit 4. Firm size (13 items) independent non-executive committee, and (market capitalization) 3. Research and directors on the audit (3) Proportion of 5. Leverage ratio development (4 items) committee, and independent non-executive 6. ROE 4. Future prospect (3) proportion of directors on the board of 7. Foreign listing status (12 items) independent non-executive directors. 5. Employee information directors on the board of (11 items) directors. 6. Social reporting and value-added information (14 items) 7. Capital market data (2 items) 2. Eng & Mak Annual reports Singapore, Control Variables Voluntary disclosure Index Significant influence (2003) (1995) 5 items such as: (12 items) such as: (42 items) such as: (p-values less than the .05 (1) managerial ownership, 1. Growth opportunities 1. Strategic information cutoff) such as: (2) existence of government 2. Market to book value of (22 items) (1) managerial ownership, ownership, assets 2. Key non-financial (2) existence of government (3) government ownership, 3. Market to book value of information ownership, (3) government (4) board composition equity (4 items) ownership, and (measured by the proportion 4. Price-earnings ratio 3. Financial information (4) board composition of outside directors on the 5. Firm size (market (16 items) (measured by the proportion board), capitalization) of outside directors on the (5) blockholder ownership. 6. Leverage ratio board). 7. Regulated industries 8. Audit size influence Not Significant influence (p- 9. Analyst tracking values less than the .05 10. Stock return, 11. ROE cutoff) such as: 12. ROA (1) blockholder ownership. 21

Table 1 (Continued) No. Author Respondent Used Location and Independent Other Independent Variable (s) Dependent Variable Items Main Results Variable Items and Control Variable (s) 3. Evans Annual reports, 10-Ks, and USA, Control Variables Voluntary disclosure scores Not Significant influence (2004) proxy statements 8 items such as: (6 items) such as: (24 items) such as: (p-values less than the .05 (2001) (1) board size, 1. Firm size (net sales) 1. Summary of historical cutoff) such as: (2) board independence, 2. Growth opportunities results (1) board size, (3) audit committee 3. ROA (7 items) (2) board independence, independence, 4. Analyst following 2. Other financial measures (3) audit committee (4) CEO / chairman 5. Firm complexity (3 items) independence, duality, 6. Industry type 3. Non-financial measures (4) CEO / chairman duality, (5) number of board (7 items) (5) number of board meetings, 4. Projected information for meetings, (6) audit committee company as a whole (7 (6) audit committee meetings, items) meetings, (7) extent of managerial (7) extent of managerial ownership, and ownership, and (8) extent of institutional (8) extent of institutional ownership. ownership. 4. Gul & Leung Annual reports Hong Kong, Moderating variable (1 item): Voluntary disclosure index Significant influence (2004) (1996) 1 item such as: 1. Proportion of experts outside (43 items) such as: (p-values less than the .05 (1) CEO duality directors on the board 1. Background cutoff) such as: information (11 items) (1) CEO duality, Control variables (14 items): 2. Financial performance (2) Interaction term between 1. SIC industry dummy Information (18 items) CEO duality and Proportion variables 3. Non-financial of experts outside directors 2. Firm size (total assets) Information (14 items) on the board (Type of 3. Director’s ownership Moderator is Quasi 4. Debt-equity ratio moderator) 5. Current ratio 6. Return on equity 7. Audit firm is Big5 8. Audit committee existence 9. Ratio of market value to book value of equity 10. Multiple listing status 11. Consolidated enterprise 12. Issues new share capital 13. Net income is negative 14. Equity market liquidity 22

Table 1 (Continued) No. Author Respondent Used Location and Other Independent Variable Dependent Variable Items Main Results Independent Variable Items (s) and Control Variable (s) 5. Haniffa & Cooke Annual reports Malaysia, Other Independent Variables Voluntary disclosure scores Significant influence (2002) (1995) 7 items such as: (19 items) such as: (65 items) such as: (p-values less than the .05 (1) family members on the A. Corporate Characteristics 1. General corporate cutoff) such as: (1) family board, 1. Firm size (total assets) information (6 items) members on the board, and (2) chairperson is non- 2. Asset-in-place ratio 2. Information about (2) Chairperson is non- executive director, 3. Industry type directors (6 items) executive director. (3) board composition, 4. Listing age 3. Corporate strategy (4) directors with cross- 5. Complexity of business (7 items) Not Significant influence (p- directorships, 6. Level of diversification 4. Capital market data values less than the .05 (5) role duality, 7. Multiple listing status (7 items) cutoff) such as: (6) finance director on the 8. Foreign activities 5. Research and (1) board composition, board, 9. Ownership structure development (1 item) (2) directors with cross- (7) chairperson with cross- 10. Profitability (ROE) 6. Future prospects directorships, directorships. 11. Type of auditors (7 items) (3) role duality, 12. Debt-Equity ratios 7. Social reporting and (4) finance director on the value-added board, and B. Personal information (18 items) (5) Chairperson with cross- Characteristics 8. Financial review directorships. 1. Race of chairperson information (13 items) 2. Race of managerial director 3. Race of finance director 4. Racial ownership structure 5. Racial composition of directors on board 6. Qualification of directors 7. Qualification of finance director 23

Table 1 (Continued) No. Author Respondent Used Location and Other Independent Dependent Variable Items Main Results Independent Variable Items Variable(s) and Control Variable(s) 6. Ho & Wong Annual reports (1997) and Hong Kong, Control Variables Important voluntary disclosure Significant influence (2001) Chief financial officers 4 items such as: (5 items) such as: 20 items perceived by financial (p-values less than the .05 (CFOs): conduct to (1) Existence of an audit 1. Firm size (total assets) analysts such as: cutoff) such as: determine the existence of committee, 2. Debt-Equity ratios 1. Future prospect, (1) Existence of an audit an audit committee (late (2) proportion of family 3. Assets-in-place ratio 2. Description of products and committee, and 1997 and early 1998) members on board. 4. ROE service, 3. China business (2) proportion of family (3) proportion of independent 5. Industry type review, 4. Sales and marketing members on board. non-executive directors, and network, 5. Acquisition and (4) existence of dominant disposal activities, 6. Details of Not Significant influence personalities (CEO duality). investments, 7. Corporate (p-values less than the .05 strategy, 8. Factors affecting cutoff) such as: future financial results, (1) proportion of independent 9. Financial ratios, 10. Bank non-executive directors, and loans, 11. Capital expenditure, (2) existence of dominant 12. Financial position, personalities (CEO duality). 13. Financial summary, 14. Main product market share, 15. Stock price, 16. Details of operating expenses, 17. Product contribution margin, 18. Aging of debtors’ balance, 19. Cost of goods sold, 20. Cash flow forecast 24

Table 1 (Continued) No. Author Respondent Used Location and Other Independent Dependent Variable Items Main Results Independent Variable Items Variable(s) and Control Variable(s) 7. Karamanou & 1,621 annual reports US, Control Variables Voluntary financial disclosure Significant influence Vafeas (1995-2000) of 9 items such as: (8 items) such as: practices (p-values less than the .05 (2005) 275 listed companies in the (1) Board of directors: (1) Bad news, such as: cutoff) such as: 1995 Fortune 500 (1.1) Pct. of outside (2) Annual forecast, Equals 1 if the firm issues a (1) Board of directors: directors, (3) Forecast dispersion, management forecast as (1.1) Pct. of outside (1.2) Board size, (4) Analyst following, voluntary financial disclosure directors, (1.3) Board meetings, (5) High-tech industry, practices in the current year as (1.2) Board size, (1.4) Insider ownership, (6) Days to end of well, 0 otherwise (1.3) Board meetings, (1.5) Institutional ownership financial reporting period, (1.4) Insider ownership, (2) Audit committee: (7) Forecast update, (1.5) Institutional ownership (2.1) Pct. of committee (8) Log (Total assets) (2) Audit committee: outsider, (2.1) Pct. of committee (2.2) Pct. committee outsider, members with financial (2.2) Pct. committee expertise, members with financial (2.3) committee size, expertise, (2.4) committee meetings (2.3) committee size, (2.4) committee meetings 8. Willekens, Annual reports and Belgium, Control Variables Balance scorecard disclosure Significant influence Vander Bauwhede, Chairman of the board of 4 items such as: (6 items) such as: index (25 items) such as: (p-values less than the .05 Gaeremynek & directors (2001 and follow- (1) Corporate Governance 1. Board size 1. Perspectives (5 perspectives cutoff) such as: Van De Gucht up mailing in January 2002) Index 2. Leverage ratio of each company reports (1) Corporate Governance (2004) (2) each one of these CG 3. Listing age information) such as financial, Index, index: 4. Firm size (total assets) customers, innovation, (2) board independence, (2.1) board independence, 5. ROA production, and learning and (3) external audit quality, and (2.2) external audit quality, 6. Industry type growth. (4) internal audit department (2.3) internal audit 2. Company reports information existence. department existence, 5 items such as quantitative (2.4) audit committee historic information, qualitative Not Significant influence existence. historic information, segment (p-values less than the .05 information, quantitative cutoff) such as: forward-looking information, (1) audit committee and qualitative forward-looking existence. information. 25

Table 2 Measurement of Independent Variable Quality of Board of Directors as Measurement of Board of directors’ quality of board and board’s committees (i.e. audit committee quality index (BOQI) and code and and remuneration committee) in compliance with the SET’s principle is used. Examples of prior studies are used. Code of Best Practice for Directors of Listed Companies (1999), Assign score: If comply score 1, Best Practice Guidelines for Audit Committee (1999), and Non-compliance score 0. The Principles of Good Corporate Governance(2001) Total scores = 10 scores. 1. Quality of Board’s Leadership Structure The titles and authority of the board’s chairman and head of Comply with No.9 of the Principles of (e.g. Evans, 2004) management team are clearly separated (BCEO) Good Corporate Governance score 1, Non-compliance score 0 2. Quality of Board’s Composition More than half of the directors on the board are INDs (BI51) Comply with No.8 of the Principles of (e.g. Karamanou & Vafeas, 2005; Good Corporate Governance score 1, Vafeas, 1999; and Willekens et al., Non-compliance score 0 2004) 3. Quality of Board’s Meetings All directors to attend every board meetings (BMAL) Comply with No.11 of the Principles of (e.g. Evans, 2004; Karamanou & Good Corporate Governance score 1, Vafeas, 2005; and Vafeas, 1999) Non-compliance score 0 4. Quality of Board’s Controlling System and Internal Audit Internal audit department is in company (BIAD) Comply with No.13 of the Principles of (e.g. Willekens et al., 2004) Good Corporate Governance score 1, Non-compliance score 0 5. Quality of Board’s Committees AC and RC are established existence (ACRC) Audit committee (AC) and Remuneration (---) committee (RC) are established in compliance with No.13 of the Principles of Good Corporate Governance score 1, Non-compliance score 0 6. Quality of AC’s Leadership Structure The chairman of AC is an IND (ACCI) Comply with No.12 of the Principles of (e.g. Haniffa and Cooke, 2002) Good Corporate Governance score 1, Non-compliance score 0 26

Table 2 (Continued) Quality of Board of Directors as Measurement of Board of directors’ quality of board and board’s committees (i.e. audit committee quality index (BOQI) and code and and remuneration committee) in compliance with the SET’s principle is used. Examples of prior studies are used. Code of Best Practice for Directors of Listed Companies (1999), Assign score: If comply score 1, Best Practice Guidelines for Audit Committee (1999), and Non-compliance score 0. The Principles of Good Corporate Governance(2001) Total scores = 11 scores. 7. Quality of AC’s Composition At least three AC members are INDs (IDAC) Comply with No. 3.1 of Best Practice (e.g.Ho & Wong, 2001; Karamanou Guidelines for Audit Committee score 1, & Vafeas, 2005; and Willekens et al., Non-compliance score 0 2004) 8. Quality of AC’s Meetings All AC members to attend every AC meetings (ACMA) Comply with No.11 of the Principles of (e.g., Evans, 2004; Karamanou & Good Corporate Governance score 1, Vafeas, 2005; and Non-compliance score 0 Liu, 2004) 9. Quality of AC’s Knowledge and Expertise At least one AC member is a financial reporting expert as CPA (ACEX) Comply with No. 3.3 of Best Practice (e.g. Karamanou & Vafeas, 2005; and Guidelines for Audit Committee score 1, Mangena & Pike, 2005) Non-compliance score 0 10. Quality of RC’s Leadership Structure The chairman of RC is an IND (RCCI) Comply with No.12 of the Principles of (e.g. Haniffa and Cooke, 2002) Good Corporate Governance score 1, Non-compliance score 0 11. Quality of RC’s Composition More than half of the RC members are non-executive directors (RCPR) Comply with No.12 of the Principles of (e.g. Vafeas and Theodorou, 1998) Good Corporate Governance score 1, Non-compliance score 0 27

Table 3 Summary of the operationalization of the moderating variables Construct Operationalization of Expect Operationalization of Previous studies ed This study Sign 1. The largest The dummy variable is set + / - The dummy variable is set to be shareholder to be one for the percentage one for the percentage of stock controlling of stock owned by the owned by the largest shareholder ownership largest shareholder at least at least 25 percent. The dummy (LCON) 25 percent variable is set to be zero for the (Wiwattanakantung, 2000). percentage of stock owned by the largest shareholder less than 25 percent. 2. The non- A family controlled if 10 + The dummy variable is set to be executive percent or more of their one for the largest shareholder director, outstanding common shares who is non-executive director. largest were held by a family and at The dummy variable is set to be shareholder least one family member zero for the largest shareholder (LCNE) was on the corporate board who is an executive director. (Chen & Jaggi, 2000). 3. The family A family controlled if 10 - The dummy variable is set to be member, percent or more of their one for the largest shareholder largest outstanding common shares who is a family member. The shareholder were held by a family and at dummy variable is set to be zero (FCON) least one family member for the largest shareholder who is was on the corporate board non-family member. (Chen & Jaggi, 2000).

Table 4 Summary of the operationalization of control variables 28

Construct Operationalization Expected Prior Studies used as Sign control variables a. Characteristics related to performance PPM Profit margin = income before + Chen & Jaggi (2000) extraordinary items (IBEX) to net sales ROE Return on equity ratio = IBEX to + Balachandran & Bliss book value of equity for the (2004), beginning of the period Chen & Jaggi (2000), Eng & Mak (2003), Gul & Leung (2004), Ho & Wong (2001) CR Liquidity ratio = current assets to + Balachandran & Bliss current liabilities (2004), Chen & Jaggi (2000), Gul & Leung (2004) b. Characteristics related to structure DE Debt-equity ratio = long-term liability + Balachandran & Bliss to book value of common stocks (2004), Chen & Jaggi (2000), Eng & Mak (2003), Gul & Leung (2004), Ho & Wong (2001), Willekens et al. (2004) LSALE Firm size = natural logarithm of net + Chen & Jaggi (2000), sales Evans (2004) LMKT Firm size = natural logarithm of + Balachandran & Bliss market capitalization (2004), Chen & Jaggi (2000), Eng & Mak (2003), c. Characteristics related to market CONG Scope of business operations = + Chen & Jaggi (2000) dummy; = 1 if company is a conglomerate firm such as Bangkok Bank Group, Kasikorn Bank Group, Bank of Ayudhaya group, CP group, Central group, Saha Union group, Saha Pathanapibul group, Siam Cement group, Sri Krung Wattana group and Sun Hua Seng; = 0 if company is a non-conglomerate firm BIG4 Type of audit firm = dummy; = 1 if + Balachandran & Bliss type of audit firm is Big4 such as (2004), PriceWaterhouseCoopers, Ernst & Chen & Jaggi (2000), Young, Deloitte and Touche, and Eng & Mak (2003), KPMG; = 0 if type of audit firm is Gul & Leung (2004) non-Big4

Table 5 29

Descriptive Statistics of Measurement of the level of board of directors’ quality (N=391) Acrony Independent Variables Companies Comply Frequency Percentage m BCEO The titles and authority of the board’s chairman 218 55.75 and head of management team are clearly separated BI51 More than half of the directors on the board are 17 4.35 independent non-executive directors (INDs) BMAL All directors on board to attend every board 14 3.58 meetings BIAD Internal audit department is in company 285 72.89 ACRC AC and RC are established existence 134 34.27 ACCI The chairman of AC is an IND 353 90.28 IDAC At least three AC members are INDs 313 80.05 ACMA All AC members to attend every AC meetings 141 36.06 ACEX At least one AC member must be a financial 46 11.76 reporting expert as CPA RCCI The chairman of RC is an IND 81 20.72 RCPR More than half of the RC members are non- 104 26.60 executive directors Overall Compliance 1,706 39.67 (Sum of Frequency = 11 BOD x 391 companies = 4,301) (1,706 / 4,301)

Table 6 Descriptive statistics of dependent, independent, control, and moderator variables (N=391) Variable Acronym Mean S.D. Dependent Variable Strategic information DVIA 0.44 .14 Non-financial information DVIB 0.20 .10 Financial information DVIC 0.40 .10 30

All of voluntary information DVIT 0.33 .08 Independent Variable Board of Directors’ Quality Index BOQI 0.40 .17 Control Variable Income before extraordinary items over PPM 0.08 .23 net sales IBEX over book value of equity for the ROE 0.20 .73 beginning of the period Current assets over current liabilities CR 2.55 3.37 Long-term debt over book value of DE 1.00 12.28 common equity Natural logarithm of net sales LSAL 5.51 1.49 Natural logarithm of market LMKT 5.32 1.60 capitalization Frequency Percentage Scope of business operations CONG Company is a conglomerate firm 1 58 14.8 Company is not a conglomerate firm 0 333 85.2 Audit firm size influence BIG4 Audit firm size is Big4 1 243 62.1 Audit firm size is not Big4 0 148 37.9 Moderator Variables Frequency Percentage The largest shareholder’s ownership LCON Controlling ownership 1 306 78.3 (More than 25%) Non-Controlling ownership 0 85 21.7 (At most 25%) The largest shareholder LCNE Non-executive director 1 97 24.8 Executive director 0 294 75.2 The largest shareholder FCON Family member 1 221 56.5 Non-family member 0 170 43.5 31

Table 7 Correlation Matrix of the major variables BOQI PPM ROE CR DE LSAL LMKT CONG BIG4 LCON LCNE FCON DVIA DVIB DVIC DVIT BOQI 1.00 .10 .01 -.13** .08 .33** .41** .03 .18** -.02 .31** -.31** .28** .28** .07 .28** PPM 1.00 .20** .09 -.05 .09 .26** .07 .09 .05 -.02 -.01 .16** .09 -.02 .10 ROE 1.00 -.01 -.08 .03 .08 -.05 .04 .03 -.01 .03 .15** .07 .04 .11* CR 1.00 -.03 -.29** -.11* -.08 -.11* .04 -.01 .01 -.01 -.14** -.05 -.09 DE 1.00 .10* .09 .12* .04 .03 -.03 .05 .12* .12* .01 .11* LSAL 1.00 .77** .10 .21** .09 .22** -.24** .27** .43** .24** .43** LMKT 1.00 .13** .19** .01 .30** -.25** .36** .46** .17** .45** CONG 1.00 .04 -.06 -.02 -.13* .05 .11* -.07 .04 BIG4 1.00 -.04 .14** -.26** .11* .13* .05 .13** LCON 1.00 -.21** .06 .00 .06 .11* .08 LCNE 1.00 -.57** .16** .18** .07 .19** FCON 1.00 -.20** -.20** -.09 -.22** DVIA 1.00 .38** .20** .67** DVIB 1.00 .35** .80** DVIC 1.00 .72** DVIT 1.00

Note: Multicollinearity between independent variables becomes a problem when the correlation between the variables exceeds .80 or .90 (Field, 2000 as cited in Mangena and Pike, 2005), * p < .05, ** p < .01. 32

Table 8 Hierarchical regression results using control variables, independent variable, and moderating variables in models 2.1 – 2.3 on the relationship between board of directors’ quality index (BOQI) and a firm’s level of strategic information (DVIA) adjusted for items that are not applicable to the firm (N=391) Standardized Beta Step 1 Step 2 Step 3 (MV) Step 4 (Interaction Term) Variables CV Model 1 Model 2.1 Model 2.2 Model 2.3 Model 2.1 Model 2.2 Model 2.3 (1)-(8) IV LCON LCNE FCON LCON LCNE FCON Control Variables PPM .05 .05 .05 .05 .06 .05 .05 .06 ROE .11* .12* .12* .12* .12* .12* .12* .12* CR .03 .05 .05 .04 .04 .05 .04 .04 DE .10* .10* .10* .10* .11* .10* .10* .11* LSAL -.01 -.01 -.00 -.00 -.02 -.00 -.01 -.02 LMKT .34** .27** .27** .26** .27** .27** .25** .26** CONG -.01 .00 .00 .00 -.01 .00 .01 -.01 BIG4 .04 .02 .02 .02 .00 .02 .03 .01

Independent Variable (BOQI) .16** .16** .15** .14* .15 .12 .15* Moderating Variable (MV) -.01 .04 -.10 -.02 -.09 -.06 Interaction term (BOQI x MV) .02 .15 -.04

Statistics R Square .16 .18 .18 .18 .19 .18 .19 .19 Adjusted R Square .14 .16 .16 .16 .17 .16 .16 .17 R Square Change .16 .02 .00 .00 .01 .00 .00 .00 F Change 9.13** 9.59** .01 .62 3.81 .01 1.05 .13 Durbin-Watson 1.92 1.93 1.94 Tolerance Min / Max .10 / .96 .10 / .96 .13 / .95

* p < .05, ** p < .01

Table 9 33

Hierarchical regression results using control variables, independent variable, and moderating variables in models 2.1 – 2.3 on the relationship between board of directors’ quality index (BOQI) and a firm’s level of non-financial information (DVIB) adjusted for items that are not applicable to the firm (N=391) Standardized Beta Step 1 Step 2 Step 3 (MV) Step 4 (Interaction Term) Variables CV Model 1 Model 2.1 Model 2.2 Model 2.3 Model 2.1 Model 2.2 Model 2.3 (1)-(8) IV LCON LCNE FCON LCON LCNE FCON Control Variables PPM -.01 -.01 -.01 -.00 -.00 -.01 -.00 -.00 ROE .05 .05 .05 .05 .05 .06 .05 .05 CR -.05 -.04 -.05 -.04 -.05 -.04 -.04 -.05 DE .07 .07 .07 .07 .07 .06 .07 .07 LSAL .16* .17* .16* .17* .16* .15 .17* .16* LMKT .31** .27** .28** .26** .27** .28** .26** .26** CONG .04 .04 .04 .04 .03 .05 .04 .04 BIG4 .02 .02 .02 .01 .00 .02 .01 .00

Independent Variable (BOQI) .10* .10* .09 .08 -.08 .11 .09 Moderating Variable (MV) .04 .04 -.07 -.18 .12 -.04 Interaction term (BOQI x MV) .30* -.09 -.02

Statistics R Square .24 .24 .25 .25 .25 .25 .25 .25 Adjusted R Square .22 .23 .23 .23 .23 .23 .23 .23 R Square Change .24 .01 .00 .00 .00 .01 .00 .00 F Change 14.79** 3.86* .87 .83 1.79 4.20* .43 .04 Durbin-Watson 1.57 1.54 1.53 Tolerance Min / Max .10 / .96 .10 / .96 .13 / .95

* p < .05, ** p < .01

Table 10 34

Hierarchical regression results using control variables, independent variable, and moderating variables in models 2.1 – 2.3 on the relationship between board of directors’ quality index (BOQI) and a firm’s level of financial information (DVIC) adjusted for items that are not applicable to the firm (N=391) Standardized Beta Step 1 Step 2 Step 3 (MV) Step 4 (Interaction Term) Variables CV Model 1 Model 2.1 Model 2.2 Model 2.3 Model 2.1 Model 2.2 Model 2.3 (1)-(8) IV LCON LCNE FCON LCON LCNE FCON Control Variables PPM -.04 -.04 -.05 -.04 -.04 -.05 -.04 -.04 ROE .04 .04 .03 .04 .04 .04 .03 .04 CR .02 .02 .02 .02 .02 .02 .02 .02 DE -.00 -.00 -.01 -.00 .00 -.01 .00 .00 LSAL .26** .26** .24** .26** .25** .23** .26** .25** LMKT -.01 -.01 .01 -.01 -.01 .01 -.02 -.01 CONG -.09 -.09 -.09 -.09 -.10 -.08 -.09 -.10* BIG4 .01 .01 .01 .01 -.01 .01 .01 -.01

Independent Variable (BOQI) .00 .01 .00 -.01 -.13 -.03 -.05 Moderating Variable (MV) .09 .01 -.06 -.08 -.09 -.15 Interaction term (BOQI x MV) .23 .12 .10

Statistics R Square .07 .07 .07 .07 .07 .08 .07 .07 Adjusted R Square .05 .05 .05 .04 .05 .05 .04 .04 R Square Change .07 .00 .01 .00 .00 .01 .00 .00 F Change 3.44** .00 2.96 .05 1.09 2.05 .55 .52 Durbin-Watson 1.53 1.53 1.50 Tolerance Min / Max .10 / .96 .10 / .96 .13 / .95

* p < .05, ** p < .01

Table 11 35

Hierarchical regression results using control variables, independent variable, and moderating variables in models 2.1 – 2.3 on the relationship between board of directors’ quality index (BOQI) and a firm’s level of all of voluntary information (DVIT) adjusted for items that are not applicable to the firm (N=391) Standardized Beta Step 1 Step 2 Step 3 (MV) Step 4 (Interaction Term) Variables CV Model 1 Model 2.1 Model 2.2 Model 2.3 Model 2.1 Model 2.2 Model 2.3 (1)-(8) IV LCON LCNE FCON LCON LCNE FCON Control Variables PPM -.01 -.01 -.01 -.00 -.00 -.01 -.01 -.00 ROE .09 .09 .09 .09* .09* .09* .09 .09* CR -.00 .01 .00 .01 .00 .01 .01 .00 DE .07 .07 .07 .07 .08 .07 .07 .08 LSAL .20** .20** .19* .20** .19* .18* .20** .19* LMKT .28** .24** .25** .22** .23** .25** .22** .23** CONG -.03 -.02 -.02 -.02 -.03 -.01 -.02 -.03 BIG4 .03 .02 .02 .02 .00 .03 .02 -.00

Independent Variable (BOQI) .11* .11* .10* .09 -.05 .09 .08 Moderating Variable (MV) .06 .05 -.10* -.14 -.01 -.12 Interaction term (BOQI x MV) .27 .07 .02

Statistics R Square .23 .24 .24 .24 .25 .25 .24 .25 Adjusted R Square .22 .22 .22 .22 .23 .23 .22 .23 R Square Change .23 .01 .00 .00 .01 .01 .00 .00 F Change 14.33** 5.08* 1.72 .86 4.12* 3.15 .23 .03 Durbin-Watson 1.57 1.52 1.50 Tolerance Min / Max .10 / .96 .10 / .96 .13 / .95

* p < .05, ** p < .01 36

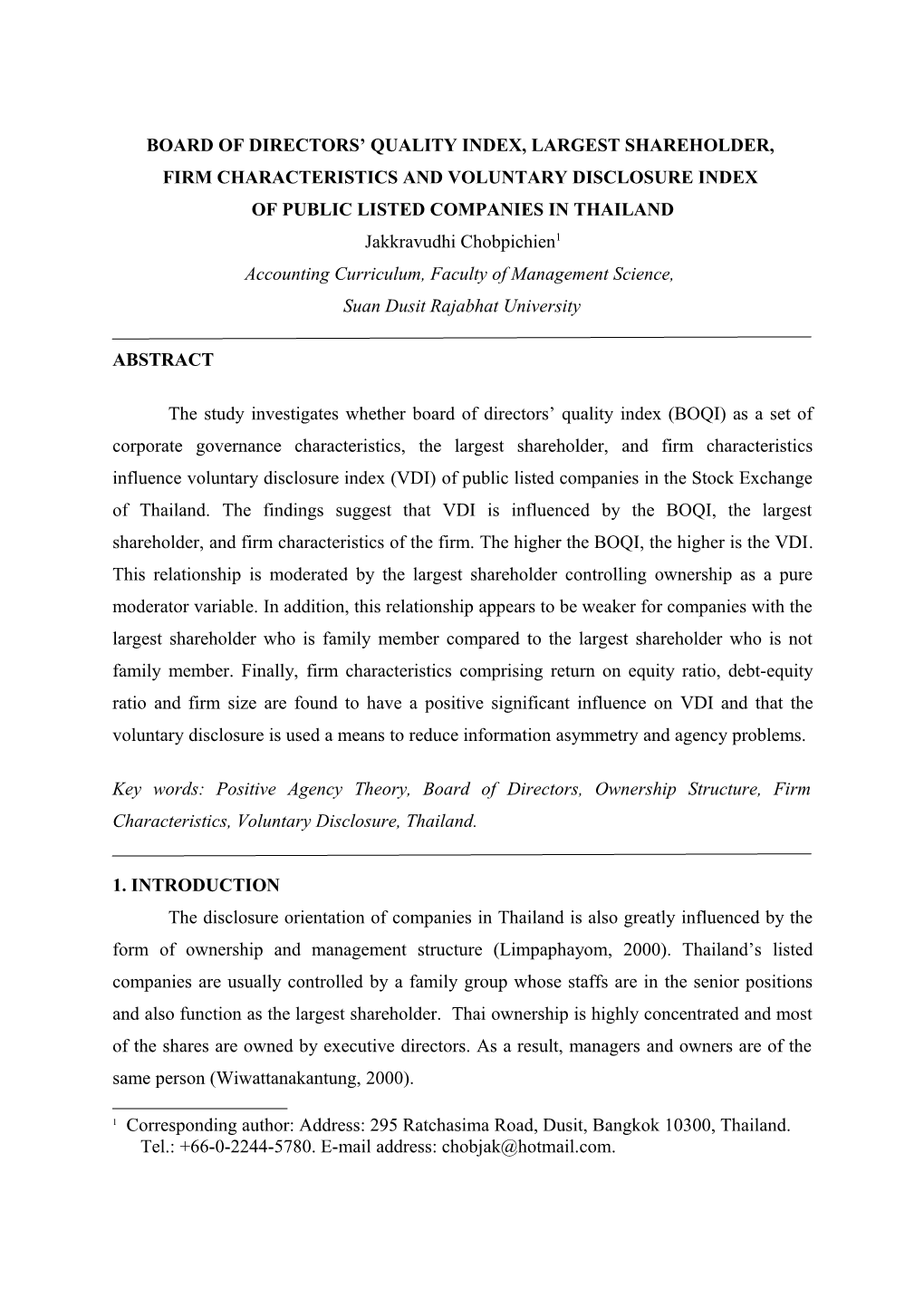

The result of the significant interaction is presented in Figure 1.

.22

.21

.20

.19

.18 LCON B

I .17 V non-controlling D

ow nership

n .16

a controlling e

M .15 ow nership .00 1.00

HLBOQI

Figure 1 Interaction between the level of board of directors’ quality (BOQI) and the largest shareholder’s ownership (LCON) for the level of non-financial information (DVIB).

APPENDIX 1 Voluntary Disclosure Checklist A. Strategic Information B. Non-financial Information (Continued) (1 General corporate information (6) Social policy and value-added ) information V1 Brief history of company V36 Safety of products V2 Organizational structure V37 Environmental protection programs – qualitative (2 Corporate strategy V38 Environmental protection ) programs – quantitative V3 Statement of strategy and V39 Community programs objectives – general V4 Statement of strategy and V40 Value-added statement objectives – financial V5 Statement of strategy and V41 Value-added data objectives – marketing V6 Statement of strategy and V42 Value-added ratios objectives – social V7 Impact of strategy on current V43 Qualitative value-added results information V8 Impact of strategy on future C. Financial Information results (3 Research and development (R&D) (7) Segmental information ) V9 Corporate policy on R&D V44 Geographical production - quantitative V10 Location of R&D activities V45 Line-of-business production – quantitative 37

V11 Number employed in R&D V46 Competitor analysis – qualitative (4 Future prospects V47 Competitor analysis – ) quantitative V12 Statement of future prospects – V48 Market share analysis – qualitative qualitative V13 Qualitative forecast of sales V49 Market share analysis – quantitative V14 Qualitative forecast of profits (8) Financial review V15 Qualitative forecast of cash V50 Profitability ratios flows V16 Order book or backlog V51 Qualitative comments on information profitability B. Non-financial Information V52 Cash flow statement – direct (5 Employee information V53 Cash flow ratios ) V17 Geographical distribution of V54 Liquidity ratios employees V18 Line-of-business distribution of V55 Gearing ratios employees V19 Categories of employees by sex V56 Disclosure of brand valuation V20 Categories of employees by V57 Financial history or summary – 6 function or more years V21 Identification of senior V58 Off balance sheet financial management and their functions information V22 Number of employees for 2 or V59 Advertising information – more years qualitative V23 Reasons for changes in employee V60 Effects of inflation on future numbers or categories over time operations – qualitative V24 Amount spent in training V61 Effects of inflation on results – qualitative V25 Nature of training V62 Effects of inflation on assets – qualitative V26 Policy on training V63 Effects of interest rates on results V27 Categories of employees trained V64 Effects of interest rates on future operations V28 Number of employees trained (9) Foreign currency information V29 Safety policy V65 Effects of foreign currency fluctuations on future operations – qualitative V30 Data on accidents V66 Effects of foreign currency fluctuations on current results – qualitative V31 Cost of safety measures V67 Foreign currency exposure management description V32 Policy on communication (10) Stock price information V33 Redundancy information V68 Share price trend V34 Equal opportunity policy V69 Market capitalization trend statement V35 Recruitment problems and V70 Foreign stock market listing related policy information 38