Chapter 6: Real Estate Market Analysis

R.E. “Market Analysis” is a collection of practical analytical tools and procedures designed to help answer decision questions, such as:

Where to locate a branch office? What size or type of building to develop on a specific site? What type of tenants to look for in marketing a particular building? What the rent and expiration term should be on a given lease? When to begin construction on a development project? How many units to build this year? Which cities and property types to invest in so as to allocate capital where rents are more likely to grow? Where to locate new retail outlets and/or which stores should be closed?

Market Anlysis usually requires quantitative or qualitative understanding (& prediction) of: Demand Side Supply Side

Of the Space Usage Market relevant to some R.E. decision. Types of Market Analysis: Specific micro-level analysis o Applies to single property, site, or user o E.g., feasibility analysis or site analysis for a development project Broader, more general characterization of a space market o Applies to an entire R.E. space market segment or submarket o E.g., forecast of supply & demand (&/or rents and vacancy rates) in Chicago office market, or Class A office Mkt in downtown Chicago

Focus on latter type (market supply & demand)…

Five major market indicators: 1. Vacancy rate 2. Market Rent 3. Quantity of new construction starts 4. Quantity of new construction completions 5. Absorption of new space Vacancy Rate: Percentage of the stock of space that is currently not occupied

Vac.Rate = (Empty SF)/(Total SF) = 1 – Occup.Rate

Watch out for sub-lease space:

o Space leased but unoccupied is vacant.

Vacancy Rate is an indicator of equilibrium (balance betw supply & demand in the space market)

Some vacancy is normal and natural in a market, due to:

o Search time & moving costs (hence LT leases): . Don’t take “first deal” . Search for “good deal” (takes time to find) o “Overbuilding”: . Impossible to perfectly predict demand growth . “Lumpy supply” The “natural vacancy rate”: o Rate around which vacancy tends to cycle o Rate that indicates supply/demand balance o Above which rents fall, below which rents rise o Tends to be higher in more volatile & faster-growth markets o Tends to be lower in more supply-restricted markets Rent: . Rent on new leases in the market . Another equilibrium variable . Most important space market variable . Tricky to accurately quantify (private info,“apples vs oranges” problems) . Watch out for “asking rent” vs “effective rent” o E.g., $10 rent but 1-yr abatement in 5-yr lease: o What would you say is the “effective rent”?

. Consider “real rent” – rent adjusted for general inflation (as better indicator of market trend)

Construction: . Supply side variable . Starts & completions o Starts “Pipeline” o Completions Additions to supply side of mkt

. Consider net addition to supply: o Constr Completions – Demolition & Conversion Out o Include re-habs & conversions in also Absorption: . Change in occupied space . Demand side variable . “Gross absorption” = Total new lease signings o Includes moves within the market . “Net absorption” = Net increase in occupied space . Net absorption more relevant for indicating market demand:

. (Vacant SF)t = (Vacant SF)t-1 + (Constr)t – (Net Absorption)t

* * *

These market indicator variables: . Vacancy, Rent, Construction, Absorption Can be used to help characterize & understand the current market, and forecast how it may change relevant to R.E. decisions. e.g., The Months Supply measure:

Vac Constr MS NetAbsorp /12

MS < Typical Construction Project Duration Tight Market Room for new development projects

MS > Typ.Constr.Duration May be some slack (but consider natural vacancy rate). Example market analysis:

Exhibit 6- : Annual construction, absorption, and vacancy in the US office market. 1994-98 are historical figures, 1999-2001 are forecasts. Source: LaSalle Advisors Investment Research, 1999 Investment Strategy Annual Report. © LaSalle Investment Management, reproduced by permission. What type of decisions would such an analysis be relevant for?… Defining the scope of the market analysis… . Geographic/Property type market segments (or sub-markets) . Time-frame of the study (historical, forecast to when?)

Example of geographic sub-markets: Atlanta office market

Exhibit 6- : Atlanta MSA Office Sub-markets, 1998. (Source: Lend Lease Real Estate Investments, Real Estate Outlook: 1999, based on data from Jamison Research and Lend Lease Investment Research. © Lend Lease, reproduced by permission. ) Market analysis methodology: . Simple trend extrapolation vs Structural analysis

Trend extrapolation: . Take advantage of inertia in space market (past partly predicts the future) . Consider trends and cycles . Potential to use statistical techniques (time-series analysis: autoregression, ARIMA, VAR, vector error- correction) . Potential to bring in capital market factors as predictors

Structural Analysis: . Model the structure of the market (underlying determinants of supply & demand, e.g. population growth and employment growth) . Forecast the underlying determinants (e.g., economic base analysis like we talked about in Ch.3), then use model to predict space market. . Formal analysis requires: o Demand model (including elasticities) o Supply model (inclu elasticities & lags) o Equilibrium model (including landlord behavior) . Useful for gaining fundamental understanding of the market, and making long-term forecasts . Used more in academic studies than business decisions More widely used in business decision-making are basic short-term (1-3 yr) structural market analyses… Exhibit 6-3: Generic framework of a basic short-term structural market analysis for real estate

SUPPLY SIDE DEMAND SIDE

Inventory existing supply Identify sources of space usage demand

Quantify relationship between demand sources and quantity of space usage

Inventory construction pipeline Forecast demand sources

Forecast of new supply Forecast of new demand

Forecast space shortfall or surplus

Decision implicatons? Major drivers of the demand side of the space market…

Exhibit 6-4: Major demand drivers by property type Property Type Demand Drivers Residential single family (Owner occupied) Population Household formation (child rearing ages) Interest rates Employment growth (business & professional occupations) Residential multifamily (Apartment renters) Population Household formation (non-child- rearing ages) Local housing affordability Employment growth (blue collar occupations) Retail Aggregate disposable income Aggregate household wealth Traffic volume (specific sites) Office Employment in office occupations: Finance, Insurance, Real Estate (FIRE) Business & professional services Legal services Industrial Manufacturing employment Transportation employment Airfreight volume Rail & truck volume Hotel & convention Air passenger volume Tourism receipts or number visitors

A simple formal structural model of a space market…

Supply side:

C(t) (R(t L) K), if R(t L) K, (1) 0, otherwise

S(t) S(t 1) C(t) (2) Demand Side:

D(t) R(t) N (t) (3)

OS(t) D(t 1) (4)

Physics: Vacancy rate: v(t) (S(t) OS(t)) / S(t) (5) Landlord behavior: R(t) R(t 1)(1 ((v(t) V ) /V )) (6)

Put these six equations together . . . Numerical example: Supply sensitivity = 0.3 Demand sensitivity = 0.3 Technology = 200 SF/employee Demand intercept = 10 million SF Rent sensitivity = 0.3 Construction lag L = 3 years

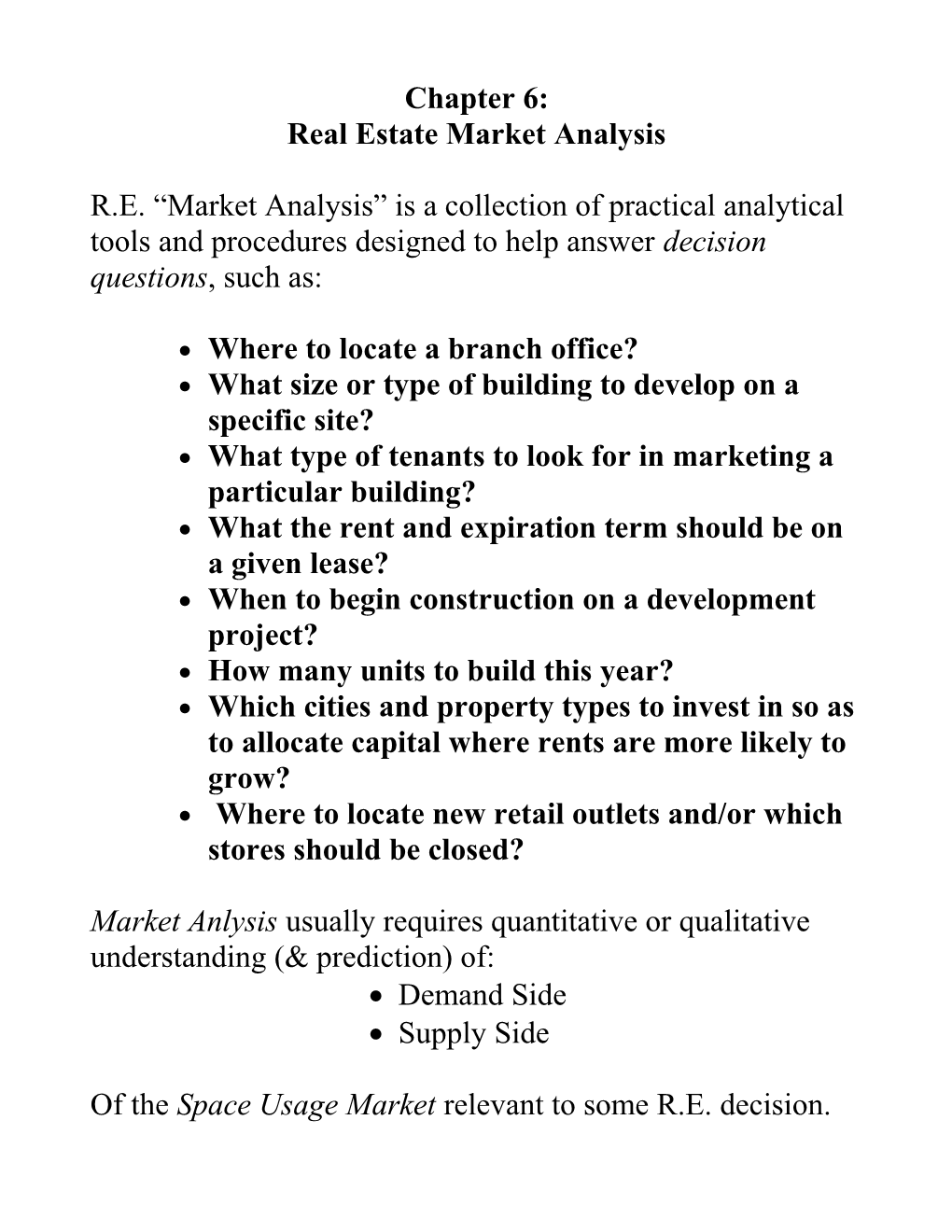

Exhibit 6-5 Simulated Space Market Dynamics

100 0.800

90 0.700 80 0.600

. 70 l p

0.500 F m

60 S E

M ,

t . r n

50 0.400 t e s R n

, 40 o c

0.300 C a V 30 0.200 20

10 0.100

0 0.000 1 3 5 7 9 1 3 5 7 9 1 3 5 7 9 1 3 5 7 9 1 3 5 7 9 1 3 5 7 9 1 1 1 1 1 2 2 2 2 2 3 3 3 3 3 4 4 4 4 4 5 5 5 5 5 Year

EMPL VAC% RENT CONST

The real estate cycle may be different from and partially independent of the underlying business cycle in the local economy.

The cycle will be much more exaggerated in the construction and development industry than in other aspects of the real estate market, such as rents and vacancy.

The vacancy cycle tends to slightly lead the rent cycle (vacancy peaks before rent bottoms).

New construction completions tend to peak when vacancy peaks. In the preceding model, were any of the market participants forward-looking?

What features of the above results do you think are due to myopia or purely adaptive behavior on the part of the market participants?

In the real world, what factors or elements in the real estate system will tend to be forward-looking?

In the real world, will it be possible to perfectly forecast the future? Will some market participants likely be somewhat myopic or adaptive in their behavior?