Additional Chapter The Eurozone and the Economic Crisis: Performance and Outlook

Learning Objectives

By the end of this chapter you should be able to understand:

The record of the eurosystem until the eurozone crisis; The main features of the international economic crisis The strains imposed on the eurozone by the economic crisis.

Introduction

The aim of this chapter is to provide a description of the historical evolution of the Eurozone to help in understanding the recent events of the euro crisis. The first years of the common currency went relatively smoothly, but from late 2009 the climate changed dramatically. Bail-outs became necessary for Greece, Ireland, Portugal, Spanish banks and Cyprus, with fear of contagion to Italy, Slovenia and other eurozone countries. The chapter attempts to show how major flaws emerged in the construction of Eurozone institutions. The first part of this chapter deals with the record of EMU in its first 10 years and the problem of ongoing divergences between euro countries. There is then a brief description of the economic crisis illustrating the strains it imposed on the euro. The approach is largely chronological to reflect the evolution of the issues and debate. At times separate paragraphs have been inserted on specific issues such as the bail-out funds, eurobonds, or the differences of opinion on the role of the European Central Bank (ECB). The final section draws conclusions and attempts to indicate possible future developments.

The first decade of the Eurosystem

The initial ten years of the euro were relatively positive, and rather surprisingly the commemorations of the first decade on the websites of the ECB and European Commission hardly make any mention of the crisis.1 The early Eurosystem was relatively successful in realizing its primary objective of price stability, partly because of the efforts of its member states to meet the Maastricht criteria. In its first decade the average inflation rate in the Eurozone was 1.98 per cent. 2 Growth was 2.1 per cent for 1999-2008, and generally slightly worse than US performance (2.6 per cent over the same period). The explanation probably lies largely in the structural weaknesses of the EU economy (see Chapter 7), and perhaps not surprisingly the ECB denied that the cause was an over-restrictive monetary policy stance. The movements of the euro against other currencies in its early years defied the predictions of many observers, with an initial fall, 3 followed by a substantial rise against the dollar after 2002

1 (when Sarkozy, among others, accused the Eurosystem of allowing overvaluation of the euro to the detriment of EU exporters). Further falls took place in 2008 and in 2010. The Eurosystem made it clear at the start that it would not take responsibility for the exchange rate, and that blind neglect was the best policy, but at times intervened (such as in 2000) to support the euro.

The underlying difficulties of the eurozone

Optimum currency area theory (see Chapter 9) suggests that to be sustainable a monetary union like the eurozone should not experience too much divergence of major economic variables. However, the eurozone countries were characterised by divergences with respect to: Public sector deficits, and thereby public debt levels (see Table 11.1 in Chapter 11); Private sector deficits (and therefore private debt levels). The private sector balance is taken to be indicated by the sum of net borrowing by households and the non-financial corporate sector; and International competitiveness, and consequently current account deficits.

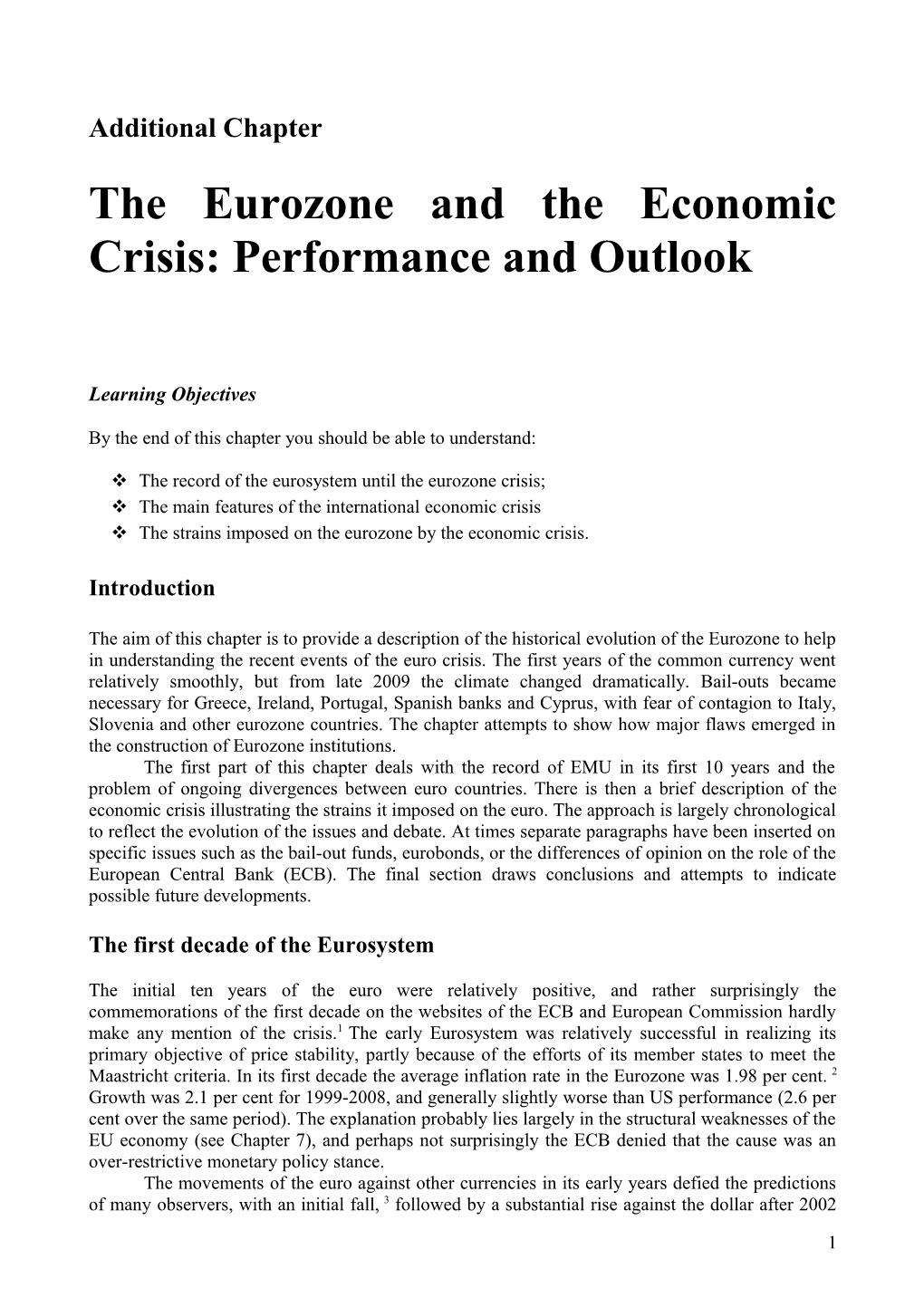

In practice when a problem initiates in one sector it is transmitted to others, and generally major difficulties end up on the books of the public sector. As will be explained below, at the beginning public debt was the main problem for Greece, though a private deficit and loss of international competitiveness added to the weakness (Nomura, 2011). Long-term loss of competitiveness and structural problems accompanied public and private deficit issues in Portugal. The level of public deficit and debt was high in Italy (see Table 11.1 in Chapter 11), but private indebtedness was relatively low (101 per cent of GDP in 2007 though rising slightly subsequently). In Ireland and Spain private sector indebtedness was 236 per cent and 211 per cent of GDP respectively in 2009, fuelled by cheap credit encouraged by the banking sector, and resulting in old- fashioned property bubbles (the one size interest rate of the eurozone did not fit all).4 As a result of intervention to resolve the situation of the banks, public indebtedness subsequently became a problem in these two countries. At the same time domestic banks held a large share of sovereign debt so there was a dangerous link between banks and the sovereign debt. As Enderlein et al (2012) argue, national fiscal problems and banking problems feed each other, and markets have recognised this source of vulnerability. Though the initial conversion rate of the D-Mark appears to have been overvalued, Germany slowly managed to regain competitiveness by keeping wage growth below consumer price inflation (see also Figure 1). During the 1990s wage inflation led to loss of competitiveness in Portugal, Ireland, Italy, Greece and Spain.5 As shown in Figure 2, countries such as Greece and Spain had large balance of payments deficits (though these fell after 2007), while others, and notably Germany, had large surpluses, reflecting diverging competitiveness. A peripheral country such as Greece has to carry out ‘internal devaluation’ to reform its labour market in order to bring about adjustments in real wages. The eurozone was characterised by asymmetry in attempts to resolve imbalances, with the internal devaluations of peripheral countries with current account deficits not being matched by expansionary policies in surplus countries such as Germany (De Grauwe 2012a). Some argued that Germany should increase its long stagnant domestic consumption (though this would require a shift in long-term patterns of behaviour).6 In March 2010 the then French Finance Minister Christine Lagarde called on ‘those with surpluses to do a little something’ to increase consumption to help weaker eurozone countries to boost exports and improve their finances, a suggestion that at least initially found little support in Germany.

2 Figure 1 Growth in nominal wages in the EU in 2000-2010 Source: Elaboration on the basis of European Commission, Statistical Annex to European Economy 2010 © European Union, 2011 National currency, annual average percentage change

Figure 2 Balance of payments end of first quarter 2012 by eurozone country (millions of euros)

Source: Elaboration on the basis of Eurostat data http://appsso.eurostat.ec.europa.eu/nui/show.do?dataset=bop_q_c&lang=en, accessed 24 August, 2012

After years of light-touch regulation and supervision of the financial sector, EU banks were highly over-leveraged when the crisis began. The ECB was not alone among central banks in focussing on price stability and failing to take adequate account of the consequences of interest rate decisions for the behaviour of banks. The introduction of EMU was not matched by parallel progress in evolving a Single Market for financial services (see Chapter 6). When a bank ran into difficulties national authorities were responsible and national taxpayers had to foot the bill. According to the European Commission,7 the volume of national support to the financial sector actually taken by banks between October 2008 and 31 December 2011 amounted to around €1616 billion (13 per cent of EU GDP).

3 The economic crisis from 2007

The economic crisis, with turmoil on international financial markets from 2007,8 and sharpest drop in economic activity since the Second World War in 2008, is frequently likened the to the Great Depression of the 1930s. Much of the literature dates the origin of the crisis to the bursting of the real estate bubble in the USA in 2007 when higher interest rates and failure of house prices to rise as expected led to a dramatic increase in default rates in the US subprime mortgage market. 9 The prices of securities linked to US real estate prices plummeted causing distress in global financial markets. What initially appeared to be primarily a US problem soon spread more widely as a result of complex linkages among international financial markets, and led in late 2008 to fears of the meltdown of the international financial system. The aim in this section is to provide a very brief outline of the main events in this crisis as it shaped many developments in the EU, including the introduction of new measures to improve financial supervision and regulation (see Chapter 6); reinforced programmes to increase growth and employment (see Chapters 7 and 17) and EMU. The literature generally indicates various factors as contributing to the rapid degeneration of the situation of the international financial system from 2007.10 A long period of low real interest rates, easy credit conditions and increases in asset prices led to a credit boom in the US and certain other developed countries, with a dramatic rise in purchases of houses and consumer durables. Protracted low returns on interest rates encouraged the financial sector to take on higher risks with the aim of increasing returns and remaining profitable. At the same time, ‘global imbalances’ contributed to overheating of the US financial system, with large end persistent current US account deficits (see Table 1.2 in Chapter 1) being accompanied by huge capital inflows from capital-poor emerging countries. At the same time China was running a huge surplus and was accused of keeping its currency low to promote exports. At a microeconomic level, factors contributing to the crisis include: the transformation of the financial sector; defects in the techniques for measuring and managing risk; flawed incentives and weaknesses in corporate governance; and failures of the regulatory system.11 The subprime mortgage crisis was preceded by the rapid growth of the weight of the financial sector in the US economy and a qualitative as well as quantitative change in the financial system (Vercelli, 2010). The increasing importance of new types of institutions belonging to a ‘shadow banking system’ (such as hedge funds) rendered it easier to move activities outside the scope of supervision and regulation by the authorities. Financial innovation, with the development of new types of instrument, many of which were linked to US mortgage payments and housing prices increased the vulnerability of the system. 12 There was little experience of assessing the risk of these instruments, or of regulating them. There was a tendency to underestimate risk, partly because before the crisis there had been a prolonged period of relative stability with low volatility of financial markets, and models often failed to take adequate account of infrequent events.13 There was also a widespread failure to realise how linkages between financial instruments could increase systemic risk. With regard to incentives, consumers and investors could not cope with the complexity and opacity of the system and were unable to safeguard their own interests. Financial institutions aimed at raising returns and this encouraged them to accumulate risk and increase leverage. Compensation of asset managers was often linked to short-term returns and the volume of affairs. Even if managers of financial institutions suspected an asset bubble, fear of sparking a chain reaction discouraged withdrawal of funds. Rating agencies often found it difficult to evaluate complex structured products, but were reluctant to pass up business, and at times had to rely on the risk management assessment of their clients. Rating agencies were also often paid by those being assessed, leading to distorted incentives and conflict of interest. A widespread belief in the efficiency of markets and in market discipline encouraged some of the authorities at the centre of

4 the global financial system to adopt an extremely light legislative touch. Box 1 sets out key dates in the evolution of the economic crisis while Box 2 deals with events from 2010 in the eurozone crisis. Widespread defaults in the US subprime market from June 2007 triggered disruption in interbank markets from August 2007 (with banks being reluctant or unable to lend to each other). Bank losses and write-downs in asset prices led to growing risks of outright bank failures. In March 2008 the investment bank, Bear Stearns ran into a severe liquidity crisis, and the US authorities stepped in to facilitate its takeover by JPMorgan Chase. After a mild recession and continuing difficulties in the interbank and US mortgage markets in the following months, the situation deteriorated rapidly after the default by the large US investment bank, Lehman Brothers, on 15 September 2008. The solvency of large parts of global financial system seemed at stake, and the US government stepped in to rescue the largest US insurance company, AIG (American Insurance Group) the following day. The crisis of confidence quickly spread across markets and countries leading to intervention on an unprecedented scale by the US and other governments. Some major financial institutions in both the EU and US were allowed to fail, but others were taken over under duress, or were nationalised (see Box 1 for specific examples). Major central banks announced co-ordinated measures to address shortages in US dollar short-term lending and the USA presented early proposals for a $700 billion programme to take on troubled assets of financial institutions.

Box 1 Key dates in the international economic crisis Date Event 2007 9 August Problems in the US mortgage market spilt over into the interbank market. 12 December Central banks in 5 main currency areas announced measures to ease problems in short-term funding markets. 2008 22 February UK bank, Northern Rock, was nationalised. 16 March JPMorgan Chase agreed to purchase Bear Stearns in a transaction facilitated by the US authorities. 4 June US government announces support measures for mortgage finance agencies Freddy Mac and Fannie Mae. 7 September US government formally took control of Freddy Mac and Fannie Mae. 15 September Default by Lehman Brothers. 16 September US government stepped in to support AIG. 18 September The UK bank HBOS was forced into a government-brokered merger with the Lloyds TSB. The UK (and subsequently US) authorities suspended short-selling (i.e. selling assets borrowed from a third party with the intention of buying identical assets to return to the lender later). Co-ordinated central bank measures to address the squeeze in US funding. late September Near simultaneous demise of the three main Icelandic commercial banks. 29 September UK mortgage lender Bradford and Bingley was nationalised. Three EU governments stepped in with a capital injection for Fortis, the insurance company. The German authorities provided a facilitated credit line for Hypo Real Estate. 30 September The Irish government introduced guarantees for six Irish banks, and other countries introduced similar measures in the following weeks. 3 October The US Congress passed a revised version of TARP (the Troubled Asset

5 Relief Program), after an earlier version was rejected on 29 September. 8 October UK announced comprehensive measures to recapitalise banks. Major central banks co-ordinated a cut in interest rates. 13 October Major central banks jointly announced that they were prepared to inject US dollars to ease tensions in money markets. European authorities pledged recapitalisation of banks system-wide. 28 October IMF package for Hungary. 15 November The G-20 countries pledged increased co-operation and efforts to encourage growth and reform the international financial system. 25 November The USA created a $200 billion facility to support consumer and small business loans, and up to $500 billion for purchases of bonds and mortgage-backed securities issued by US housing agencies. 2009 19 January As part of a more general rescue package, the UK authorities increased their stake in Royal Bank of Scotland. Other national authorities introduced similar measures in the next few days. 10 February USA presented plans for a support package including up to $1 trillion in a Public-Private Investment Program to purchase troubled assets. 5 March Bank of England introduced a programme of about $100 billion aimed at purchases of private sector assets and government bonds over a three- month period. 2 April G-20 communiqué pledged joint measures to restore confidence and growth, and to strengthen the financial system. 7 May US published results of stress tests on the largest US financial institutions, identifying 10 banks with a capital shortfall to be covered primarily by additions to equity. 2010 May Greek bailout agreed. 21 July US President Obama signed the Dodd-Frank Wall Street Reform and Consumer Protection Act (the ‘Reform Act’) relating to the regulation and supervision of the U.S. financial system. 12 September Agreement reached on Basel III setting a new capital ratio for banks of 4.5% (more than double the previous 2% level) and a new buffer of 2.5%, with phasing in of the new rules from January 2013.

Source: Elaborated on the basis of BIS (2009 and 2010) and Financial Times (various issues).

By October 2008, despite the default of the three main Icelandic banks, there were signs that the unprecedented co-ordinated intervention across countries was beginning to stem the crisis of confidence. On 8 October six central banks, including the ECB, the Federal Reserve and the Bank of England announced co-ordinated interest rate cuts. However, when official statistics in early 2009 revealed the scale of the global economic slowdown (also in emerging markets), the price of financial assets again fell. They recovered from March 2009 when major central banks (including the Bank of England, and the Federal Reserve) announced their commitment to purchases of assets and bonds. In May 2009 the ECB stated that it would start purchasing euro-denominated bonds. Despite the USA releasing the results of stress tests of banks in May 2009, the fragility of financial markets continued. Unemployment rose, in particular, in countries such as Ireland, Spain and the USA that had experienced construction booms before the crisis, The combination of financial rescue and support packages, and lower tax returns led to high levels of government budget deficits and public debt in most industrial countries. In addition to doubts about the effectiveness of support packages (which could lead to dependence of the financial

6 system on financial assistance, delays in adjustment, and possible moral hazard), there were worries about the sustainability of the high and growing level of public debt in some countries. These were exacerbated in November 2009 when Dubai World (one of the country’s three strategic investment vehicles) announced that it was seeking a moratorium on debt repayments. In September 2010 after months of discussion, international agreement was finally reached on Basel III to strengthen the international regulatory framework. This entails the gradual introduction from January 2013 of a new capital ratio for banks of 4.5 per cent (more than double the previous 2 per cent level) with a new buffer of 2.5 per cent. Though limited in scale, the aim of the agreement was to increase transparency, and constrain the build-up of excessive leverage and maturity mismatches. It was hoped this could ensure that banks maintain more liquidity to face market crises, while at the same time avoiding reduced lending which could stifle economic recovery. The ECB was one of the early and most active actors in taking measures against the crisis, injecting €95 billion into markets in August 2007, and €348.6 billion in December 2007 to address fears of insufficient short-term credit. Following the collapse of Lehman Brothers, in October 2008 the EU countries agreed a rescue plan of €1873 billion to shore up their financial sectors. The EU set out principles for bank guarantees and, as explained in Chapter 7 recommended a co-ordinated fiscal stimulus by an amount equivalent to 1.5 per cent of EU GDP (though views on fiscal stimulus varied considerably both between and within countries). In May 2009 the ECB cut its principal interest rate to a then record low of one per cent.

The beginning of eurozone crisis

Between 1999 and 2008 in what has been described as one of the ‘most extraordinary mispricings in modern financial history’ (Nomura 2011: p.38) investors had been treating all euro-denominated bonds (from German to Greek) as if they carried almost the same credit risk. From late 2008, and in particular from 2010, doubts about the ability of some of the peripheral countries to service their debt led to a rise in the yields on their sovereign bonds (see Figure 3).

Figure 3 Monthly sovereign bond yields in 2010/11 Source: Elaboration on the basis of Eurostat data, © European Union, 2011.

7 Though initially Portugal seemed the weak link in the eurozone, the crisis was eventually set off by high levels of public deficit and debt in Greece, leading to fear of default. From the early days of Greek qualification to join the euro there was a suspicion of creative accounting to meet the Maastricht criteria. In January 2010 the new Greek government stated that Greek official statistics had seriously underestimated the size of the government deficit, which was adjusted up to 13.6 per cent of GDP for the year (double what had earlier been predicted). After months of delay and debate about whether the IMF should be involved,14 on 1 May 2010 agreement was reached on a package of assistance from the ‘Troika’ of ECB, European Commission and IMF. This consisted of up to €110 billion for Greece (of which €30 billion was from the IMF), conditional on Greek implementation of a stringent austerity package. In May 2010 it was also decided to exempt the Greek government from minimum credit requirements on collateral used in its liquidity-providing operations. The following months were marked by protests, riots and strikes in Greece against the fiscal tightening. On 10 May 2010 a bail-out package for eurozone countries of up to €750 billion was agreed. This included a special-purpose European Financial Stability Facility (EFSF) of up to €440 billion (though in practice the lending capacity was limited to about €250 billion because of the need to keep large cash buffers to maintain its triple A rating). In addition there was €60 billion from the European Financial Stabilisation Mechanism,15 and up to €250 billion from the IMF. The EFSF which was set up for three years can raise funds on financial markets and make loans to eurozone countries in need.

Box 2 Key dates from 2010 onwards in the eurozone crisis Date Event January 2010 Greek sovereign debt crisis worsens: deficits are at least double those reported.

February 2010 The EU approves the Irish NAMA (National Assets Management Agency) or bad banks scheme.

March 2010 German Chancellor Merkel says that countries failing to respect budget discipline should be expelled from the eurozone. Van Rompuy task force set up to look into economic governance. May 2010 EU/IMF bail-out of up to €110 billion for Greece. Agreement on package of assistance for eurozone countries of up to €750 billion, including a special-purpose European Financial Stability Facility of up to €440 billion. The ECB decided to buy government bonds (the Securities Market Programme), and to exempt the Greek government from minimum credit requirements on collateral used in its liquidity-providing operations. The ECB reopened credit lines set up in autumn 2008 with the other major central banks, including the Federal Reserve. A fundamental debate on economic governance of the euro and EU was launched.

July 2010 Results of stress tests of EU banks released with seven out of 91 banks failing (five in Spain, two in Germany, but surprisingly none in Ireland). France and Germany announce they are in favour of ‘neutralisation of voting rights for eurozone countries with excessive deficits.

September 2010 European Commission presents economic governance proposals

October 2010 Franco-German agreement at Deauville on a permanent ‘crisis resolution mechanism’ making bondholders share in the cost of future bailouts from 2013. Van Rompuy Report on economic governance of the EU. At a European Council Germany wins agreement for a Treaty change to introduce a permanent replacement to the EFSF.

November 2010 The Troika (IMF, ECB and European Commission) agree €85 billion bail-out package

8 for Ireland. The Eurogroup decides on the permanent European Security Mechanism with bondholders paying for part of a future default.

December 2010 European Council declares that it is ‘…ready to do whatever required’ to protect the euro.

February 2011 Germany, backed by France, presents a proposal for a Competitiveness Pact.

March 2011 European Council agrees the Euro-Plus Pact.

May 2011 Portuguese bail-out.

August 2011 ECB extends its bond-buying to Italy and Spain. Jürgen Stark resigns.

November 2011 Mario Draghi becomes President of the ECB.

December 2011 Six Pack measures on economic governance adopted. David Cameron isolated at European Council that agrees Fiscal Compact Treaty. First LTRO operation with loans of up to 3 years of €489 billion from ECB to banks.

February 2012 Second LTRO operation with loans of 529.5 billion. Second bail-out for Greece.

June 2012 Bail-out of up to €100 billion agreed for Spanish banks. Report of the 4 Presidents on the architecture of EMU European Council agrees Pact for Growth and Jobs.

July 2012 Draghi announces the ECB will do ‘whatever it takes to preserve the euro’.

September 2012 Agreement on the OMT programme allowing ECB purchases of government bonds of up to three years duration.

March 2013 German Constitutional Court rules in favour of the ESM and Fiscal Compact treaty. “Two Pack” on economic governance comes into operation. Cypriot bailout Source: Elaborated on the basis of BIS (2009 and 2010), EurActiv, and Financial Times (various issues).

In a somewhat controversial move, the ECB also decided to intervene in markets to buy government bonds in a programme known as SMP (or the Securities Market Programme). Some were opposed to this measure, including Axel Weber, then President of the Bundesbank and so also member of the Governing Council of the ECB. Though considered a front- runner to replace Trichet as President of the ECB he subsequently resigned from the Bundesbank because of disagreement with the ECB policy and, in particular, insistence on tighter interpretation of the no bail-out clause. There was a delay before German approval of the Greek package since, as explained below, there was concern that the German Constitutional Court would declare rescue plans and the EFSF illegal, and against the no bail-out clause introduced by the Treaty of Maastricht (now Article 123 TFEU, see Chapter 11). At a meeting in Deauville in October 2010 Angela Merkel and Nicolas Sarkozy published a joint statement in favour of giving national politicians more authority to delay or block sanctions (the German concession to France), the possible suspension of voting rights for a country that failed to respect the SGP, and Treaty change to establish a permanent ‘crisis resolution mechanism’ to replace the EFSF when it came to an end in 2013. This would share the cost of future rescue plans between private creditors and taxpayers. The ECB President Trichet warned that talk of debt restructuring and forcing private creditors to bear part of the burden would unsettle bond markets (as in fact occurred, helping to spark the Irish crisis).

9 The Irish crisis

Following Ireland’s entry to the Eurozone in 1999, low interest rates and inflows of foreign capital allowed Irish banks to borrow heavily to finance the Irish property boom.16 Politicians who relied on developers, builders and bankers for electoral support helped to fuel the construction bubble with tax breaks and failure to tighten regulation. In September 2009 the Irish government introduced guarantees for the debts of six Irish banks, maintaining this was necessary to prevent systemic collapse.17 In March 2010 the NAMA (the National Assets Management Agency) came in to operation as a ‘bad bank’ to acquire bad property loans at a steep discount from the banks.18 The results of the stress tests published in July 2010 were positive for all the Irish banks (though Anglo- Irish Bank was excluded from the tests), but with the benefit of hindsight, were based on excessively optimistic forecasts, in particular relating to the property market. Bond yields for Ireland remained relatively stable during 2009 and early 2010, probably as a reaction to the severe austerity measures introduced in successive budgets by the Irish Government from March 2009 on. Irish sovereign bond yields began to rise rapidly from mid-2010 (see Figure 3) as awareness grew of the huge scale of financing necessary for the government to honour its guarantees to Irish banks. If the bank bail-out costs are also included, the Irish budget deficit grew from 11.9 to about 32 per cent of GDP in 2010, with public debt of 98.6 per cent.19 The financial turmoil precipitated a fall of government in Ireland, and the question of loss of national sovereignty was hotly debated in the Irish press. One of the most contested issues was the request by other EU partners for Ireland to raise its level of corporation tax from 12.5 per cent (a request refused on various occasions, see also Chapter 6). Ireland had long been accused of unfair tax competition, but maintained that the issue was not directly related to the banking crisis, and that low corporation tax was central to economic recovery and the ability to attract FDI.20 In November 2010 the Irish government announced a four-year austerity plan and a decrease of 12 per cent in the minimum wage. A few days later agreement was reached on a €85 billion bail-out package for Ireland.21

The bail-out funds

At the time of the Irish crisis it was agreed to set up a permanent European Security Mechanism (ESM) for dealing with debt crises in the Eurozone with an effective lending capacity of €500 billion.22 Collective action clauses that would involve bondholders in any eventual debt restructuring are envisaged for the ESM. In April 2012 it was agreed to increase IMF resources by $430 billion so the total sum available for rescues came to some $1500bn. 23 In 2012 the rating of the EFSF was downgraded following the downgrading by Standard and Poor’s of various EU countries.24 In November 2011 the Commissioner for the Internal Market Barnier had tried unsuccessfully to suspend sovereign ratings in ‘exceptional circumstances’. Rating agencies were accused of poor timing and conflicts of interest, and blamed for not spotting the US subprime mortgage crisis (see above) and many of the difficulties of the banking sector. The role of the eurozone rescue funds has been the subject of much debate, and various proposals have been advanced. In his writings on the economic crisis, Krugman (2012) stressed the dangers of speculators betting safely against a fund known to be too small to stabilise a market. To meet this difficulty, one suggestion was to grant the ESM a banking license so it could benefit from the lending operations of the ECB to banks (see below). In this way it would be possible to leverage ESM measures well beyond its lending ceiling of €500bn. However, Mario Draghi maintained that this was not permitted by the present design of the ESM, and was a matter for governments to decide.25

10 The debate about Eurobonds

Parallel to the debate about the size and nature of eurozone bail-out funds was an ongoing discussion about whether there should be mutualisation of eurozone debt, and in particular, whether a eurobond should be issued.26 This would entail euro area sovereign debts being jointly guaranteed by member states of the eurozone, and would have the expected advantage of lowering borrowing costs for peripheral countries. Various authors have pointed to the US experience under Alexander Hamilton, the first US Treasury secretary, as a model for the eurozone.27 Hamilton also faced a seemingly overwhelming debt problem as a result of borrowing by states to finance the American war of independence. His solution was to assume the debts of states (with no haircuts for investors), and issue a new federal debt instead. A market for US Treasury bonds was created. In the long run, this enabled the US federal system to emerge, with limits on state borrowing, a central bank, and a federal budget capable of stabilizing the economy. However, eurobonds are opposed in many circles, and notably in Germany.28 Various attempts have made to render the eurobond proposal more acceptable. Delpa and von Weizsäker (2010) wrote a policy brief for the Brueghel institute proposing that national debt below the Maastricht limit of 60 per cent could be transformed into ‘blue’ Eurobonds, while ‘red’ debt over 60 per cent would remain the responsibility of member states. The cost of the scheme was estimated as about €5.5 billion and would be permanent. However, the cost of borrowing on the higher risk red tranche of borrowing could increase, undermining the effectiveness of the scheme. A proposal by the German Council of Economic Experts (2011) effectively reverses these colours. Their suggestion was to pool government debt of the member states above 60 per cent in a debt redemption fund with joint liability. The cost was estimated at about €2.3 billion and the proposed scheme would last for about 25 years with Italy and Spain as the main beneficiaries.

The summer of 2011: The Portuguese bail-out and fears of contagion

In March 2011 the Portuguese Prime Minister Socrates resigned when the Parliament rejected the fourth set of austerity measures in a year, and in May 2011 also Portugal was granted a €78 billion bail-out from the EU and IMF. There were worries of contagion to larger eurozone countries in particular in August 2011.29 In the face of widening spreads on long-term bonds for Spain and Italy, the ECB extended its purchases of bonds on secondary markets to these two countries. Jürgen Stark, a German member of the Executive Board of the ECB, resigned, subsequently saying his motive was opposition to this policy. Austerity packages introduced by the Berlusconi government were considered inadequate and failed to assuage markets and in November 2011 a government of technocrats under Mario Monti was formed. In December measures involving fiscal and pension reform were passed, paving the way for a further package in 2012 aiming to tackle liberalisation of closed professions and labour market reform, though in practice the proposals were substantially watered down in the face of vested interests.

Towards the Fiscal Compact treaty

Countries such as Germany, Finland and the Netherlands feared that Eurozone bail-out funds or the introduction of eurobonds would give rise to moral hazard. They therefore called for tighter conditionality, and an increased role for the EU in controlling national budgets and ensuring that member states introduce adequate structural measures to raise competitiveness. The terms vary

11 according to interlocutor, and while many refer to steps towards fiscal union, Angela Merkel often used the term ‘political union’. Not one to hold back on giving advice to the Eurozone, in May 2012 David Cameron warned of the risks to everyone of a Eurozone break-up if there were not moves towards an effective firewall (earlier he had referred to a ‘big bazooka’), and political and fiscal union. In his ‘State of the Union’ address of September 2012, Barroso called for a ‘federation’ of nation states, a term echoed by French finance minister Moscovici, who also called for a common unemployment insurance fund. Again there was a stop-go process of proposals, agreements, and measures to reform economic governance. Some of these initiatives entailed working through the EU institutions using the time-honoured ‘Community’ method (see Chapter 3), while others were based upon intergovernmental co-operation between EU member states. The ‘Six-Pack’ and ‘Two-Pack’ legislative reforms described in Chapter 11 relied on the ‘Community’ method, but were paralleled by various intergovernmental initiatives during 2011. At a European Council meeting of February 2011 Germany, with the backing of France, tabled a ‘Competitiveness Pact’.30 This entailed indicators and monitoring of price competitiveness, stability of public finance, and minimum rates for investment in research and development. In return Germany was expected to agree increased financing for the EFSF. Regular review of the application of the Competitiveness Pact by the European Council was also advocated. In the event agreement was not reached on the Competitiveness Pact, but an alternative, the Euro-Plus Pact (see also Chapter 11), was agreed in March 2011. Though watered down with respect to the initial Franco-German proposal, the essence of the Euro-Plus Pact was again to accept tighter economic co-ordination as a quid pro quo for German agreement to boost the eurozone bail- out funds. Four non-eurozone member states (Britain, the Czech Republic, Hungary and Sweden) remained out of the Pact and the European Stability Mechanism, but the other non-eurozone countries decided to participate. The proposal for a Fiscal Compact treaty or ‘Treaty on Stability, Co-ordination and Governance in the Economic and Monetary Union’ (see Chapter 11) was presented at a European Council of December 2011 when British Premier David Cameron remained isolated vis- à-vis all the other member states. Cameron probably mistakenly assumed that Germany wanted a treaty backed by all 27 member states at all costs. To the surprise of the other participants, after 5 hours of negotiations and late at night he unsuccessfully requested what he termed ‘reasonable concessions’ as a condition for support. These related, in particular, guarantees for financial services and the single market. 31 At the European Council of January 2012 agreement was reached by 25 countries on the Fiscal Compact. The UK announced that it was not planning to stop member states involved in the initiative from using EU institutions. The Czech Republic also decided that it would not participate because of ratification difficulties.32

The Longer-Term Refinancing Operations (LTRO): The ECB decision to grant cheap credit to the banks

Though the new Monti government and its economic package of December 2011 reduced spreads, fears about the survival of the Eurozone remained and there was continuing evidence on financial markets of the ‘animal spirits’ described by Keynes. When Mario Draghi took over from Trichet as President of the ECB in November 2011, he announced that the sovereign bond-buying programme would be strictly limited, also with a view to assuaging the fears in some German circles that their Constitutional Court would judge such measures illegal (see below). Critics maintained that the benefits of extending the bond-buying programme to countries such as Italy and Spain in 2011 had proved relatively short-lived. In December 2011 the Governing Council of the ECB agreed an unprecedented measure to allow unlimited quantities of cheap 3-year loans to the banks.33 Under the scheme known as LTRO 12 (longer-term refinancing operations) in December 2011 523 banks borrowed €489 billion roughly equivalent to 5 per cent of the GDP of the Eurozone. In a second stage of the LTRO scheme the ECB lent a further €529.5 billion to some 800 banks in February 2012.34 On both occasions LTRO led to a fall in the borrowing costs of some of the periphery countries at least for a time. At the World Economic Forum in Davos in January 2012 Draghi maintained that LTRO had prevented ‘a major, major credit crunch’. However, many banks were under pressure as the European Banking Association had set a 9 per cent threshold for banks’ core tier one capital ratios. It was feared that they might prove unwilling to provide credit to the real economy, or to buy sovereign debt unless required to by national authorities.35 In addition concern was expressed about the exposure of the ECB balance sheet, which was estimated to have grown from €1,458bn in 2008 to €2,967bn in 2012.36 In order to receive the unlimited three-year loans the banks had to provide collateral, and this created difficulties for some of the banks most in need of liquidity. To meet this situation the ECB also made adjustments to what could be considered as collateral.37 The possibility of different standards being applied in different countries led to accusations of ‘Balkanisation’ of eurozone monetary policy, though Draghi maintained that national central banks were better placed to assess the situation in their country. The President of the Bundesbank, Jens Weidmann expressed concern about lowering of credit standards. 38

The ongoing Greek crisis and the possibility of exit by a member state from the euro

The EU and IMF had long been pointing to the persistent failure of Greece to complete the fiscal and structural reforms requested in return for the €110 billion bail-out of May 2010. The weakness of the political class, bureaucratic obstruction and social resistance were all accused of hindering implementation of the measures. However, Greece had suffered five years of recession, and pro- cyclical austerity measures worsened the situation. The tax base had been eroded so restrictive measures entailed cuts in wages, pensions and services adding to poverty and homelessness, and encouraging social disorder. It was largely the high interest rates on refinancing debt that pushed Greek debt from 130 per cent in 2009 to 170 per cent of GDP in 2011. In November 2011 Sarkozy and Merkel raised the possibility of Greece leaving the euro (sometimes referred to as ‘Grexit’). In February 2012 Commission Vice President Neelie Kroes stated that it was simply not true that allowing one country to exit would cause the whole structure to collapse. However, exit would inevitably be messy (see Eichengreen, 2007). 39 It would probably breach the EU Treaty, which does not foresee member states leaving the euro, though Article 50 of the Lisbon Treaty allows for exit from the EU.40 Exit is likely to involve a plethora of legal cases over redenominated contracts, a run on banks, bank failures, and massive capital exodus in the expectation of substantial devaluation. Capital controls would probably be necessary to prevent currency leaving the country. Article 65 TFEU allows for controls to be imposed for the purposes of ‘taxation, prudential supervision of financial institutions’, as well as for ‘public policy and public security’.41 However, it is difficult to see how capital controls could be applied on a long term basis in a single market, so exit from the EU could not be excluded. This would mean that the exiting country could lose transfers from the EU budget for economic, social and territorial cohesion, and for agriculture. There would be inflationary pressures resulting from higher prices of imports after devaluation. Printing and distributing a new currency would also involve technical costs and would take time (see also the long process of preparing euro introduction described in Chapter 10), ruling out the possibility of secrecy or surprise. Debt default, increased poverty and widening income disparities would be difficult to avoid. Eichengreen, Rose and Wyplosz (1996) have shown that a crisis in one country generally involves contagion to others.42 The Vice President of the ECB, Constâncio (2012), describes how 13 contagion may cause financial instability to reach systemic dimensions. He argues that contagion plays a crucial role in exacerbating the sovereign debt problems in the euro area so that the authorities should concentrate their crisis measures on mitigating this phenomenon. With Greek exit it would be difficult to avoid bank runs in other peripheral countries, and possibly also elsewhere due to the still wide, though reduced exposure of banks. Banks had been cutting cross-border lending since mid-2010, but this process accelerated in the first half of 2012, reflecting worries that euro break-up would lead to capital controls and tighter regulation.43

The second Greek bail-out

In late 2011 agreement in principle appeared to be reached on a second bail-out for Greece and further austerity measures, though the details remained to be worked out. The Greek Prime Minister Papandreu announced that he would hold a referendum on the package, but he was forced to backtrack and step down in favour of a crisis coalition under the former Vice President of the ECB, Papedemos. Eurozone partners, in particular creditor countries such as Germany, the Netherlands and Finland, had lost trust in the Greek ability to implement the necessary fiscal and structural reforms. In January 2012 the Greek finance minister angrily rejected German calls for Greece to cede sovereignty over tax and spending decisions to the budget Commissioner. In February 2012 German finance minister Wolfgang Schäuble called for Greek elections due in 2012 to be postponed, hinting that Greek should follow the Italian example with a purely technocratic government. There was outcry in Greece against what was considered undue interference in the democratic process. In February 2012 a second bailout of €130 billion with lower interest rates on bail-out loans for Greece was agreed conditional on further austerity measures.44 At the same time agreement was reached on the conditions for private sector involvement (PSI) or a ‘voluntary’ restructuring or ‘haircut’ of 53.5 per cent on €206 billion of Greek sovereign debt.45 It was hoped that this would reduce Greek debt from 170 per cent of GDP in 2011 to 120.5 per cent by 2020. Despite a strong showing of Syriza, a radical left coalition under Alexis Tsipras, in the first round of Greek elections in May 2012, a broad coalition government under the centre-right party New Democracy was sworn in in June 2012 so the political outlook seemed more stable. However, many observers felt that the second Greek deal would offer only temporary respite and that the Greek ‘issue’ would return.46 A debt of 120.5 per cent of GDP at the end of the decade is still substantial. Many forecasts, including those of the EU and IMF, suggested that even if the package could be successfully implemented the debt-to-GDP ratio would be higher. Up to €30 billion of the bail-out fund is earmarked to recapitalise Greek banks, but these have been suffering withdrawal of deposits and are likely to suffer additional losses as a result of the government bond swap.

Towards a bail-out for Spanish banks

In March 2012 the new Spanish Prime Minister Rajoy obtained EU assent to a raise in the government deficit to 5.8 per cent of GDP for 2012 because the country was in recession and the 2011 deficit had been higher than forecast. Additional problems also arose from fiscal laxity and mismanagement at the level of some autonomous regional and municipal governments. The Spanish government tightened austerity, introduced labour market reforms and required banks to set aside an extra €54 billion as bad loan provisions and capital buffers in 2012. However from March 2012 the Spanish spread again began to rise. There were worries about Spanish banks and their failure to recognise the full extent of their loan losses as a result of property investments in the decade to 2007. On several occasions the Spanish government revised its estimate of how much recapitalisation of the Spanish banks would cost. In particular, extra capital was needed for the nationalised Bankia, which had been formed out of seven former savings banks. As in Greece, bank

14 deposits were shrinking as clients moved their capital abroad in a slow-motion bank run.47 There was discussion about segregating difficult property loans into a ‘bad bank’ or asset management agency similar to the Irish NAMA. In June 2012 up to €100 billion in assistance from eurozone funds was agreed for Spanish banks. The deal again revealed the flaw in the system that had already become evident in the cases of Ireland and Greece. Under then-existing rules eurozone assistance had to be channelled by the Spanish government to the banks, a step that would add to sovereign debt.

Towards the Pact for Growth and Jobs

Though restrictive fiscal measures were necessary to calm bond markets, many felt that member states such as Germany had pushed too far for austerity measures at a time of recession. Simultaneous attempts to cut deficits may spill over into other countries and aggravate the economic slowdown. During 2012 there were growing calls for measures to foster growth and employment at the national and EU levels by, for instance, French President Hollande, the Commissioner for Economic and Monetary Affairs, Ohli Rehn, Mario Draghi and Mario Monti. Gradually opinions also in Germany began to shift in favour of more growth orientation. In May 2012 the finance minister Wölfgang Schäuble suggested that German prices could be allowed to rise faster than those of other eurozone countries (within a corridor of 2 to 3 per cent) to address imbalances, though without prejudicing the overall commitment to price stability and low inflationary expectations. Two theoretical developments added intensity to the debate about the effectiveness of austerity measures. In its October 2012 World Economic Outlook the IMF published results from a study showing that the impact of fiscal policy on growth was higher than previously estimated (IMF, 2012). The standard fiscal multipliers used in forecasting models, including those of the IMF were 0.5.48 The research suggested that the fiscal multiplier was in the range of 0.9 to 1.7. If this is the case fiscal tightening will cause a greater contraction of GDP than previously estimated.49 In a bestselling book This Time it is Different: Eight Centuries of Financial Folly, of 2011 and other research papers Professors Reinhart and Rogoff of Harvard University provided data that they believed indicated a 90 per cent threshold of public debt to GDP, beyond which economic growth declines rapidly. The authors presented several calculations covering different time periods including the post-War period and two centuries from 1790 to 2009. Many policy makers in the EU and USA (including Olli Rehn in the European Commission) were influenced by what became known as the ’90 per cent rule’, though the original academic research was rather more ambivalent. In 2013 a paper by Thomas Herdon, Michael Ash and Robert Pollin attempted to replicate the results, but found that Reinhart and Rogoff had made mistakes in the analysis causing growth at high debt levels to be underestimated. An error in the Excel spreadsheet meant that several critical years for New Zealand had been left out. The way of calculating average growth was also said to give too much weight to unrepresentative data points. The authors of the later paper (Herdon, Ash and Pollin 2013) thought that growth after the 90 threshold should have been 2.2 per cent rather than the -0.1 per cent of Reinhart and Rogoff (2011). From the heated debate that ensued it appeared that convincing evidence for a threshold was more elusive than had first appeared. Moreover slower GDP growth could be a cause of higher debt rather than a consequence, or causation could run in both directions (or neither). More caution was needed in interpreting data, and advocates of economic austerity could no longer rely on the 90 per cent rule as a central part of their toolkit.

The Report of the Four Presidents

15 Just before the European Council of June 2012, a report presented by European Council president Herman Van Rompuy in collaboration with the presidents of the Commission, Barroso, the Eurogroup, Junker, and the ECB, Draghi set out a blueprint for reform of the architecture to create a ‘genuine’ EMU (President of the European Council, 2012). This was important in providing an overall structure for the subsequent debate and initiatives presented, so it is useful to indicate the financial, fiscal, economic and political steps considered necessary: 1) An integrated financial framework (or move towards a banking union, see Chapter 11) with common measures for recapitalising or closing banks, and a European scheme to guarantee customer deposits, provided a single supervisor for EU financial institutions was in place. 2) A qualitative move towards a fiscal union, which would probably require treaty change. This would involve an integrated budgetary framework with coordination, joint decision-making, tighter enforcement and ‘commensurate steps towards common debt issuance’. The mutualizing of sovereign debts was seen as a medium-term objective and its details were not spelt out. Upper limits on deficits and debts would be agreed in common, and the EU role would be reinforced, possibly by introducing a eurozone fiscal body, such as a treasury office. The role and functions of the EU budget would also be redefined. 3) An integrated economic policy framework with adequate mechanisms to ensure growth, employment, competitiveness and social cohesion, and to address imbalances. This would take into account policies regarding labour markets and tax coordination to ensure the smooth running of EMU. 4) Measures to ensure democratic legitimacy and accountability, also through close involvement of the European and national parliaments.

The proposals regarding the financial framework mask differences, and not surprisingly sparked a lively debate. In July 2012 160 German economists, including the president of the IFO Institute, Hans-Werner Sinn, published a manifesto against a banking union. Another letter was signed by 200 German economists claiming that a banking union was necessary to save the eurozone. Rather confusingly, some economists signed both.

The June 2012 European Council

The European Council of June 2012 followed the (by then) well-established pattern of interventions to resolve the euro crisis. After an initial positive reaction by the markets and media, doubts set in and differences in interpretations as to what had been (or should be) decided arose, causing the initial euphoria to evaporate very quickly.50 None the less, some progress was made in addressing certain aspects of the flawed institutional structure of the eurozone. A ‘Pact for Growth and Jobs’ was agreed, taking up the proposals of additional capital for the EIB, €5 billion in EU project bonds, and more targeted use of EU Funds to promote economic, social and territorial cohesion. Country-specific recommendations to guide the policies and budgets of member states were also endorsed. Recognising the need to move towards a banking union and taking into account the report of the four presidents, Eurozone countries also agreed to be draw up a plan for common supervision of their banks involving the ECB (see Chapter 11). There was no agreement at the European Council to introduce Eurobonds or to increase the size of the EFSF or ESM as such measures were opposed by Germany. It was agreed that the ESM could directly help refinance troubled banks without having to pass through national governments once the supervision of the ECB is in place. As declared in the conclusions of the European Council, the aim was to ‘break the vicious circle between banks and sovereigns’. It was feared that if EU interventions were treated as senior, this could deter private investors. Seniority entails being put at the back of the queue to absorb losses (as happened for the 16 ECB in the second Greek bail-out of March 2012). It was therefore agreed to drop seniority status for eurozone loans to recapitalize Spanish banks, and subsequently (in September 2012) for other loans or bond purchases. At the Summit Spain and Italy sought measures to reduce borrowing costs on their sovereign debt, but they were concerned to avoid the stigma of a full bail-out. The European Council agreed ESM intervention on secondary bond markets. Monti believed that the terms for intervention had been rendered lighter,51 but Germany, Finland and the Netherlands subsequently maintained that no changes in conditionality had been introduced. Italy and Spain stated that for the time being they had no plans to activate the mechanism.

Changes in the Role of the ECB

In July 2012 the President of the ECB Mario Draghi made his famous statement that the ECB would ‘whatever it takes to preserve the euro’, adding ‘and believe me that will be enough’. He considered it ‘squarely’ within the mandate of the ECB to prevent ‘convertibility risk’ arising from doubts that the euro would survive, and maintained that it was ‘pointless to bet against the euro’. The justification for unconventional measures by the ECB was (as Draghi had stated in the past) that the transmission mechanism of monetary policy was no longer working. Draghi warned of ‘financial fragmentation’ with far higher interest rates being paid by firms and households in peripheral countries such as Greece, Spain, Portugal and Italy than in core countries such as Germany. The ‘singleness’ of monetary policy, long seen as a cornerstone of financial integration, was being undermined, and the collapse in cross-border lending by banks exacerbated this problem. If the interdependence between banks and sovereign debt could be reduced by the ECB buying government bonds, the price paid by banks to access funding could be cut, and banks might be prepared to pass these lower costs on to firms and households. In September 2012 the agreement was reached on the programme to allow the ECB to intervene to purchase short-term bonds of up to three years duration, which was named outright monetary transactions (OMT). The ECB also agreed to renounce seniority. In contrast with the previous bond-buying programme, which was limited, potentially unlimited purchases could be endorsed with no prior quantitative limits. Interventions would require beneficiary countries to ask for support from eurozone bail-out programmes, and to accept ‘strict and effective’ conditionality. The bail-out funds would intervene in the primary market to buy long-term bonds. However, the bottom line of the ECB was that the crisis was ultimately for politicians to resolve by means of fiscal consolidation and appropriate structural reforms. The ECB hoped to avoid the shortcomings of its previous SMP programme, which had involved purchases of €212 billion, 52 but failed to stop the crisis escalating. One member of the ECB’s governing Council, Bundesbank president Jens Weidmann, withheld his vote on the programme, though the other German representative, Jorg Asmussen voted in favour. The Bundesbank commented publically on Weidmann’s decision, stating that he considered bond-buying tantamount to financing governments by printing banknotes, which is said to blur the distinction between fiscal and monetary policy. It was also stated that the interventions could also redistribute risks between the taxpayers of different countries.53 In its first year the mere presence of OMT seemed to guarantee its effectiveness and it was not actually used. However, various observers expressed doubts about how effective conditionality would prove in practice if the ECB is prepared to do what it takes to save the euro anyway. If a country fails to implement adequate reform would the ECB stop buying its bonds and run the risk of spooking markets? Though the likelihood of short-term inflation was low, it was feared that ECB credit extension without effective policy conditionality could give rise to moral hazard and ultimately lead to a loss of ECB credibility. 54

17 The role of the German Constitutional Court

In 2010 the German Constitutional Court was called upon to rule on whether the EFSF and the disbursement of bail-out funds to Greece were compatible with the no bail-out clauses of the treaties (see Chapter 11). The Court rejected appeals for injunctions in both these cases on the grounds that delays would cause greater damage to Germany than an eventual temporary constitutional infringement. The complaint against the ESM was that it was not compatible with the German Constitution (or Grundgesetz) because undermined the budget sovereignty of the Bundestag or German Parliament, and lacked democratic control.55 In September 2012 the Court in Karlsruhe ruled that any increase in the German financial liability to the ESM above €190 billion would have to be sanctioned by the Bundestag, and comprehensive information on the operations of the ESM would have to be provided to the parliamentarians. The Court also ruled in favour the legality of the Fiscal Compact treaty (see Chapter 11), which, together with the ESM, had been approved by a two-thirds majority in the Bundestag in July 2012. A final judgement by the Court on both issues was postponed until later.

The Cyprus Bailout

From the 1980s low corporate tax, dual tax agreements, and light-touch regulation enabled Cyprus to develop a ‘business model’ based on providing financial services abroad. As a result the Cypriot banking sector was estimated to have assets over 8 times Cypriot GDP including large Russian deposits. Bank transfers between Russia and Cyprus were estimated at €250 billion in 2012.56 Cypriot banks were heavily exposed to the Greek crisis and presented an example of contagion. The situation was exacerbated by substantial falls in Cypriot property prices. Public debt amounted to 87 per cent of GDP in 2012. In early 2012 the Communist government under President Demetris Cristofias obtained a €2.5 billion loan from Russia. In June 2012 days before a deadline to recapitalise one the main Greek Cypriot banks, Cyprus again asked for a €5 billion loan from Russia, but in the event had to seek an EU bailout. Without imposing losses on those holding bank deposits, in March 2013 it was stated that €17.2 billion was needed for a rescue package (though later it was suggested that €23 billion was required). The Cypriot government first announced that there would be a ‘tax’ of 6.75 per cent on bank deposits of under €100,000 and of 9.9 per cent on deposits of over €100,000. The aim seemed to be to avoid antagonising Russians with large bank deposits and placing the Cypriot ‘business model’ at risk. Not surprisingly there were angry protests in the streets of Cyprus, and the Cypriot Parliament rejected the proposal. A revised bail-out package was presented on March 25 2013 with safeguards on deposits less than €100,000 (in line with EU principles). The package entailed winding up the second largest Cypriot bank, Laiki, and splitting it into a ‘good bank’ of deposits less than €100,000 to be merged with the number one lender, the Bank of Cyprus, and a ‘bad’ bank with larger deposits subject to haircuts.57 Months later in August 2013 the size of the haircuts on deposits over €100, 000 was set at 47.5 per cent.58 The Dutch Finance Minister Dijsselbloem made the controversial statement that Cyprus marks a new commitment by the eurozone to make investors rather than taxpayers bear the burden of bank failures, though he later backtracked stating that Cyprus was a special case.

Slovenia

In July 2012 Slovenia denied rumours that it was about to ask for a bail-out, but a month later the

18 rating agency Moody’s downgraded the sovereign bond rating of Slovenia. The government deficit rose to 6.7 per cent in 2012 and losses of the mainly state-owned banks continued after a combined loss of €200 million in 2011,59 mainly due to bad loans after the bursting of a credit-fuelled bubble similar to that of Spain and Ireland.

Conclusions

The first 10 years of the Eurozone were relatively tranquil and low spreads suggested that markets did not even conceive the possibility of its breakup. It was only with the crisis the consequences of certain unresolved questions began to emerge. The initial selection of countries to join the euro was clearly too generous (the Eurozone was not an optimal currency area); one size did not fit all; and there was an asymmetry between the monetary and economic aspects of EMU. From late 2009 the Eurozone lurched from crisis to crisis. There were risks of bank runs, defaults and exit from the euro of one or more countries, and most member states entered recession. Repeatedly, the announcement of austerity packages by national governments, agreement by the European Council or intervention by the ECB caused markets to rally briefly, only to be followed after a short time by renewed widening of spreads. That disaster has so far been avoided in such turbulent times is thanks to some timely interventions. The bond-buying programme of the ECB with its relaxing of collateral under Trichet managed temporarily to reduce spreads. The unlimited three-year loans from the ECB to banks through LTRO provided liquidity for the financial system and lowered borrowing costs for governments, even if the benefits passed on to firms or households were limited. Austerity measures were agreed in peripheral countries such as Greece, Portugal, Italy, Ireland, Spain, and Cyprus, but they have encountered popular backlash. Fiscal laxity has been exposed in some cases, but recession has knocked austerity packages off target and rendered structural reforms difficult. Ireland seemed the first of the bail-out countries on the road to recovery, but the scale of the mortgage burden still hangs over the economic prospects. Gradually more consensus is emerging on the need also for measures to promote growth, employment and competitiveness, but so far little has been accomplished and differences between eurozone countries persist. Weaknesses remain in the banking system and additional credit is needed for the real economy. Banks backed by weak sovereigns have to pay more to raise funds, and the debt burden of peripheral sovereigns increases if they have to bail out banks. It still remains to be seen whether this vicious circle can be broken. Discussion has begun on a banking union (see Chapter 11), but huge differences in positions remain. The EFSF and ESM bail-out funds were gradually put in place and as a quid pro quo more co-ordination of economic policies was painstakingly agreed. However, the opposition of creditor countries to a ‘transfer union’ has meant that the two rescue funds are not the ‘big bazooka’ called for by David Cameron. Agreement to introduce eurobonds has not been reached. The role of the EU in monitoring, and supervision of economic policies has increased, in particular through the Six- Pack and Two-Pack, and this trend seems likely to continue, in parallel with the Fiscal Compact treaty and other intergovernmental initiatives. However it is necessary to ensure the legitimacy of these steps towards a ‘fiscal union’. The application of economic conditionality by the EU raises issues about respect for democratic principles and national sovereignty. The real game-changers in halting the euro crisis (at least for now) seem to have been Draghi’s promise to do ‘anything it takes to save the euro’ and the mere existence of OMT (or the possibility of unlimited purchase of short-run government bonds). However, doubts remain about the effectiveness of OMT (in particular relating to conditionality) if put to the test. Since 2012 economic turbulence has declined, but it is unlikely to be over. The EU (and consequently the eurozone) has a sui generis institutional structure and in general relies on 19 consensus. It takes time and concessions to reach common positions. Disagreements are open, and markets pick up vulnerabilities. Again and again agreements seem to have been reached only to evaporate subsequently when the details have to be worked out. The EU is also constrained by its treaties, and this complicates the role of the ECB. Central banks in countries such as the USA, UK, China and Japan were quick to use quantitative easing to face the crisis, but the ECB is not a ‘normal’ central bank. With the main interest rate of the ECB reduced to record lows, unconventional or ‘exceptional’ methods had to be found. Article 123 of the Treaty (TFEU) forbids lending to any EU or national government or public authority and monetary financing, while Article 127 (TFEU) sets out the primary objective of price stability. There have been disagreements about whether the bond-buying programmes of the ECB comply with these restrictions, though the justification used for such measures was that otherwise the transmission mechanism for monetary policy could not operate. The threat of delay of the ESM and Fiscal Compact by the German constitutional Court has been overcome at least for now. Gradually the powers of the ECB have become more like those of other central banks. Faced with the costs and high risks of contagion of eurozone break-up or exit by one or more member states, the eurozone has edged messily towards tigher integration. Steps have been taken in the direction of a fiscal, and banking union, but the issue of legitimacy has not yet been satisfactorily resolved. The usual practice of muddling through has prevailed. Progress is piecemeal and the process causes tensions with non-eurozone countries (such as Britain over financial regulation). It seems probable that the traits of a two- or multi-speed EU will be reinforced. EU integration has always edged forward in times of crisis and this seems again be the outcome of efforts to do ‘whatever it takes to preserve the euro’. The difficult task now is that of ensuring the democratic accountability of this process, also to avoid political backlash against the economic policies being imposed.

Summary of Key Concepts

. The early years of the euro were associated with relatively low inflation (though the ceiling of two per cent was often exceeded), but rather sluggish growth. There were substantial divergences between euro member areas with regard to public sector deficits, private sector deficits and competitiveness. . The Eurozone is characterised by an asymmetry with the internal devaluations of peripheral countries not being matched by expansionary policies in countries with current account surpluses. . Many date the beginning of international economic crisis to the collapse US subprime mortgage market in 2007, though the situation deteriorated rapidly after the collapse of Lehman Brothers in 2008. The Eurozone crisis dates from early 2010 and began in Greece. . With the economic crisis bail-outs were organised for Greece, Ireland, Portugal, Cyprus and Spanish banks. These bail-outs involved the Troika of ECB, European Commission and IMF. . The role of the ECB has changed with the euro crisis. From May 2010 the ECB intervened with purchases of Greek government bonds under the Securities Market Programme (SMP). In August 2011 the SMP was extended to Spain and Italy. In December 2011 and February 2012 the ECB gave unlimited quantities of cheap three-year loans to the banks under the LTRO programme (long-term refinancing operations). In July Mario Draghi promised to do ‘whatever it takes to preserve the euro’. In September 2012 the outright monetary transactions (OMT) was agreed allowing the ECB to intervene to purchase short-term government bonds of up to three years duration.

20 . In May 2010 a three-year rescue fund, the European Financial Stability Facility (EFSF), for eurozone countries of up to €440 billion, was set up. The permanent European Security Mechanism (ESM) of €500 billion for crisis resolution in the eurozone, came into operation from 2013. It envisages with creditors bearing part of the cost of bail-outs (as occurred in the Cypriot bail-out of March 2013). . Though there has been much debate about Eurobonds, these are opposed in many circles, in particular in Germany, and have not been introduced. . In parallel with the Six Pack and Two Pack reforms of economic governance, there have been intergovernmental initiatives, in particular with the Euro-Plus Pact of March 2011 and the Fiscal Compact Treaty. The aim is tighten economic co-operation as a quid pro quo for the bail-out funds. . In September 2013 the German Constitutional Court ruled in favour of the ESM and Fiscal Compact Treaty. . Growing doubts about excessive reliance on austerity measures led to the introduction of a Pact for Growth and Jobs in June 2012, though measures have been limited. . An exit by a peripheral country such as Greece from the euro (Grexit) is likely to involve default, bank runs and probable contagion to other countries.

Questions for study and review

1 What underlying imbalances arose during the first decade of the euro and why were their consequences so serious? 2 Describe the main features of the international economic crisis. 3 Indicate the main features of the two bail-out packages for Greece? Do you think another intervention will be necessary? 4 What do you consider the main causes of the economic crisis in Ireland? 5 What were the main difficulties encountered when introducing the two EU bail-out funds (the EFSF and the ESM)? 6 Describe, giving examples, the vicious circle between sovereign debt and the banks of a country. How can this link be broken? 7 Do you think that Eurobonds should be introduced? 8 How has the role of the ECB changed with the euro crisis? 9 What are the likely consequences of a country leaving the euro? 10 What do you consider the outlook for the Eurozone?

For useful websites see the OLC to this book

Footnotes:

1 A review of the ECB video on the first 10 years of the euro in the Financial Times of 6 December 2011 awards only one star out of five. The video is criticised for pointing out advantages of the euro

21 such as the ‘ability to compare prices of vegetables in different countries’, while the only reference to the crisis is a passing mention of ‘challenges’. See the website of the ECB http://www.ecb.int/euro/html/anniversary.en.html or of the European Commission http://ec.europa.eu/economy_finance/emu10/citizens_en.htm consulted 9 February 2012.

2 The data here are taken from Eurostat. See also European Commission (2008), and Regling et al (2009).

3 Various explanations of the initial weakness of the euro were given: the faster productivity increase and more flexible markets of the USA; a few untimely statements by the first ECB president, Duisenberg; capital outflows from the EU; and the untested and cumbersome nature of EMU institutions. Some observers have also argued that market nervousness about EU enlargement also contributed to the weakening of the euro. Subsequently the strength of the euro was said to reflect factors such as international portfolio adjustment (della Posta, 2006), relatively high interest rates in the euro zone and falling confidence in the dollar (spurred also by the large US current account and fiscal deficits). 4 The statistics here are taken from Nomura (2011). Private indebtedness also rose to 187 per cent of GDP for Portugal in 2009. 5 These are sometimes called the ‘PIGS’, and though the ‘I’ initially indicated Ireland, subsequently it was often taken to refer to Italy and the term ‘PIIGS’ is also used.

6 Paul Krugman suggested giving a voucher worth €1000 to all Germans to spend in the southern EU states (as reported in Mario Nuti’s blog, Transition at http://dmarionuti.blogspot.it/ accessed 13 September, 2012).

7 The 2012 State Aid Scoreboard http://ec.europa.eu/competition/state_aid/studies_reports/2012_autumn_working_paper_en.pdf accessed 2 August 2013. 8The rise in international economic uncertainty already began earlier. A major setback in terms of promoting the creation of a fully-fledged ‘knowledge-based economy’ was the series of technology, media and telecoms (TMT) stock crashes that occurred between March 2000 and late 2002, and impacted massively on investors’ confidence around the world. This was followed by a string of accounting scandals (Worldcom, Enron, and so on). The overall impact was to undermine confidence in the robustness of western economies.

9 The term subprime refers to the quality of the borrowers, who have a poor credit history and greater risk of default than ‘prime’ borrowers. See Kindleberger (2000) or Minsky (1980) for a typology of crises

10 The literature is vast and growing rapidly. See, for example, BIS (2009 and 2010), Brunnermeir (2009), European Commission (2009d), IMF (2010a and b), Nomura (2011), the OECD (2010), Vercelli (2010) and various issues of the Financial Times (where Martin Wolf, in particular, attaches much importance to the problem of global imbalances). See http://www.ft.com/comment/columnists/martinwolf accessed 10 February 2011. 11 See the annual reports of the BIS (Bank for International Settlements, 2009 and 2010) for a discussion of these various causes. 12 The increasing use of securitisation or the transformation of non-traded assets and liabilities into traded securities entailed transformation from a banking model of ‘originate and hold’ to one of ‘originate and distribute’. Securities such as mortgage-based securities (MBS), which involved bundling mortgages of increasingly high risk, played a key role in transmitting the housing crisis to financial markets. Collateralised debt obligations (CDOs) involved forming a diversified portfolio

22 of mortgages, other types of loan, government bonds etc. The portfolios were then divided into ‘tranches’ and sold to investors with differing propensity for risk. Those buying tranches and bonds could also cover themselves by buying credit default swaps (CDS), or contracts to insure against the default of a particular bond or tranche. In practice the opacity and complexity of these securities often meant that the market failed to price them accurately, and underestimated their systemic risk. The US authorities allowed the self-regulation of this over-the-counter ‘derivatives market. In 2003 Warren Buffett, the ‘Sage of Omaha’ or famous economic commentator, referred to these derivatives as ‘weapons of mass destruction’. See Brunnermeier (2009) for a description of these instruments, and the risks involved.

13Models often assumed that the distribution of returns on many different assets was normal and so had thin tails. As Taleb (2010) pointed out, what was needed was ‘black swan rationalisation’ with adequate account being taken of high impact rare developments (‘fat tails’).

14 Some economists such as Daniel Gros and Thomas Mayer called for the creation of a European Monetary Fund, see their article in The Economist, 20 February 2010.

15 The European Financial Stabilisation Mechanism depends on funds raised by the Commission using the EU budget as collateral.

16 Loans of the six main Irish Banks doubled in four years to reach €409 billion in 2007 when the Irish property market turned (Irish Times, 31 May 2010).