Carry Forward Balances – from Fiscal Year 2016/2017 An Information Bulletin from Analysis, Planning & Budget and Financial Services – April 30, 2017

Table of Contents Carry Forward Rules - QUICK REFERENCE:...... 1 1A – OPERATING/UNIVERSITY ALLOCATION FUNDS...... 2 1B – OPERATING/SELF-FINANCING FUNDS:...... 5 1C, 1E, 1F - UNRESTRICTED NON-GRANT FUNDS:...... 5 1D - CLEARING FUNDS:...... 6 1E & 1F - UNRESTRICTED SELF-FINANCING GRANT-RELATED FUNDS:...... 6 2 - RESTRICTED FUNDS NOT LINKED TO GRANTS (all 2’s except 2L):...... 6 2 - RESTRICTED GRANT-RELATED FUNDS:...... 7 TRUST FUNDS (all 8’s except 8A, 8L, 8M):...... 8 9A – BASE CAPITAL EQUIPMENT FUNDS:...... 8 Appendix A – Legend of Abbreviations and Glossary of Terms...... 10 Appendix B – Example of a Carry Forward based on Cumulative Fund Balance...... 11 Appendix C – Organization codes for faculties and libraries...... 13 Appendix D – Funds excluded from the faculty and libraries transfer (step4)...... 14

A “Carry Forward Balance” or “Cumulative Surplus/Deficit” is an amount that is posted as a budget in the new fiscal year, representing the prior year’s cumulative results. This budget appears each May in account code 700421, 700422 or 700428 (depending on the Fund Type), and carries a document number starting with ‘CF’. The budget carry forward is usually posted at the end of May (after final cut off).

A positive budget will increase your current year spending power due to past accumulated surplus. A negative budget will decrease your current year spending power due to a past over-expenditure.

The rules used to calculate the balance forwards differ by Fund Type. If you do not know the fund type of your fund, it is located at the top of your Monthly Fund/Grant Details report under Minerva >> Finance (Fund) Administration menu >> Financial Statements, or use form FTMFUND in Banner INB.

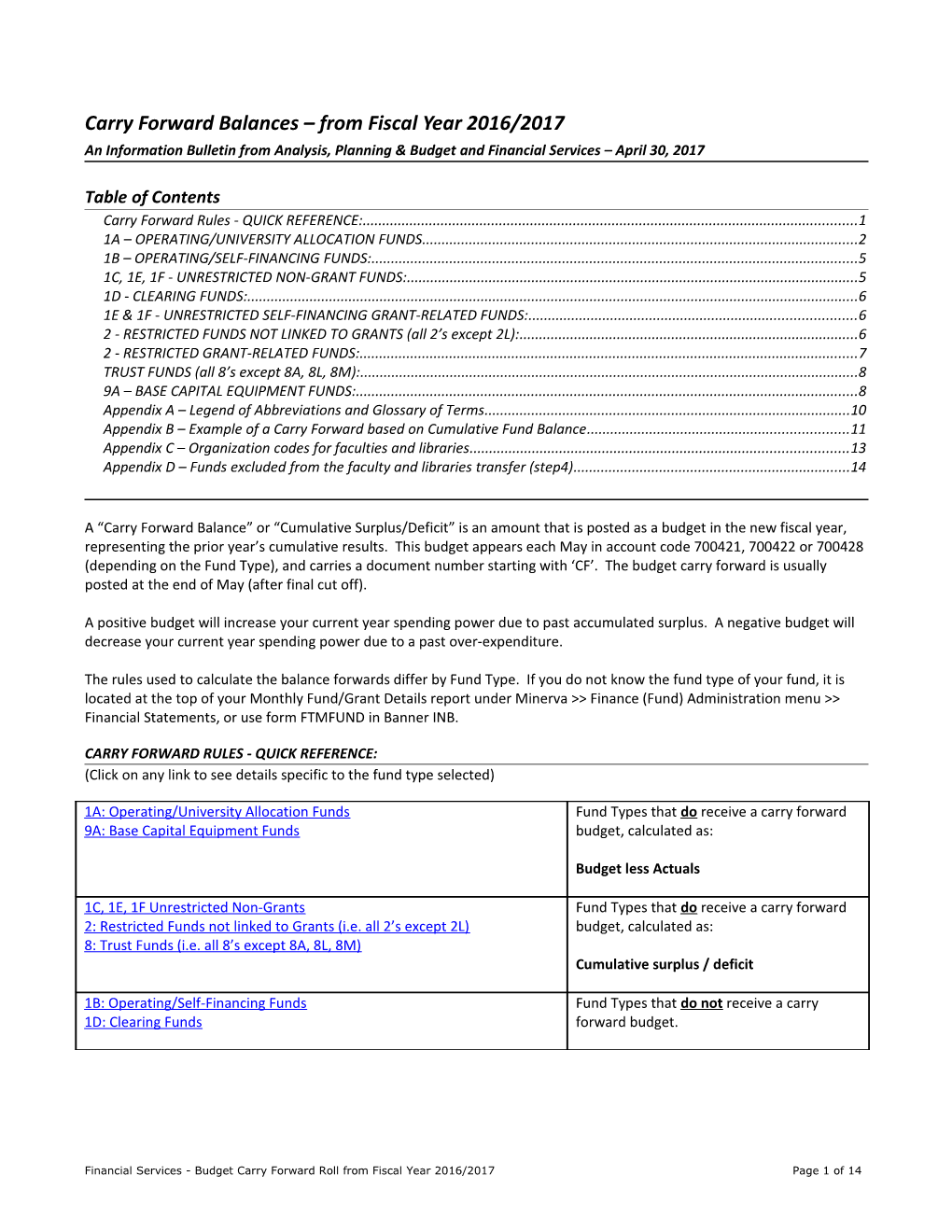

CARRY FORWARD RULES - QUICK REFERENCE: (Click on any link to see details specific to the fund type selected)

1A: Operating/University Allocation Funds Fund Types that do receive a carry forward 9A: Base Capital Equipment Funds budget, calculated as:

Budget less Actuals

1C, 1E, 1F Unrestricted Non-Grants Fund Types that do receive a carry forward 2: Restricted Funds not linked to Grants (i.e. all 2’s except 2L) budget, calculated as: 8: Trust Funds (i.e. all 8’s except 8A, 8L, 8M) Cumulative surplus / deficit

1B: Operating/Self-Financing Funds Fund Types that do not receive a carry 1D: Clearing Funds forward budget.

Financial Services - Budget Carry Forward Roll from Fiscal Year 2016/2017 Page 1 of 14 The rest of this document elaborates on these fund types, shows the calculation details with examples, and contact information should you have questions.

Appendix A shows a Legend of Abbreviations and a Glossary of Terms for your convenience.

1A – OPERATING/UNIVERSITY ALLOCATION FUNDS

Fund description: 1A funds represent a unit’s fundamental and ongoing operations funded by the University budget allocation. For more details, refer to the Fund Type Overview.

All Operating Funds are affected by items 1 and 2 below however only Faculty and Libraries’ funds are affected by item 3 and only Administrative Units are affected by item 4.

1) The carry forward is calculated as Budget less Actuals.

2) There is no supplementary budget roll for prior year encumbrances.

3) Faculties and Libraries:

Any resulting surplus budget carry forward, calculated at the Faculty level is eliminated and a corresponding amount is setup in specific Faculty Reserve Funds. Any resulting annual deficit budget carry forward, calculated at the Faculty level is consolidated in one fund under the responsibility of the Dean. Appendix C lists all organizational units affected by this step.

4) Administrative Units

All free balance carry forwards, at the major unit level are applied towards the University’s operating deficit.

Steps in the 1A Carry Forward Calculation: The budget carry forward is done in a series of steps. In all steps, a fund population is extracted and then the requisite calculation is made and posted before moving on to the next step. The summarized steps are shown here followed by a more detailed explanation.

1) Calculate Budget Carry Forward and post to each fund – Budget less Actuals. 2) Backoff surplus/deficit in benefits accounts. 3) Backoff all carry forwards to funds under fund predecessor 1010 - “Central University Allocation Funds”

Carry forward is complete at this point for all units not identified as Faculties/Libraries in Appendix C and for funds explicitly excluded from the Faculty/Libraries calculation in Appendix D.

4) Determine net surplus/deficit for Faculty/Libraries. a. Surplus: Backoff all carry forwards and post consolidated surplus amount to account 400010 in Surplus Reserve Fund. b. Deficit: Backoff all carry forwards and post consolidated deficit amount to account 700421 in Deficit Fund.

5) Administrative units with a free balance carry forward will have that carry forward applied to the University deficit.

Step 1: How the carry forward is calculated & posted: Budget Carry Forward = Budget less Actuals (Cents >= $0.50 are rounded up, otherwise dropped)

Financial Services - Budget Carry Forward Roll from Fiscal Year 2016/2017 Page 2 of 14 This calculation is applied to each FOAPAL combination and will be recorded as a temporary budget. A free balance is posted as a positive number and an over expenditure is posted as a negative number.

The Budget Module will carry a separate record for every FOAPAL combination, each with a description indicating the original Organization/Account/Program codes it relates to. For example: “BUD C/F 12345/500001/1000” where 12345 = organization code, 500001 = account code, 1000 = program code. These records are ultimately posted as a consolidated entry in the operating ledger to Account code 700421 and to the fund’s default Organization and Program codes, with an Activity and Location code of 000000.

To illustrate:

Prior Year (Ending Balance): Fund Org Account Prog Activity Location Budget YTD Activity Commit Balance 151901 12345 500001 1000 000000 000000 700.00 400.00 0.00 300.00 151901 12345 700004 1000 001234 000000 0.00 500.00 0.00 -500.00 151901 12345 700004 1000 000000 567890 0.00 100.00 0.00 -100.00 151901 12345 700004 1000 000000 000000 1,000.00 180.40 0.00 819.60 151901 12345 700006 1000 000000 000000 0.00 11,225.30 0.00 -11,225.30 151901 12345 700006 1000 001234 000000 0.00 4,000.00 0.00 -4,000.00 151901 12345 700007 1000 000000 000000 4,050.00 0.00 4,050.00 0.00 151901 12345 700421 1000 000000 000000 22,500.00 0.00 0.00 22,500.00 Total 26,850.00 15,605.70 4,050.00 7,194.30

In the New Year, the Prior Year Carry Forward Balance is represented in the Budget Module as follows: Fund Org Account Prog Activity Location Budget Description 151901 12345 700421 1000 000000 000000 -300 BUD C/F 12345/500001/1000 151901 12345 700421 1000 000000 000000 -500 BUD C/F 12345/700004/1000 151901 12345 700421 1000 000000 000000 -100 BUD C/F 12345/700004/1000 151901 12345 700421 1000 000000 000000 820 BUD C/F 12345/700004/1000 151901 12345 700421 1000 000000 000000 -11,225 BUD C/F 12345/700006/1000 151901 12345 700421 1000 000000 000000 -4,000 BUD C/F 12345/700006/1000 151901 12345 700421 1000 000000 000000 4,050 BUD C/F 12345/700007/1000 151901 12345 700421 1000 000000 000000 22,500 BUD C/F 12345/700421/1000 Total 11,245

The above Budget Module records are posted to the Operating Ledger in the New Year as two consolidated entries (sum of account free balances, and sum of account over-expended balances), using a document number starting with ‘CF’:

Fund Org Account Prog Activity Location Budget Description 151901 12345 700421 1000 000000 000000 27,370.00 151901 BUDGET CARRY FORWARD ROLL 151901 12345 700421 1000 000000 000000 -16,125.00 151901 BUDGET CARRY FORWARD ROLL Total 11,245.00

Step 2: Backoff surplus/deficit in benefits accounts

In 1A funds, benefit expenditures are automatically covered by a budget provided by the University and posted to account 600125. As such, any resulting surplus or over expenditure in the benefit account codes is removed from the Budget Carry Forward calculation. The description for these postings reads as “REV. C/F BENEFITS” in the Budget Module, and “BUDGET CARRY FORWARD ROLL” in the Operating Ledger.

Financial Services - Budget Carry Forward Roll from Fiscal Year 2016/2017 Page 3 of 14 Step 3: Backoff all carry forwards to funds under fund predecessor 1010 - “Central University Allocation Funds”

Funds classified as Central University Allocation Funds are not entitled to a budget carry forward. The carry forward is calculated and posted for these funds and then removed entirely.

In rare cases, some faculties have funds in this category however most do not.

Step 3 marks the end of the Budget Carry Forward calculation for Administrative units (units not listed in Appendix C).

Step 4: Determine net surplus/deficit for Faculty/Libraries.

This step is exclusive to the organizational units listed in Appendix C; the list consists of all Faculties and the Libraries.

The total of all carry forward amounts for a given Faculty will be calculated to determine a net surplus (positive amount) or net deficit (negative amount). In either case, the carry forwards for each fund are backed out and the corresponding amount posted to a Surplus Reserve Fund in the case of a net surplus or a Deficit Fund in the case of a net deficit.

a) James McGill, William Dawson, TALIF, Chantier II and IRDC funds are excluded from the consolidated calculation. If these funds have a carry forward, it is not backed out. See Appendix D for further information.

b) Fund affiliation to a given Faculty or to the Libraries is determined by the organization code default of the fund.

c) Funds rolling up to predecessor fund code 1010 are excluded from the consolidated calculation because these funds do not get a carry forward. Most Faculties aren’t affected by this. See Step 3 above for more information.

Surplus amounts will be posted to account 400010 in the Faculty’s Surplus Fund. Deficit amounts will be posted as a budget to account 700421 of the Faculty’s Deficit Fund.

Query/Reporting tips: Use the Budget Module form FZIBLFP to query budget transactions by FOAPAL (in this case the account code would be 700421) and to drill down to the document details. Conversely, from a document number on FGIDOCR in Finance, you may select “Budget Document Drill Down” from the Options menu to see the corresponding Budget Module details.

The consolidated Operating Ledger posting(s) can be viewed using Banner forms FGIBDST (How to query the balance of a fund in FGIBDST) or FGITRND (How to view transaction detail activity in FGITRND). They will appear as transactions on your Monthly Fund Details report for May and easily identified by looking for document codes starting with ‘CF.’

To see your funds in the context of the 4 steps laid out above, use Crystal Web Template entitled “Budget Carry Forward” in the Summary Reports section of the Financial Services website. The report must be run for the prior fiscal year.

Questions? Please direct all questions to your fund administrator in the Unrestricted Accounting Office. Contact information is displayed in the Summary of Free Balances by User Security (FZRG0055) report under Minerva >> Finance (Fund) Administration menu >> Financial Statements, or in form FTMFUND in Banner INB.

1B – OPERATING/SELF-FINANCING FUNDS:

Financial Services - Budget Carry Forward Roll from Fiscal Year 2016/2017 Page 4 of 14 Fund description: 1B funds represent a unit’s fundamental and ongoing self-funded operations. These funds are required to submit a formal budget each year. For more details, refer to the Fund Type Overview.

Why a carry forward is not calculated: These funds do not automatically receive a budget carry forward amount. If the use the free balance of a previous year is required, it must be addressed during the Agreement discussions. If authorized, the unit Financial Budget Model (FBM) submitted, for the respective annual exercise, must reflect the expenditures. . A repayment plan is imposed in cases of accumulated deficits. The accumulated profit or loss of each fund is found in the fund balance (account code 400003).

Query/Reporting tips: To view fund balance accounts, you may use the Web report template “Trial Balance Summary” in the General Ledger Reports section of the Financial Services website. Alternatively, one may consult the Banner form FGITBSR to view this balance.

Questions? Please direct all questions to your fund administrator in the Unrestricted Accounting Office. Contact information is displayed in the Summary of Free Balances by User Security (FZRG0055) report under Minerva >> Finance (Fund) Administration menu >> Financial Statements, or in form FTMFUND in Banner INB.

1C, 1E, 1F - UNRESTRICTED NON-GRANT FUNDS:

How the carry forward is calculated & posted: Budget Carry Forward = Fund Balance (i.e. cumulative profit or loss) as found on the General Ledger under account code 400003 @ April 30th. Note: this calculation only considers “Actuals”.

The Fund Balance is determined by Fund code and will be recorded as a temporary budget. A cumulative Surplus is posted as a positive number and a cumulative Deficit is posted as a negative number.

A single record is posted to the Fund on the Operating Ledger, using that Fund’s Org and Prog, and the account code 700422. The description is “C/F CUM SURPLUS/DEFICIT.”

See Appendix B for an example of how Cumulative Fund Balances Carry Forwards are calculated.

Query/Reporting tips: This single entry can be viewed from Banner form FGIBDST (How to query the balance of a fund in FGIBDST) or FGITRND (How to view transaction detail activity in FGITRND). It will appear as a transaction on your Monthly Fund Details report for May as a document code starting with ‘CF.’

To view fund balance accounts, you may use the Web report template “Trial Balance Summary” in the General Ledger Reports section of the Financial Services website. Alternatively, one may consult the Banner form FGITBSR to view this balance.

Questions? Please direct all questions to your fund administrator in the Unrestricted Accounting Office. Contact information is displayed in the Summary of Free Balances by User Security (FZRG0055) report under Minerva >> Finance (Fund) Administration menu >> Financial Statements, or in form FTMFUND in Banner INB. 1D - CLEARING FUNDS:

Financial Services - Budget Carry Forward Roll from Fiscal Year 2016/2017 Page 5 of 14 Fund description: 1D funds are clearing funds and therefore all balances must be cleared at the end of every fiscal year. Hence there should be no carry forward generated in the first place. For more details, refer to the Fund Type Overview.

Questions? Please direct all questions to your fund administrator in the Unrestricted Accounting Office. Contact information is displayed in the Summary of Free Balances by User Security (FZRG0055) report under Minerva >> Finance (Fund) Administration menu >> Financial Statements, or in form FTMFUND in Banner INB.

1E & 1F - UNRESTRICTED SELF-FINANCING GRANT-RELATED FUNDS:

Fund description: 1E and 1F are unrestricted funds linked to a grant code for inception-to-date reporting. For more details, refer to the Fund Type Overview.

Why a carry forward is not required: Grant balances are calculated from inception-to-date. That is, a grant balance incorporates all transactions from the beginning of the grant to the present day regardless of how many fiscal years the grant may span. Regular funds without a grant work on the year-to-date principle and so they “close” at the end of each fiscal year and start the new fiscal year at zero necessitating a carry forward to be posted from the previous year to the current year.

Due to the inception-to-date concept, balance forward amounts need not be posted to grants. However, to allow for systematic ‘budget availability checking’, an entry is processed to reflect the grant’s status. This entry does not impact the balances depicted on grant queries or reports because it does not post to the grant ledger.

Query/Reporting tips: Use Minerva “Budget Query for Fund Holders” or Banner form FRIGITD (Grant Inception to Date) to view the cumulative results for a fund (How to query a grant balance in FRIGITD). As the name suggests, it shows all activity on a Grant from the date the grant is created to the present. As an alternative use the report “Monthly Grant Details” from Minerva Reports (Financial Statements) or the Web report template “Monthly Grant Details” located in the Month End Reports section of the Financial Services website.

Questions? Please direct all questions to your fund administrator in the Unrestricted Accounting Office. For inquiries relating to 1F funds, you may contact your fund administrator in the Research Financial Management Services. Contact information is displayed in the Summary of Free Balances by User Security (FZRG0055) report under Minerva >> Finance (Fund) Administration menu >> Financial Statements, or in form FTMFUND in Banner INB.

2 - RESTRICTED FUNDS NOT LINKED TO GRANTS (ALL 2’S EXCEPT 2L):

Fund description: Fund types starting with a ‘2’ that are not linked to a grant code represent restricted activity for which inception-to-date reporting is not required. These funds typically receive a budget to spend as revenues are recorded. For more details, refer to the Fund Type Overview.

How the carry forward is calculated & posted:

Financial Services - Budget Carry Forward Roll from Fiscal Year 2016/2017 Page 6 of 14 Budget Carry Forward = Fund Balance (i.e. cumulative profit or loss) as found on the General Ledger in account code 400006 @ April 30th. Note: this calculation only considers “Actuals”.

The Fund Balance is determined by Fund code and will be recorded as a temporary budget. A cumulative Surplus is posted as a positive number and a cumulative Deficit is posted as a negative number.

A single record is posted to the Operating Ledger for that Fund, using the Org and Prog defaults for that fund, and the account code 700422. The description is “C/F CUM SURPLUS/DEFICIT.”

See Appendix B for an example of how Cumulative Fund Balances Carry Forwards are calculated.

Query/Reporting tips: This single entry can be viewed from Banner form FGIBDST (How to query the balance of a fund in FGIBDST) or FGITRND (How to view transaction detail activity in FGITRND) as a document number starting with ‘CF.’ It will appear as a transaction on “Monthly Fund Details” from Minerva Reports (Financial Statements), or use the Web report template “Monthly Fund Details” located in the Month End Reports section of the Financial Services website.

Questions? Please direct all questions to your fund administrator in the Research Financial Management Services. Contact information is displayed in the Summary of Free Balances by User Security (FZRG0055) report under Minerva >> Finance (Fund) Administration menu >> Financial Statements, or in form FTMFUND in Banner INB.

2 - RESTRICTED GRANT-RELATED FUNDS:

Fund description: Fund types starting with ‘2’ and are linked to a grant code to support inception-to-date reporting. For more details, refer to the Fund Type Overview.

Why a carry forward is not required: Grant balances are calculated from inception-to-date. That is, a grant balance incorporates all transactions from the inception of the grant to the present day regardless of how many fiscal years the grant may span. Regular funds without a grant work on the year-to-date principle and so they “close” at the end of each fiscal year and start the new fiscal year at zero necessitating a carry forward to be posted from the previous year to the current year.

Due to the inception-to-date concept, balance forward amounts need not be posted to grants. However, to allow for systematic ‘budget availability checking’, an entry is processed to reflect the grant’s status. This entry does not impact the balances depicted on grant queries or reports because it does not post to the grant ledger.

Query/Reporting tips: Use Minerva “Budget Query for Fund Holders” or Banner form FRIGITD (Grant Inception to Date) to view the cumulative results for a fund (How to query a grant balance in FRIGITD). As the name suggests, it shows all activity on a Grant from the date the grant is created to the present. As an alternative use the report “Monthly Grant Details” from Minerva Reports (Financial Statements) or the Web report template “Monthly Grant Details” located in the Month End Reports section of the Financial Services website.

Questions? Please direct all questions to your fund administrator in the Research Financial Management Services. Contact information is displayed in the Summary of Free Balances by User Security (FZRG0055) report under Minerva >> Finance (Fund) Administration menu >> Financial Statements, or in form FTMFUND in Banner INB. TRUST FUNDS (ALL 8’S EXCEPT 8A, 8L, 8M):

Financial Services - Budget Carry Forward Roll from Fiscal Year 2016/2017 Page 7 of 14 Fund description: Fund Types starting with ‘8’ are funds owned by affiliated yet legally separate entities for which the University provides bookkeeping services. For more details, refer to the Fund Type Overview.

How the carry forward is calculated & posted: Budget Carry Forward = Fund Balance as found on the General Ledger under account code 400015 @ April 30th. Note: this calculation only considers “Actuals”.

The Fund Balance is determined by Fund code and will be recorded as a temporary budget. A cumulative Surplus is posted as a positive number and a cumulative Deficit is posted as a negative number.

A single record is posted to the Fund on the Operating Ledger, using that Fund’s Org and Prog, and the account code 700422. The description is “C/F CUM SURPLUS/DEFICIT.”

See Appendix B for an example of how Cumulative Fund Balances Carry Forwards are calculated.

Query/Reporting tips: This single entry can be viewed from Banner form FGIBDST (How to query the balance of a fund in FGIBDST) or FGITRND (How to view transaction detail activity in FGITRND). It will appear as a transaction on your Trust Fund Details Minerva report (Financial Statements) for May as a document code starting with ‘CF.’

To view fund balance accounts, you may use the Web report template “Trial Balance Summary” in the General Ledger Reports section of the Financial Services website. Alternatively, one may consult the Banner form FGITBSR to view this balance.

Questions? Please direct all questions to your fund administrator in the Unrestricted Accounting Office. Contact information is displayed in the Summary of Free Balances by User Security (FZRG0055) report under Minerva >> Finance (Fund) Administration menu >> Financial Statements, or in form FTMFUND in Banner INB.

9A – BASE CAPITAL EQUIPMENT FUNDS:

Fund description: 9A funds represent a unit’s base capital equipment allocation funded by the University’s capital grant from the provincial government. For more details, refer to the Fund Type Overview.

How the carry forward is calculated & posted: Budget Carry Forward = Budget less Actuals

The carry forward balance is calculated for each FOAPAL combination and will be recorded as a temporary budget. A free balance is posted as a positive number and an over expenditure is posted as a negative number.

A consolidated entry will be posted for each Fund-Org-Account-Prog combination to account code 700421 and to the fund’s default Organization and Program codes, with the Activity and Location codes set to 000000. The transaction description will indicate the original Organization, Account and Program codes it relates to. For example: “BUD C/F 12345/500001/1000 where 12345 = organization code, 500001 = account code, 1000 = program code.

To illustrate:

Financial Services - Budget Carry Forward Roll from Fiscal Year 2016/2017 Page 8 of 14 Year 01 (Ending Balance): Fund Org Account Prog Activity Location Budget YTD Activity Commit Balance 900004 12345 700004 1000 001234 000000 0.00 500.00 0.00 -500.00 900004 12345 700004 1000 000000 567890 0.00 100.00 0.00 -100.00 900004 12345 700004 1000 000000 000000 1,000.00 180.40 0.00 819.60 900004 12345 700006 1000 000000 000000 0.00 11,225.30 0.00 -11,225.30 900004 12345 700006 1000 001234 000000 0.00 4,000.00 0.00 -4,000.00 900004 12345 700007 1000 000000 000000 4,050.00 0.00 4,050.00 0.00 900004 12345 700421 1000 000000 000000 22,500.00 0.00 0.00 22,500.00 Total 27,550.00 16,005.70 4,050.00 7,494.30

In Year 02, the Year 01 Carry Forward Balance is represented as follows: Fund Org Account Prog Activity Location Budget Description 900004 12345 700421 1000 000000 000000 -500.00 BUD C/F 12345/700004/1000 900004 12345 700421 1000 000000 000000 -100.00 BUD C/F 12345/700004/1000 900004 12345 700421 1000 000000 000000 819.60 BUD C/F 12345/700004/1000 900004 12345 700421 1000 000000 000000 -11,225.30 BUD C/F 12345/700006/1000 900004 12345 700421 1000 000000 000000 -4,000.00 BUD C/F 12345/700006/1000 900004 12345 700421 1000 000000 000000 4,050.00 BUD C/F 12345/700007/1000 900004 12345 700421 1000 000000 000000 22,500.00 BUD C/F 12345/700421/1000 Total 11,544.30

Query/Reporting tips: This single entry can be viewed from Banner form FGIBDST (How to query the balance of a fund in FGIBDST) or FGITRND (How to view transaction detail activity in FGITRND) as a document number starting with ‘CF.’ It will appear as a transaction on “Monthly Fund Details” from Minerva Reports (Financial Statements), or use the Web report template “Monthly Fund Details” located in the Month End Reports section of the Financial Services website.

Questions? Please direct all questions to your fund administrator in the Capital Projects Accounting Office. Contact information is displayed in the Summary of Free Balances by User Security (FZRG0055) report under Minerva >> Finance (Fund) Administration menu >> Financial Statements, or in form FTMFUND in Banner INB.

Financial Services - Budget Carry Forward Roll from Fiscal Year 2016/2017 Page 9 of 14 APPENDIX A – LEGEND OF ABBREVIATIONS AND GLOSSARY OF TERMS

Legend of Abbreviations Abbreviation Terminology BUD Budget C/F Carry Forward CUM Cumulative REV Reversal

Glossary of Terms Terminology Definition Actuals Refers to expenses and/or revenues that have been spent or received. Differs from budget dollars which are an estimation of what will happen and commitments which are funds reserved for future expenses. Deficit A situation where a fund’s balance is negative, also known as overdraft. That is, more money has been spent than is allowed for by the budget and/or revenue. Alternatively, when referring to the general ledger, a deficit denotes a situation where the cumulative fund balance is negative. Free Balance Refers to an amount that is free to spend. That is, the fund in question has spending power. This term is typically used in reference to the operating ledger or grant ledger. Overspent/Over expenditure/”OE”/”o/e” A negative balance. See “Deficit” Temporary Budget Budget amount (adopted or an adjustment) that is non- recurring in nature, and is therefore not included in any future year budget allocation. Cumulative Fund Balance Typically refers to the General Ledger account codes starting with 4. This represents the sum of assets less liabilities over the life of a fund. In layman’s terms this is the “net worth” of the fund for all time and determines an overall state of surplus funds or a lack of funds (deficit). It is possible to have spending power in a given year but have a fund balance in a deficit position (indicates overspending in prior years). A cumulative fund balance is often said to be either in a surplus or deficit position (see related definitions). Cumulative Surplus/Deficit See “Cumulative Fund Balance” Inception to date A term particular to grants denoting the principle by which the grant’s balance is calculated by incorporating all transactions from the beginning of the grant’s life (inception) to the current date. This differs from funds that aren’t linked to grants that use the “year to date” principle. Surplus A situation where a fund’s balance is positive, also known as a free balance. That is, more money remains than has been spent budget and/or revenue. Alternatively, when referring to the general ledger, a surplus denotes a situation where the cumulative fund balance is positive. Year to date Also known as YTD. A term particular to funds that aren’t linked to a grant (see “Inception to date” for more information). Year to date balances are calculated based on transactions from the beginning of the fiscal year (May 1) to the present date.

Financial Services - Budget Carry Forward Roll from Fiscal Year 2016/2017 Page 10 of 14 APPENDIX B – EXAMPLE OF A CARRY FORWARD BASED ON CUMULATIVE FUND BALANCE

Cumulative Fund Balances are tracked in the General Ledger of the Banner Financial Information System. Day-to-day transactions such as revenues and expenses are tracked and represented as Assets, Liabilities and Cumulative Fund Balance. Most Banner finance users do not refer to the General Ledger but rather to the Operating Ledger or the Grant Ledger.

To view fund balance accounts, you may use the Web report template “Trial Balance Summary” in the General Ledger Reports section of the Financial Services website. Alternatively, one may consult the Banner form FGITBSR to view this balance.

The example below shows a fund over the course of 3 years:

At the end of the first year the Cumulative Fund Balance is a surplus of $2,000. At the end of the second year the fund has a $1,000 Cumulative Fund Balance in a deficit position. A surplus carry forward imparts additional spending power in the new year whereas a negative or deficit carry forward detracts from spending power in the new year effectively recovering the debt incurred by previous overspending.

Note: If this sample fund had been a 1A Operating fund and its carry forward calculated as Budget less Actuals then after the first year the carry forward would be $2,000. At the end of second year it would be a negative $1,000 (deficit carry forward).

Year 01: The Fund is opened in Year 01 with a balanced budget as shown here: Budget Actuals Encumbrance Balance Revenue -5,000 -5,000 0 0 Expenses 5,000 3,000 500 1,500 Total 0 -2,000 500 1,500

Year 02: A surplus (accumulated revenue > expenses) Carry Forward transaction from Year 01 is posted in Year 02 as shown here:

Account Title Adj. Budget YTD Activity Balance 700422 Cumulative Surplus/Deficit 2,000 0.00 2,000 [Note: only Actuals are considered in this calculation]

Year 02 Revenue & Expenditures plus Carry Forward from Year 01 Yr02 Budget Actuals Encumbrance Balance Revenue -4,000 -4,000 0 0 Expenses 4,000 7,000 500 -3,500 700422 2,000 0 0 2,000 Total 2,000 3,000 500 -1,500

The Budget Carry Forward from Year 02 is calculated as the accumulated results of the Fund, i.e. the sum of each year’s performance: Year Carry Forward Balance Adj. Budget 01 Surplus 2,000 02 Deficit -3,000 Accumulated results: -1,000

Financial Services - Budget Carry Forward Roll from Fiscal Year 2016/2017 Page 11 of 14 Year 03: A deficit (accumulated revenue < expenses) Carry Forward from Year 02 posted in Year 03:

Account Title Adj. Budget YTD Activity Balance 700422 Cumulative Surplus/Deficit -1,000 0 -1,000

Financial Services - Budget Carry Forward Roll from Fiscal Year 2016/2017 Page 12 of 14 APPENDIX C – ORGANIZATION CODES FOR FACULTIES AND LIBRARIES

Organization Code Organization Name 90020 Faculty of Agricultural & Environmental Sciences 90021 Faculty of Arts 90022 School of Continuing Studies 90023 Faculty of Dentistry 90024 Faculty of Education 90025 Faculty of Engineering 90027 Faculty of Law 90028 Desautels Faculty of Management 90029 Faculty of Medicine 90030 Schulich School of Music 90032 Faculty of Science 90034 Libraries

Financial Services - Budget Carry Forward Roll from Fiscal Year 2016/2017 Page 13 of 14 APPENDIX D – FUNDS EXCLUDED FROM THE FACULTY AND LIBRARIES TRANSFER (STEP4)

The list of predecessor fund codes below is used to identify funds that will not be included in the Faculty and Libraries transfer (Step 4 of the budget carry forward roll).

The INB form FTMUND can be used to see if a given fund falls under one of these fund predecessors. Use the query functionality of the form to look up the 6 digit fund in question and then look at the “Predecessor Fund” field.

Title Predecessor Code IRDC 10052 James McGill 10055 William Dawson 10056 TALIF 10066 Chantier II 10068 Special Provisions for BCF 10069

Financial Services - Budget Carry Forward Roll from Fiscal Year 2016/2017 Page 14 of 14