France Exchange Visit Report, 11-12 September 2008, Nice/Toulon

10 persons from seven different organisations and seven different countries (Albania, Bulgaria, Italy, Macedonia, Netherlands, Poland, UK) participated in the France exchange visit organised by EMN secretariat from 11th to 12th of September 2008. It gave the participants the possibility to discover the work of Adie. On the first morning the participants met in the premises of one of Adie’s main bank partners, BNP Paribas. After a presentation of EMN by EMN Executive Director P. Guichandut and a short presentation of the exchange visit participants, S. Antamarian, the Regional Director of Adie PACA, gave an introduction to the work of Adie. Afterwards, the group split into two. The first group stayed in Nice where participants had the possibility to discuss with the Adie loan officers on the spot. Moreover, a presentation about Adie’s BDS services was given, including a discussion with an Adie volunteer. On the second day this group went to Cannes, about 30 minutes from Nice where the participants met with the Adie partner Créactive, a business incubator (“couveuse”) and with two microentrepreneurs, one holding a shop where he sells street wear and one restaurant owner. The second group went to Toulon, about two hours from Nice for a discussion with the Adie team (loan officers, support staff and volunteers), visited a “Boutique de Gestion” (French business support structure) and met a microentrepreneur (Indian product and clothes shop) and the local market.

Question studies - Learning points 1) The French social welfare system – transition from unemployment to self-employment France has a system of social welfare which supports persons who would like to start a business. Persons who receive RMI (revenue minimum d’insertion – social welfare for those who have exhausted unemployment benefits) have the right to a start-up support programme called ACCRE which allows new entrepreneurs to continue to receive social welfare and exonerates them from paying social charges for the first 6–12 months of the new business. This period can be extended if the authorities esteem that the business is not yet sustainable.

1 2) Adie structure - Adie headquarters in Paris houses the loan management system (GAIA) and lobbying activities. - For its work, Adie has divided France in operational regions which do not correspond to the political division. This regional division has been made with regard to profitability aspects. - In the PACA region Adie has a microcredit portfolio of 3 million € = 850 credits. - Since 2007 Adie has clearly separated its support activities from its credit activities. It has opened one branch as pilot project which is expected to become self-sustainable. 3) Clients/sectors - Clients are heterogeneous. Their levels of studies cover illiterate persons as well as those with higher studies. Half of Adie clients come from urban areas and 25% from rural areas (with less than 5000 inhabitants). Disadvantaged urban neighbourhoods are also Adie’s target areas. 18% of the clients are unemployed and 7% come from the Roma population. - Most of the financed activities are start-ups with less than 5 years and in the trade and service sectors (low investment needs). - Adie measures the survival rate of financed businesses, but also what it calls the “rate of re-integration into the labour marker” (“taux d’insertion”) which is much higher than the survival rate of the businesses. This corresponds to Adie’s social mission (see Adie power point presentation). - Adie can finance activities in the grey economy. It supports them to incite them to become formal. 4) Types of loans and loan amount - Typical Adie microloans have a 9.71% interest rate + 5% commission. The average amount of a microloan is 3000€. - A “prêt d’honeur » (honnour loan) is generally provided in complement to an Adie microloan. It increases the final loan amount for the client and is provided depending on the type of projects (cash flow projection). It is financed through regional grants and has 0% interest. Normally, the honour loan is only a small additional amount and does not represent more than 10% of the amount of the microloan (f.ex. 4000€ microloan + 500€

2 honour loan). The honour loan has to be paid back at the same time as the microloan. - Additionally, a start-up loan called EDEN (State aid) can complement the first two types of loans. - In general the global amount (including microloan, EDEN and honour loan) that may be obtained from Adie does not exceed 8000€ (Adie political decision). - Adie can provide a second loan even if the person has not yet totally paid back the first one, if he/she has not yet access to bank credit. 5) Loan provision procedure - First contact (reception) is always made by telephone. A meeting is arranged with a loan officer in one of Adie’s offices or “stand-by” points (so- called “permances” in which Adie staff is only present one afternoon per week for instance). Proximity is a key concept. - Appraisal: 1h meeting - The capability of paying back is assessed by looking at the personal bank account over the last three months + personal interview (intended to analyse risk). The loan advisor fills in an internal file which is confidential. - The final decision is taken by a selection committee that meets once a week. The loan officer may refuse a project, but only the selection committee has the power to approve a project. - The committee treats 3-15 projects each week. - In general 4-5 days pass between reception and appraisal. The final decision may take up to 1 month. - Adie has considerably speeded up its number of loans and the credit provision procedure. 5 years ago, each loan officer provided 20 loans per year. Today: 70-100 loans per LO per year. Seven year ago, only one selection committee took place per month; today: one per week; however Adie can still do better; in order to become sustainable it is estimated that Adie has to provide 12,000 nouveaux credits with a write-off rate lower than 3% (today write-off rate is around 3%). - One of the participants highlighted that Adie’s procedure is low in comparison to the working method in Bulgaria where it only takes 2h to provide a loan. The whole process is managed through the computer. On an

3 average 155 loans are provided per year per loan officer. Interest is at 18%. 6) Social impact measurement Adie has carried out a study on social impact and has a system for social impact measurement. This is intended to make sure that Adie remains close to its target group and mission. 7) Risk management To manage risk, Adie uses 50% guarantee from a family member/ a friend (who has to be able to assume the monthly instalments; this is in order to give the candidate the feeling of responsibility). The other 50% are provided by the FGIE guarantee which Adie pays for. The client does not pay for FGIE (national guarantee fund). 8) Loan recovery Reasons of non-repayment: - Types of activities; - Personal motivation; - Forgot to put money on account; The monthly instalments are automatically debited every 10th of each month. In case of failed repayment, the loan officer immediately calls the client. The guarantee is taken on immediately. 9) Loan officer evaluation - Objectives are qualitative (portfolio developments, partnering, fieldtrip) and quantitative (number of loans) - Number of loans depends on the experience of the loan officer, the knowledge of the sector, the number of selection committees - There is no system of gratification, but redistribution depending on the regions 10) How to have good records? - Adie proposes training to its new employees: three weeks over 18 months (provided by employees or cabinets); additionally, all employees can take part in three trainings each year; - Adie has partnerships with banks – loan officers are in direct contact with the bank officers;

4 - Good judgments and risk management (know the client; does the client have bank problems? what is his/her behaviour regarding money? Change contact person; work together with bank officer and social worker);

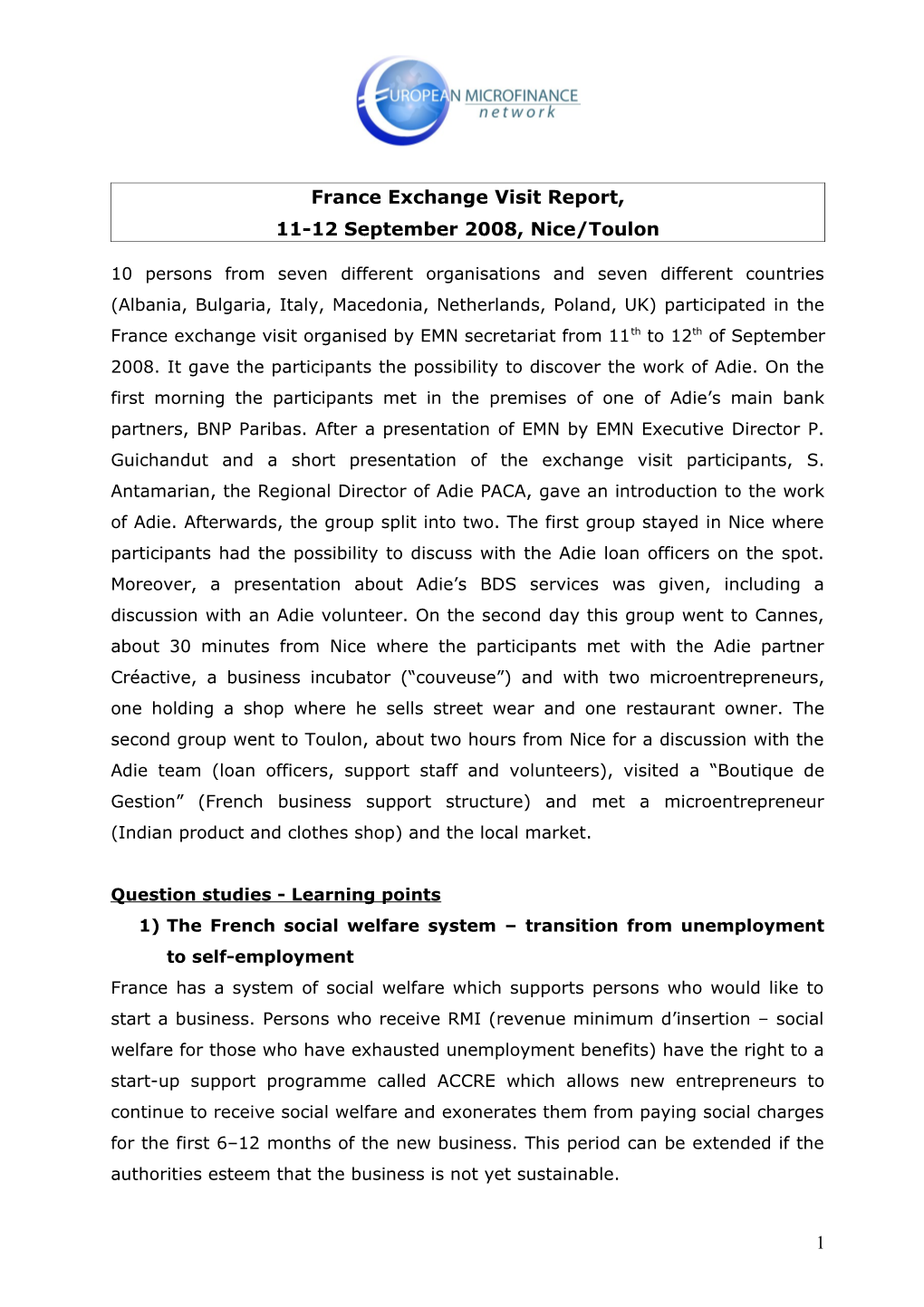

11) BDS services Adie has very well developed BDS services. Adie provides pre- and post-business support. Volunteers assure the greatest part of Adie’s BDS services. Pre-business start-up support: - « Bien Démarrer » (get off to a good start) (group sessions) - Service 3W (group session of 2h) - How to win (save) time? How to win customers? How to win money?) Specific public financing: Accompagnement Amont RMI (specific programme for people who benefits from RMI)

Credit BDS

Reception

Appraisal individual group

Upstream “Get off to a guidance good start” (Bien démarrer) Credit Committee after approval Follow-up group individual individual win Adie A la contact carte

Moreover, Adie works in partnership with business support structures such as the “Boutiques de Gestion” or business incubators (“couveuses”) which give the new entrepreneur the possibility to start his/her business without taking too much risk. As such the couveuse Créactive in Nice can take the legal responsibility for a business, so that the entrepreneur can concentrate 100% on the business start.

5 Post-bussines start-up support: - Adie Contact (business diagnosis by telephone every three months; free of charge and addresses all entrepreneurs who obtained a microloan from Adie) - Adie Conseil (“hotline” - business support by telephone; open to all Adie clients; can be followed by a personal interview) - Stand-by points (“permanences”) - Specialised training courses in partnership with big enterprises and/or provided by volunteers) – f.ex. Computing training courses

Specific projects: - Créajeunes for young entrepreneurs in disadvantaged neighbourhoods - SAP (Service Accompagnement de Projet)

12) Islamic Finance Several years ago, Adie created a specific finical product for the Muslim population (called “prêt de liberté” – freedom loan), for which it transformed the interest into fees. There seems to be no need for this product in France as there was very low take-up of this product. The Muslim population (mainly from North and sub-Saharan Africa) is reached without a specific tool. In the UK Street Cred had to give up its special loan product addressing Somali women due to a change in legislation (need to show interest as such). Somali women cannot be reached without an adapted product. Financial leasing would be a possibility, but is only possible for bigger organisations.

6 Evaluation

Of the 10 participants, five filled in the evaluation form (out of which three practitioners and one academic). Participants could indicate their level of satisfaction on a scale from 1 (definitely not satisfied) to 5 (definitely satisfied).

Participants were less satisfied with the organisational efficiency during the visit and the materials disseminated. They were most satisfied with the booking process and with translation.

Please indicate the level of satisfaction with the following organisational aspects of the exchange visit:

Answer Options Rating Average 1. Pre-exchange organisational efficiency, i.e. provision of 3 information, visa support, hotels etc. 2. Guide for the exchange visit 3,8 3. Booking and payment process 4,4 4. Translation 4,6 5. Organisational efficiency during the visit 2,8 6. Price, value for money spent 2,6 7. Time alloted for networking 3,4 8. Opportunity to learn more about microfinance 3,4 9. Opportunity to exchange experiences, practices 3,6 10. Opportunity to promote your institution 3,8 11. Materials disseminated during the exchange visit 2,6 12. Relevance of issues and subjects covered by the visit 3,4 The activities on Thursday afternoon were rated below average. It can be suggested that the trip by car was too long (group 2) and did not leave enough time for discussion on Thursday afternoon. The general presentation of Adie was rated high.

Now we would like to know how you evaluate the presentation of EMN/Adie and the visits to host organisations:

Rating Average 1. Presentation of host organisations 4 2. Presentation if microcredit in France 3,4 3. Presentation of EMN 3,8 4. Host organisation's visit (overall rating) 3 - Activities on Thursday afternoon 2,5 - Activities on Friday morning 3,5 - Activities on Friday afternoon 2,75 - Visit to microentrepreneurs 3,25 - Visit to partners 3,75 5. Debriefing and conclusions 3,2

7 The most relevant activities for the participants were:

- The presentation of Adie (mission, business development support, programmes);

- Practical operations and procedures ;

- The conditions to obtain a microcredit;

- The involvement of volunteers;

- Exchange of experience between the participants/networking;

- Client visits (how client assess the support they received from Adie);

Other relevant topics that should have been covered during the exchange visit:

- More time on business analysis and risk management;

- The near future;

- Case studies, real examples of how the process works;

Three out of five persons would definitely recommend taking part in an EMN exchange visit.

Would you recommend to others involved in microfinance that they participate in an EMN exchange visit?

1 - definitely not 0 2 - probably not 0 3 - don't know 1 4 - probably yes 1 5 - definitely yes 3 Three persons stated that they would take part in another exchange visit organised by EMN; two would rather not like to take part again.

Would you be interested in participating in the next EMN exchange visit in 2009? Response Answer Options Count 1 - definitely not 1 2 - probably not 1 3 - don't know 0 4 - probably yes 2 5 - definitely yes 1

8 Suggestions for future exchange visits organised by EMN are:

- More insight in the technical aspects;

- Shorter days, shorter travel time, no overrunning of the schedule, better logistics organisation;

- Smaller groups (not more than 4 people);

- Better organisation of topics covered (so they are not repeated);

- Less theory, more practical examples;

- Case studies of entrepreneurs (including negative examples);

- Background information on the clients visited;

While some participants stated that the visit should have been longer, others stressed that one day would have been enough. Additionally, one person thought that it would be better not to organise an exchange visit in conjunction with the Annual Conference in order to benefit more from the unique possibility to get to know best practice.

9