TB4369 GS/CB /10-12-1999

Country Report Poland

Road Transport Charges

Final

On behalf of: Phare Multi-Country Transport Programme

NEI Transport, December 1999 CB/TB4369r24 Table of contents

Pages

Summary i

1 Background 1

2 Database 2 2.1 Road networks 2 2.2 Traffic 2 2.3 Vehicle Fleets 3 2.4 Fuel Consumption and Data Consistency 3

3 Actual and planned RTC systems 4 3.1 Fuel Taxation 4 3.2 Vehicle Taxation 4 3.3 Other taxation 5

4 Revenues 7

5 Allocation mechanism 8

6 Expenditures and infrastructure cost 9

7 Cost recovery ratios 10

8 EU compliance 11

9 Conclusions and Recommendations 12

CB/TB4369r24 i

Summary

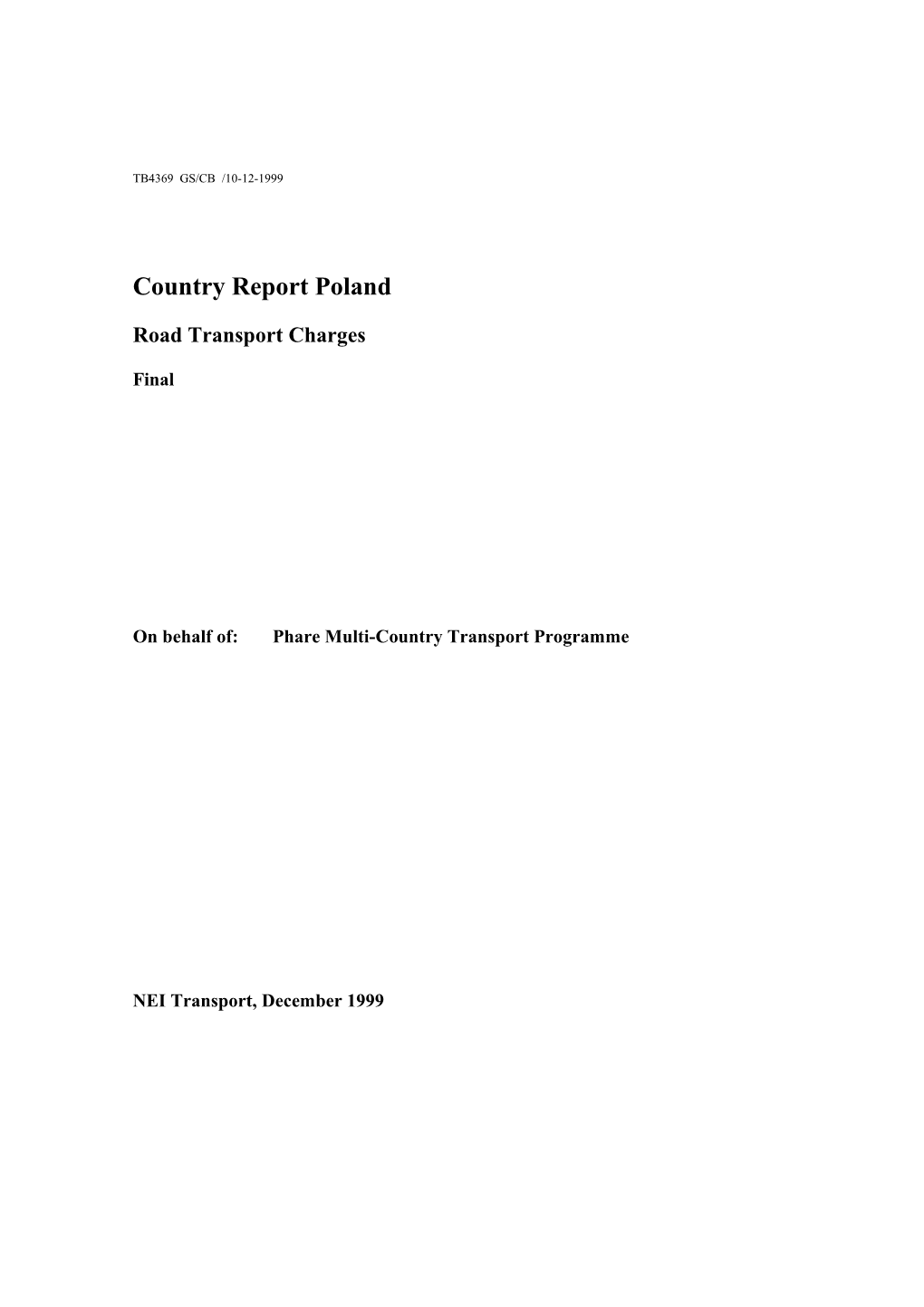

Country characteristics Road fiscal policy Cost recovery Main policy objective is the harmonisation 4500 of Polish fiscal policy on roads with EU 4000 regulations 3500 3000 Revenues from fuel taxation are partly 2500 other earmarked for building, modernisation and 2000 fuel 1500 protection of roads invest ment 1000 There is a road user charge for domestic and 500 overhead foreign entrepreneurs carrying out 0 m aintenance international road transport revenues costs Ratio Actual/Normative maintenance: 39%

Institutional and legal setting Transport Means Tax is a local vehicle tax, partly based on the Act on Financing Public Roads. This tax does not cover private cars Revenues from the Transport Means Tax are flowing to the county budgets, from which construction, maintenance and management of county roads have to be paid. System of fuel taxation is laid down in Act of 08.01.93 (O.J.11,50) Revenues of the latter are earmarked for the infrastructure fund There is a fund under the General Directorate of Public Roads This fund is part of the general budget, but the funds are earmarked The means of this fund are coming from road charges, concessions and permits and the use of roads in international traffic

EU Comparison Excise tax on fuel (Heavy) vehicle taxation

Fuel Tax Vehicle Tax

0,4 800

0,3 600 r r e a t i e l y /

0,2 / o 400 o r r u u E E

0,1 200

0 0 Poland EU Poland EU Petrol Unleaded Petrol Leaded Diesel Rigid light trucks * Rigid medium trucks * Rigid heavy trucks * Articulated trucks *

Direction of move The fuel excise duties are currently under EU-minimum levels, but are approaching EU minima as determined in the relevant Directive The vehicle taxation is exceeding the EU minima and is among the highest in the Phare region.

CB/TB4369r24 ii

Conclusions and Recommendations Poland is approaching the EU Minima set for fuel taxation and is already exceeding the EU minima set for annual vehicle tax for heavy vehicles. A vast share of revenues from fuel taxation is transferred to the road sector. It has now come to a point where it should decide on whether to introduce a tolling or a road user charges system in order to respect the user pays and the territoriality principle.

It is recommended to: increase the rates of the fuel taxation gradually towards EU minimum levels restructure the vehicle tax system: tax to be based upon number of axles, maximum permissible gross loading weight and type of suspension and introduce the principle of minimum levels given growing traffic figures and the transit character of Poland the introduction of a tolling or road user charges system is recommended. A user charging system similar to the Euro Vignette could be considered. At the same time a tolling systems (in close combination with a concession system for new motorways) is an option consider the option to involve the private sector in road maintenance activities, possibly through concessions.

CB/TB4369r24 1

1 Background

The most important goal of the Polish fiscal policy regarding road transport is the harmonisation and adjustment to the European Union regulations. The adjustment process is proceeding which is expressed, amongst others, in the introduction of the possibilities of concessions for international transport, the adjustment of the fuel excise level and the launch of a road charges system on the basis of the Euro- vignette.

At the moment, there are no tolls being in force in Poland, but only some road charges. However, there is the possibility to introduce charges for passing through motorways and express carriageways after completion of their construction (in compliance with the Decree of Minister of Transport and Maritime Economy). The following principles have been adopted for tolling: May not include secondary roads By-pass must be available Public transport has to serve the destination

Furthermore Poland is considering the possibilities of a congestion charge and some tax exemptions for the support of combined transport.

The Transport Means Tax is touched upon by the Act on financing public roads. This charge may be considered as local vehicle taxation. This tax is established within a general framework that is laid down on a national level, fixing maximum taxation levels. The amended Act of 8 January 1993 (O.J. No. 11,item 50) covers the excise fuel taxation. Since 1 January 1998 the Decree of Minister of Transport and Maritime Economy (of 3 December 1997 together with the amendment of 31 March 1998) is in force on charges on international road transport for passing national roads and units entitled to collect them. This Decree is based on the Act of 2 August 1997 on conditions of international road transport practice (O.J. No. 106, item 677).

The main regulation on infrastructure funds is Art. 30 of the act of 2 August 1997 „On Conditions of International Road Transport Practice” (O.J. No. 106., item, 677). This article proclaims that revenues obtained from road charges and from charges for concessions and from permits granted are transferred to a separate account of the General Directorate of Public Roads with a designation for the building and maintenance of national roads. The means of this fund are only received from granted foreign concessions and permissions and the use of roads in international traffic. Establishment of this account was possible after affirming the act of 2 August 1997 about international transport.

CB/TB4369r24 2

2 Database

2.1 Road networks

Poland has a rather extensive public road network, totalling over 360,000 kms. As per 1-1-1999 the public road sector has been reorganised, limiting the extent of the national road network from over 45,000 kms to 18,100 kms and redefining the networks under other authorities; particulars are shown in table 2.1

Table 2.1 Road Networks

Road type Network length (km) Share paved (%)

Motorways 264 100 Express roads 241 100 Other national roads 17,595 100

Subtotal National 18,100 100

Voivodeship (provincial) roads 29,600 100 Powiat (district) roads 126,600 87 Gmina (communal) roads 190,000 45

Grand total 364,300

The general condition of the national roads leaves much to be desired; only some 20% is good to fair, about 40% is unsatisfactory, while 40% is in a poor state of repair.

2.2 Traffic

The last extensive traffic counts have taken place in 1995, from which average volumes and composition on the national road network have been derived. After applying growth factors, estimates for 1998 have been prepared, which are presented in table 2.2. Included are Contractors estimates of Average Annual Daily Traffic (AADT) on Voivodeship and District roads.

Table 2.2 AADT and Composition on Road Networks (1998)

Network Pass. Buses Light Medium Heavy Art. Total cars trucks trucks trucks trucks Motorways 7,200 180 450 360 270 540 9,000 Express roads 4,000 100 250 200 150 300 5,000 Other nat. and 2,480 62 155 124 93 186 3,100 Voivodship District 600 15 41 36 22 36 750 Communal 40 1 3 2 1 2 50

CB/TB4369r24 3

2.3 Vehicle Fleets

Information on the vehicle fleets is only available at a rather aggregated level, as follows: Passenger cars and utilities 7,782,500 Buses 85,100 All trucks 1,088,870

Partly based on the traffic composition, the truck fleet has been subdivided into light, medium, heavy and articulated trucks, applying the following shares (%): 40 - 30 - 15 - 15

2.4 Fuel Consumption and Data Consistency

Based on the vehicle fleets and estimates of typical annual vehicle-km productions and typical fuel consumption rates, total fuel consumption in the road sector can be derived. Another approach is based on the AADT levels in combination with fuel consumption rates, complemented with estimates for urban traffic. Outcomes can subsequently be compared with direct information on fuel use through import and production data.

All data sources contain errors, but the AADT approach can be considered as the most accurate; indeed, results show a good consistency with direct information. The adopted total consumption is as follows (in million litres): leaded gasoline 1,500 unleaded gasoline 6,264 diesel 7,066

From the vehicle fleet and AADT estimates, the annual production of vehicle-km per vehicle type can be deduced. For passenger cars this would average 12,300 km and for buses 33,000 km, which appear in good ranges. Only for trucks the figure of 12,200 km seems quite low, possibly owing to an overestimate of the operational fleet.

CB/TB4369r24 4

3 Actual and planned RTC systems

3.1 Fuel Taxation

The excise fuel tax is covered by the Act of 8 January 1993 (O.J. No. 11,item 50) with later changes and amendments to the act. This Act introduces excise liquid fuel tax and sets the rates at the level of: 80 % in relation to producers’ sale price and 400 % - to importers’ sale price in proportion to customs value raised by customs duty

The excise for engine fuel is determined by the Decree of Minister of Finance of 5 January 1998 (O.J. No. 2, item 3). Charge levels for excises, customs duties and other fuel taxation were established at the levels, indicated in table 3.1:

Table 3.1 Level of fuel excise duties

Product Level per ton in Euro 94-octane petrol (leaded) 293 Unleaded patrol 257 Diesel 167

The revenues from fuel excise transferred to the state budget amount to Euro 1645 million annually. The Act on financing public roads introduced the notion that they are designated within the budget act for building, modernisation and protection of roads. The level of this designated budget may not be less than 30 % of revenues planned in a particular year.

3.2 Vehicle Taxation

The Transport Means Tax may be considered to be vehicle taxation. This tax is touched upon in the Act on financing public roads of 29 August 1997 (O.J. No.123, item 780) which introduced amendments to the act of 12 January 1991 „On Local Taxes and Charges” (O.J. No. 9, item 31 with later amendments).

Based on art. 8 of the Act on financing public roads, the following categories are subject to transport means tax: Motor trucks with load capacity from 2 ton to 12 ton, Motor trucks over 12 ton, Truck-tractors and semi-trailers with load capacity over 5 ton, Trailers and semi-trailers with load capacity over 5 ton, Buses.

The responsible tax body for Transport Means Tax affairs is a county body or a city body that in this way has resources at its disposal. The transport means

CB/TB4369r24 5 taxation fees depend on the kind and size of the vehicles. Motor trucks and buses are subject to transport means taxation: motor trucks depending on load capacity, buses depending on number of seats. The yearly rate level of the transport means tax is fixed by means of a county council or a city council resolution (based on art. 10 of the Act on local taxes and charges). The Minister of Finance introduces maximum levels for the transport means taxes by means of decrees (based on art. 20 par. 2 of the Act on local taxes and charges). The annual tax rate for a vehicle may not exceed the maximum rates.

Table 3.2 Maximum rates Transport Means Tax

Categories Maximum rate in Euro Motor truck with load capacity over 12 ton 435 Truck-tractor and ballast tractor 435 Motor truck with load capacity from 2 to 12 ton 336 (semi-)trailer with load capacity over 5 ton 336 Bus 336 Source: Decree of the Minister of Finance of 20 November 1997

A policy goal is to differentiate the level of the tax rate depending on the type and size of the vehicle, in proportion to the road wear degree. Private cars are not covered by the Transport Means Tax. Somehow these users of the infrastructure are supposed to contribute through paying excise duties.

The revenues of county budgets from transport means taxes amounted to Euro 283,4 million in 1997. Tasks in the area of financing buildings, modernisation, maintenance and protection of county roads, as well as managing them are financed by county budgets.

3.3 Other taxation

Important legislation concerning user charges is the Decree of Minister of Transport and Maritime Economy of 3 December 1997 (O.J. No. 148, item 992), based on the Act of 2 August 1997 „On Conditions of International Road Transport Practice” (O.J. No. 106, item 677). The Act on public roads and amendments to some acts of 28 April 1993 art. 13 (O.J. No. 47, item 212) regulate that the use of public roads in cases specified in par. 2 might depend on payment of road charges.

In accordance the RTC legislation in Poland, the road carrier is obliged to pay the following charges: for international transport concessions for foreign permits on international road transport for passing national roads for ferry passages on public roads on vehicles exceeding permissible standards for passing the Polish public roads

CB/TB4369r24 6

Stamp duties (for transportation documents) related to air pollution

Domestic and foreign entrepreneurs carrying out international road transport (for hire and reward and for own account) pay a fee related to the time of passing, and to the type and permissible total weight of the vehicle. It is possible to choose either annually, half-yearly, monthly, weekly or daily versions. The resources are transferred to a separate fund of the General Directorate of Public Roads with the intention to build and maintain national roads.

Foreign vehicles must be charged with road usage fees. A foreign entrepreneur carrying out international road transport pays a fee related to the time of the passage, and the type and total weight of the vehicle. He pays this charge at the customs office at the border. Thus road charges are obligatory for both domestic and foreign carriers. The latter pays regardless of the nationality, origin, and destination of the vehicle.

The levels of road charges are specified in the Decree of Minister of Transport and Maritime Economy mentioning charges for passing national roads used for international road transport and it defines the units appointed to collect them. The level of these fees in 1998 is indicated in table. The rate depends on the permissible total weight of the vehicle and has been decreased gradually towards EU levels.

Table 3.3 Minimum and maximum level of road user charge in Euro

Vehicle Minimum level per day Maximum level per year Bus 3,35 314 Truck 4,52 1255

The revenues resulting of road charges transferred to the account of the general Directorate of Public Roads amounted to Euro 68 million in 1997 (including charges by way of issue concessions, permits and road charges).

Road users also pay ecological charges in respect of exhaust fumes emission. The Decree of Ministers’ Council of 30 December 1997 (O.J. No. 162, item 1117) is in force, which obliges to pay charges for emission of pollutants to the air. Appendix No. 4 of the Ministers’ Council Decree contains a list of unit charge rates for emission of pollutants into the air produced during fuel burning in combustion engines.

CB/TB4369r24 7

4 Revenues

Revenues are largely raised through the fuel excise duties, of which 42% are earmarked to the road sector, as laid down in the Act of August 1997 with its subsequent modifications. Funds are supplemented by the International Road Transport Fee (IRT), by direct support from local governmental budgets and IFI funding.

Excise taxes amount PLN 0.94 per litre leaded gasoline, PLN 0.87 for unleaded gasoline and PLN 0.63 for diesel. Of the total amount, expected to be about PLN 11,000 mln. in 1999, 42% or PLN 4,620 mln. are channelled to the various road networks, applying specific distribution keys (see Chapter 10).

For the national road network total funds for 1999 amount to PLN 2,977 mln., broken down as follows (million PLN):

Table 4.1 Breakdown of Road Fund

Amount (mio PLN) Budget 1,366 IRT 180 World Bank 353 Phare 326 EIB 576 Other 176 Total 2,977

CB/TB4369r24 8

5 Allocation mechanism

Of the total amount from fuel excise taxes, 42% is earmarked to roads; this is further divided in 31.5% (at least not less than 30%) for national, provincial and district roads and 10.5% for the communal roads. Of the allocation to non- communal roads, 60% (or 18.9% of the total) is devoted to provincial and district roads and to those national, provincial and district roads, which are within towns with a district status. The remaining 40% (or 12.6% of the total) is for the national roads under the General Directorate for Public Roads (GDDP). Table 5.1 summarises the allocations of the earmarked fuel taxation to the various road networks.

Table 5.1 Distribution of the Budget from Fuel Excise Taxes – 1999

Road Network Length (km) Share (%) Expected Amount (MPLN) National 16,800 12.6 1,385 Provincial 28,700 6.0 663 District 121,700 7.4 808 Nat., Prov., Distr. 7,100 3.5 391 Roads in Towns Investment Prov., 2.0 216 Distr. Roads and Maint. Of Ferry Crossings Subtotal 31.5 3,462 Communal Roads 186,000 10.5 1,153

For the national roads, the budget is supplemented with the revenues from the IRT (MPLN 180) and grants and loans from International Financing Institutions (MPLN 1,431).

CB/TB4369r24 9

6 Expenditures and infrastructure cost

Expenditures The total budget for the national road network in 1999 amounts to MPLN 2,977 and is distributed over Management and Maintenance (MPLN 749 or 25%), Modernisation (MPLN 1,638 or 55%) and New Construction (MPLN 591 or 20%). A proper distinction between routine and periodic maintenance and rehabilitation/modernisation is not possible. Modernisation includes periodic maintenance and rehabilitation as well as strengthening and truly modernisation.

Normative Maintenance Normative maintenance consists of routine and periodic maintenance, assuming an otherwise satisfactory condition of the road network. This is presently not the case in Poland, where 80% of the network length is considered to be in unsatisfactory to bad conditions. As a consequence, actual maintenance requirements are (substantially) higher than indicated by normative standards.

Contractor has estimated normative maintenance costs, based on previous studies in the Region, differentiating for traffic volumes and distinguishing routine/periodic and fixed/variable costs. When applying an overall average AADT for the 18,100 km national roads, indicative, normative totals would amount to: routine maintenance EURO 2,125 per km or MEURO 38.5 (MPLN 151) periodic maintenance EURO 5,625 per km or MEURO 102 (MPLN 401)

It seems that for the National Road Network (749 MPLN) actual expenditures on maintenance, are exceeding the calculated normative maintenance costs (552 MPLN). Nevertheless total maintenance expenditures are far below total normative maintenance costs. (see table 7.1).

New Construction Investments in new road infrastructure are limited to the construction of two bypasses (Poznan and Katowice). Furthermore, in the near future by passes in Gdansk and Krakow and A4 motorway sections are planned under ISPA financing. Plans to construct an extensive system of motorways under concessions have been downgraded; instead, capacity extensions will be limited to specific situations where congestion warrants action.

CB/TB4369r24 10

7 Cost recovery ratios

The RTC Analytical Tool calculates a number of cost recovery ratios (CRRs). In figure 7.1 a graphical overview is presented of revenues (excise tax on fuel and annual vehicle tax) and expenditures, broken down in (normative) maintenance, overhead and capital investments (rehabilitation and reconstruction).

Figure 7.1 Revenues and expenditures (million Euro)

4500 4000 3500 3000 2500 other 2000 fuel 1500 investment 1000 500 overhead 0 maintenance revenues costs

In table 7.1 an overview is presented of a number of CRRs in Poland. A figure of 100 percent stands for equal revenues and costs. Figures below 100 demonstrate shortages of funds, while values above 100 reveal a surplus.

Table 7.1 CRRs in Poland

Cost Recovery Ratio (%)

TOTAL Tool Revenues over Normative MAINTENANCE Costs 439% TOTAL Tool Revenues over Normative TOTAL Costs 177% Actual TOTAL Expenditures over Normative TOTAL Costs 28% Actual MAINTENANCE Expenditures over Normative MAINTENANCE Costs 39%

CB/TB4369r24 11

8 EU compliance

The Polish fuel excise duty system is comprised by a set of fixed charges (293/257 and 167 Euro for leaded/unleaded petrol and diesel). This system is in contradiction with the EU system which is operating minimum rates (337/287 and 245 for the three mentioned categories).

The vehicle tax is a weight-based (loading capacity) tax (although with very few categories) with maximum rates (435 Euro for a truck with load capacity exceeding 12 tonnes). Examples of taxation rates (minimum and maximum): Tax rates for transport means for a bus in 1998 are within the limits of Euro 45 - 182 depending on the number of seats in the bus; Tax rates for a motor truck and a truck-tractor in 1998 are within the limits of Euro 232 - 434 depending on the load capacity of the motor truck or the pressure on fifth wheel coupling of the truck-tractor; Tax rate for a trailer or a semi-trailer shaped within the limits of Euro 145 – 290; Tax rate for a truck-tractor is Euro 434.

The structure of this system and the tax base is not in accordance with the EU system which is based minima and on the number of axles, the maximum permissible gross loading weight (up to 44 tonnes) and the type of suspension of the vehicle or vehicle combination. The maximum rates of the vehicle tax are below the EU minimum rates. On top of that the taxation system is not quite transparent since the definitive tax level is established locally.

In figure 8.1 an overview is presented of the levels for fuel and annual vehicle tax in Poland in relation to the EU minima.

Figure 8.1 Fuel and annual vehicle tax in Poland in relation to EU minima (per 1/1/1998)

Fuel Tax Ve hicle Tax

0,4 800

0,3 600 r r e a t i e l y / 0,2 / o 400 o r r u u E E

0,1 200

0 0 Poland EU Poland EU Petrol Unleaded Petrol Leaded Diesel Rigid light trucks * Rigid medium trucks * Rigid heavy trucks * Articulated trucks *

CB/TB4369r24 12

9 Conclusions and Recommendations

It should be noted that the most important goals of the Polish policy regarding road transport is the harmonisation and adjustment to the EU regulations, which includes adjustment of fuel excise levels and a road user charging system similar to the Euro Vignette model.

Poland has thus adopted basic EU principles in the field of RTC. At the same time it should be noted that Poland has established a certain degree of earmarking through a Road Fund designed for financing the building of national roads.

It is recommended that the rates of the fuel taxation will be increased - in order to reflect the EU legislation – giving the diesel rates most of the attention taking into account its impact in the commercial sector.

Also it is recommended that Poland restructure the vehicle tax system, using the number of axles, the maximum permissible gross loading weight and the type of suspension as a base. Also the principle of minimum rates should be introduced. This may be done along with a sole adjustment of the maximum rates. The usage of maximum rates in a decentralised system may be continued. It should be noted that local governments need to be compensated if the revenues from the Transport Means Tax decreases.

It should be acknowledged that Poland is in a process of implementing a road user charging system similar to the EU Vignette system. The Polish system – under development – is intended to be non-discriminatory to Polish and foreign vehicles. So far the charging system is confined to national roads used for international traffic.

It is recommended that the process of implementing a user charging system similar to the Euro Vignette system will be continued, taking into account the latest regulation as reflected in Directive 99/62 (based on motorways/other high classed roads, maximum rates, differentiation in Euro I and II). Especially the current application of ecological charges could be replaced by the EURO I and II classification, resulting in an improved enforcement.

Accordingly, a principle decision should be made whether to have user charges or tolls on motorway sections, as it is not in accordance with the EU legislation to apply both on the same section of the road. The question is whether tolling is suitable and feasible in Poland.

CB/TB4369r24