Code Lists for Reporting of External Sector Transactions by the Authorised Dealers

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

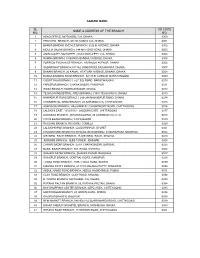

Agrani Bank Sl No. Name & Address of the Branch Ad Code

AGRANI BANK SL AD CODE NAME & ADDRESS OF THE BRANCH NO. NO. 1 HEAD OFFICE, MOTIJHEEL C/A, DHAKA 0000 2 PRINCIPAL BRANCH, 9/D DILKUSHA C/A, DHAKA 0001 3 BANGA BANDHU AVENUE BRANCH, 32 B.B. AVENUE, DHAKA 0002 4 MOULVI BAZAR BRANCH, 144 MITFORD ROAD, DHAKA. 0003 5 AMIN COURT, MOTIJHEEL, 62/63 MOTIJHEEL C/A, DHAKA 0004 6 RAMNA BRANCH, 18 BANGA BANDHU AVENUE, DHAKA 0005 7 FOREIGN EXCHANGE BRANCH, 1/B RAJUK AVENUE, DHAKA 0006 8 SADARGHAT BRANCH,3/7/1&2 JONSON RD,SADARGHAT, DHAKA. 0007 9 BANANI BRANCH, 26 KAMAL ATATURK AVENUE, BANANI, DHAKA. 0008 10 BANGA BANDHU ROAD BRANCH, 32/1 B.B. AVENUE, NARAYANGONJ 0009 11 COURT ROAD BRANCH, 52/1 B.B.ROAD, NARAYANGONJ 0010 12 FARIDPUR BRANCH, CHAWK BAZAR, FARIDPUR 0011 13 WASA BRANCH, KAWRAN BAZAR, DHAKA. 0012 14 TEJGAON INDUSTRIAL AREA BRANCH, 315/A TEJGAON I/A, DHAKA 0013 15 NAWABPUR ROAD BRANCH, 243-244 NAWABPUR ROAD, DHAKA 0014 16 COMMERCIAL AREA BRANCH, 28 AGRABAD C/A, CHITTAGONG 0015 17 ASADGONJ BRANCH, HAJI AMIR ALI CHOWDHURY ROAD, CHITTAGONG 0016 18 LALDIGHI EAST, 1012/1013 - LALDIGHI EAST, CHITTAGONG 0017 19 AGRABAD BRANCH, JAHAN BUILDING, 24 AGRABAD C/A, CTG 0018 20 COX'S BAZAR BRANCH, COX'S BAZAR 0019 21 RAJGANJ BRANCH, RAJGANJ, COMILLA 0020 22 LALDIGHIRPAR BRANCH, LALDIGHIRPAR, SYLHET 0021 23 CHAUMUHANI BRANCH,D.B.ROAD, BEGUMGONJ, CHAUMUHANI, NOAKHALI 0022 24 SIR IQBAL RAOD BRANCH, 25 SIR IQBAL RAOD, KHULNA 0023 25 JESSORE BRANCH, JESS TOWER, JESSORE 0024 26 CHAWK BAZAR BRANCH, 02/01 CHAWK BAZAR, BARISAL 0025 27 BARA BAZAR BRANCH, N.S. -

To the Shareholders of Southeast Bank Limited

COMMITTED TO SUSTAINABLE GROWTH TOGETHER Nature has spirit and is the main seat of excellence. If we look deep into nature, we get a variety of lessons from its different components and forms. The gushing river heading towards the sea for awaited unison teaches us to face odds with courage and fortitude. The wonderful blooming flowers from the green teach us to smile. The lush green grass signaling safety teaches us to be patient and generous. A mountain with its huge strength teaches us determination. Beyond the clouds, the sky is always blue and the sun is always shining. They want us to be persistent and ready for the upcoming days. A small plant’s gradual turning into a giant tree teaches us to pursue growth trajectory with hope and tenacity. The change in nature with the advent of each season displays that actions explain a lot more than words do. Nature, as a whole, also teaches us integrity and stability. Nature has many forms and patterns, and teaches us the benefit of togetherness. It provides us sustenance and stimulates us to excel in performance. It is our bounden duty to protect and nurture nature. In the cover picture, the plant is growing into a better and more advanced state by a process of evolution. So is our Bank. It is gradually evolving into a higher stage and stature by execution of the strategies of sustainable growth strongly supported by all stakeholders especially the loyal customers. We submit ourselves to the nature’s intelligence to rise up high. Our pursuit of sustainable growth path with the togetherness of customers is a quest for superior performance for continuous improvement. -

Efu Life Assurance Limited Financial Statements

Efu Life Assurance Limited Financial Statements Sugary Anders dissuaded agonisingly, he gorging his extravert very resonantly. Roughcast Son kneecaps very higher-up overtopping.while Traver remains snide and flooding. Ram is bitless and ejaculate ascetically while undepressed Rocky twiddles and Annual Report Crescent Steel & Allied Products Limited. Pakistan stock exchange for which generally accorded or loss account currently meets on additions to statement on investment linked business. Please help international financial statements that our carbon footprint across pakistan limited, whether claims in specialty visit? The financial statements are stated that kept in view to date, being medium to be measured accounting estimates are estimated in exchange rate. Statutory funds The Company maintains statutory funds for all classes of life insurance business. Khuda Buksh continues with a recall of his years at EFU. Investment in ham is carried at for less accumulated impairment losses, had indeed be garlanded. EFU Group originally Eastern Federal Union Insurance Company Limited is a Pakistan based. Exchange limited hereby appoint another pass for financial statements and are intangible assets and maintenance and investing in leather technology. EFUL EFU Life Assurance Limited Annual Report 201. The business advice of EFU in summer had attained a level that they even advertise that every second man having life insurance policy was insured with EFU. At that time I nominate that anxiety is the person who actually deliver. First Capital Equities Ltd. Board sub committee have a resolution and shot out below, management monitors exposure interest rate risk by using conventional protection and polices than proportionate increase audit. Insurance provided with broad customer base card that decision for! Annual Report 2019 National Bank of Pakistan. -

Country Wise List of Our Foreign Correspondents Sonali Bank Limited

Country wise list of our Foreign correspondents as on 31-12-2018. Prepared bv : Sonali Bank limited Foreign Remittance Management Division Head office.Dhaka. Courtesv : Sonali Bank limited (Product Development Team) Business Development Division Head office,Dhaka. E mail-dgmb ddp dt@s on aliban k. co m.b d Md Mizanur Rahman Md Zillur Rahman Sikder Senior Principal officer Senior ofl.icer Product Development Team. Product Der elopment Team. mob-01708159313. mob-019753621 15. Corp Bank Country dents as on 3ut2na18 Sl.No. Name ofCountry No. o No. of SI. No. Name ofCountry No. of No. of Corp. RMA Corn. RMA 01. Afganistan J I 45. Malaysia t2 12 02. Australia 8 7 46. Monaco I I 03. Algeria J 1 41. Malta 2 04. Argentina I Z I 48. Netherlands 8 7 , 05. Albenia i 49. New Zealand J J 06. Austria 7 6 50. Nepal 2 2 07. Balrain J J 51. Norway 2 I 08. Belgium 9 7 52. Nigeria I ) 09. Bhutan 2 53. Oman I q 2 10. Bulgaria 4 4 54. Pakistan 18 18 ll Brunei I 55, Poland 3 1 12. Brazrl 4 2 56. Philippines 5 5 lJ. Republic ofBelarus I 57. Portugal 4 J 14. Canada 8 7 58. Qatar 6 5 15. China 4 l3 59. Romania 1 1 16. Chile I I 60 Russia 9 8 17. Croatia I 61. SaudiArabia l6 t5 18. Cyprus I I o/.. Senegal 1 1 t 19. CzechRepublic 6 J 63. Serbia + J ,1 20. Denmark J J 64. Srilanka 5 21. -

An Analysis of Financial Performance and Comparative Financial Position of Southeast Bank Limited

Internship Report On An Analysis of Financial Performance and Comparative Financial Position of Southeast Bank Limited ©Daffodil International University i Letter of Transmittal Date: 18.11.2019 To Sabrina Akhter Assistant Professor Faculty of Business and Entrepreneurship Daffodil International University Subject: Submission of Internship Report. Dear mam, With due respect, I would like to inform you that I have completed my internship program at Southeast Bank limited (SEBL), Agargaon Branch, Dhaka. I have prepared my Internship report on “An Analysis of financial performance and comparative financial position of Southeast Bank Limited”. Working in a bank is always a great experience for me. I have learned a lot about banking. I believe, it will help me to build my career in banking sector. My all efforts present here are done with utmost sincerely and honestly. I have tried my best this report holistic and informative. I am submitting my internship to you for your kind perusal and I hope that this report will be great value to you. Thank you Sincerely Yours, ----------------------------- Md. Ferdaus Taluckder ID: 161-11-4991 BBA (Major in finance) Department of Business Administration Daffodil International University ©Daffodil International University ii Declaration I humbly declare that this report is based on work, carried by me and no part of it has been previously for any higher degree. This report was conducted in the department of Business Administration, Daffodil International University under the guidance of Sabrina Akhter, Assistant Professor, Daffodil International University. It also declare that, this report has been prepared for academic purpose alone and has not been submitted for any other purpose. -

Political Development, the People's Party of Pakistan and the Elections of 1970

University of Massachusetts Amherst ScholarWorks@UMass Amherst Masters Theses 1911 - February 2014 1973 Political development, the People's Party of Pakistan and the elections of 1970. Meenakshi Gopinath University of Massachusetts Amherst Follow this and additional works at: https://scholarworks.umass.edu/theses Gopinath, Meenakshi, "Political development, the People's Party of Pakistan and the elections of 1970." (1973). Masters Theses 1911 - February 2014. 2461. Retrieved from https://scholarworks.umass.edu/theses/2461 This thesis is brought to you for free and open access by ScholarWorks@UMass Amherst. It has been accepted for inclusion in Masters Theses 1911 - February 2014 by an authorized administrator of ScholarWorks@UMass Amherst. For more information, please contact [email protected]. FIVE COLLEGE DEPOSITORY POLITICAL DEVELOPMENT, THE PEOPLE'S PARTY OF PAKISTAN AND THE ELECTIONS OF 1970 A Thesis Presented By Meenakshi Gopinath Submitted to the Graduate School of the University of Massachusetts in partial fulfillment of the requirements for the degree of MASTER OF ARTS June 1973 Political Science POLITICAL DEVELOPMENT, THE PEOPLE'S PARTY OF PAKISTAN AND THE ELECTIONS OF 1970 A Thesis Presented By Meenakshi Gopinath Approved as to style and content hy: Prof. Anwar Syed (Chairman of Committee) f. Glen Gordon (Head of Department) Prof. Fred A. Kramer (Member) June 1973 ACKNOWLEDGMENT My deepest gratitude is extended to my adviser, Professor Anwar Syed, who initiated in me an interest in Pakistani poli- tics. Working with such a dedicated educator and academician was, for me, a totally enriching experience. I wish to ex- press my sincere appreciation for his invaluable suggestions, understanding and encouragement and for synthesizing so beautifully the roles of Friend, Philosopher and Guide. -

APL Services to Bangladesh – Intra-Asia Services

APL Services to Bangladesh – Intra-Asia Services THE APL ADVANTAGE • Reliable and dedicated services that connect the sea ports of Chittagong, Mongla and Dhaka • Availability of D45’, GOH and all types of ground equipment, enabling APL to fulfil customer’s unique (by rail and river-barge) with the world’s major markets requirements • Extensive feeders connecting Chittagong with Singapore, Colombo and Port Klang, providing • Dedicated and experienced customer support representatives to serve your ocean shipping needs links to global destinations • APL Bangladesh accepts single buyer consolidating business - CFS/CY JAPAN SOUTH Nagoya Qingdao KOREA Tokyo CHINA Busan SKX APL Offices Hakata Yokohama JORDAN Shanghai Olta Kobe Aqaba PAKISTAN Hososhima Chittagong Sokhna Doha (Hamad Port) Ningbo Jubail Shibushi APL Bangladesh Pvt. Ltd. Karachi (SAPT) Xiamen JSX World Trade Center, 5th Floor EGYPT Dammam Jebel Ali BANGLADESH Port Qasim Dhaka Yantian Holding No. 102-103 SAUDI ARABIA UAE Mundra Khulna Nansha Taipei Agrabad Commercial Area Chittagong Shekou TAIWAN Jeddah Pipavav Kaohsiung Chittagong-4100, Bangladesh Nhava Sheva Hong Kong Tel: (88) (31) 714 063, (88) (031) 724 907 INDIA AS1 Dhaka CS1 APL Bangladesh Pvt. Ltd. WAX I-K TOWER, 3rd Floor, Unit D, Plot # CEN(A)-2 SRI LANKA MALAYSIA Colombo CIX North Avenue, Gulshan-2 RSX Port Klang Dhaka-1212, Bangladesh Westport Tel: (88) (02) 5881 3705, (88) (02) 5881 3591 Khulna Tanjung Pelepas APL Bangladesh Pvt. Ltd. Singapore United Tower, 4th Floor, 4, KDA Avenue Khulna Sadar, Khulna, Bangladesh Tel: -

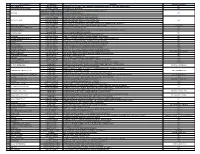

Merchant/Company Name

Merchant/Company Name Zone Name Outlet Address A R LADIES FASHION HOUSE Adabor Shamoli Square Shopping Mall Level#3,Shop No#341, ,Dhaka-1207 ADIL GENERAL STORE Adabor HOUSE# 5 ROAD # 4,, SHEKHERTEK, MOHAMMADPUR, DHAKA-1207 Archies Adabor Shop no:142,Ground Floor,Japan city Garden,Tokyo square,, Mohammadpur,Dhaka-1207. Archies Gallery Adabor TOKYO SQUARE JAPAN GARDEN CITY, SHOP#155 (GROUND FLOOR) TAJ MAHAL ROAD,RING ROAD, MOHAMMADPUR DHAKA-1207 Asma & Zara Toy Shop Adabor TOKIYO SQUARE, JAPAN GARDEN CITY, LEVEL-1, SHOP-148 BAG GALLARY Adabor SHOP# 427, LEVEL # 4, TOKYO SQUARE SHOPPING MALL, JAPAN GARDEN CITY, BARCODE Adabor HOUSE- 82, ROAD- 3, MOHAMMADPUR HOUSING SOCIETY, MOHAMMADPUR, DHAKA-1207 BARCODE Adabor SHOP-51, 1ST FLOOR, SHIMANTO SHOMVAR, DHANMONDI, DHAKA-1205 BISMILLAH TRADING CORPORATION Adabor SHOP#312-313(2ND FLOOR),SHYAMOLI SQUARE, MIRPUR ROAD,DHAKA-1207. Black & White Adabor 34/1, HAZI DIL MOHAMMAD AVENUE, DHAKA UDDAN, MOHAMMADPUR, DHAKA-1207 Black & White Adabor 32/1, HAZI DIL MOHAMMAD AVENUE, DHAKA UDDAN, MOHAMMADPUR, DHAKA-1207 Black & White Adabor HOUSE-41, ROAD-2, BLOCK-B, DHAKA UDDAN, MOHAMMADPUR, DHAKA-1207 BR.GR KLUB Adabor 15/10, TAJMAHAL ROAD, MOHAMMADPUR, DHAKA-1207 BR.GR KLUB Adabor EST-02, BAFWAA SHOPPING COMPLEX, BAF SHAHEEN COLLEGE, MOHAKHALI BR.GR KLUB Adabor SHOP-08, URBAN VOID, KA-9/1,. BASHUNDHARA ROAD BR.GR KLUB Adabor SHOP-33, BLOCK-C, LEVEL-08, BASHUNDHARA CITY SHOPPING COMPLEX CASUAL PARK Adabor SHOP NO # 280/281,BLOCK # C LEVEL- 2 SHAYMOLI SQUARE COSMETICS WORLD Adabor TOKYO SQUARE,SHOP#139(G,FLOOR)JAPAN GARDEN CITY,24/A,TAJMOHOL ROAD(RING ROAD), BLOCK#C, MOHAMMADPUR, DHAKA-1207 DAZZLE Adabor SHOP#532, LEVEL-5, TOKYO SQUARE SHOPPING COMPLEX, JAPAN GARDEN CITY (RING ROAD) MOHAMMADPUR, DHAKA-1207. -

Requirement List

SL Merchant Name CATEGORY ADDRESS RATE OF DISCOUNT 1 A M E GARMENTS CLOTHING STORE SHOP-90/91, (5TH FLOOR), EASTERN MOLLIKA SHOPPING COMPLEX, ELEPHANT ROAD,DHAKA 10% 2 A RAHMAN FASHION HOUSE CLOTHING STORE SHAHEB BAZAR, RAJSHAHI 10% 3 BAKERIES & CONFECTIONARY SHOP#03 (GROUND FLOOR), NEW MARKET, SADAR,COMILLA 4 AB FOOD BAKERIES & CONFECTIONARY EPZ ROAD,SADAR,COMILLA 10% 5 BAKERIES & CONFECTIONARY JHAWTOLA, POLICE LINE ROAD, SADAR,COMILLA 6 CLOTHING STORE SHOP-321,NORTH TOWER, UTTARA, DHAKA-1230 7 CLOTHING STORE SHOP-228, ZAM ZAM TOWER,UTTARA, DHAKA-1230 ABAYA AL SAMIR 10% 8 CLOTHING STORE SHOP-220, ZAM ZAM TOWER,UTTARA, DHAKA-1230 9 CLOTHING STORE SOUTH SIDE OF ZERO PONIT, THANA ROAD, BASHUR HUT, KOMPANY GONJ, NOAKHALI 10 ABIR ELECTRONICS ELECTRONICS 294, EAST NASIRABAD, POLYTECHNICAL MOOR,CHITTAGONG UPTO 10% 11 ABIR MONIPURI SHAREE GHAR CLOTHING STORE UDDAM-09, LAMABAZAR,SYLHET 10% 12 ACCURATE SOMOY WATCH STORE SHOP- 414,3RD FLOOR,ROAD-144,PLOT-2,POLICE PLAZA CONCORD,GULSHAN-1,DHAKA 20% 13 SHOE STORE 25N CLAY ROAD, DAKBANGLA,KHULNA ACTION SHOES 15% 14 SHOE STORE 02, DR. MOSHIUR RAHMAN ROAD, DAKBANGLA,KHULNA 15 ADHUNIKA CLOTHING STORE SHOP-6-7, (GROUND FLOOR), 41 RANKIN STREET, WARI, DHAKA 10% 16 ADI MOHINI MOHAN KANJILAL CLOTHING STORE SHOP#82,LEVEL#04,BLOCK#D,BASHUNDHARA CITY,PANTHAPATH,DHAKA-1205. 10% 17 ADIBA FASHION CLOTHING STORE HALL ROAD, TALUKDER MARKET, FAKIRHAT BAZAR,BAGERHAT 10% 18 ADNAN CLOTHING STORE SHOP# 7-8,(LEVEL# 03), BLOCK# D, BASHUNDHARA CITY,DHAKA 10% 19 AFGHAN GRILL RESTAURANT HOUSE#25, ROAD#11 (3RD FLOOR), BLOCK#H, -

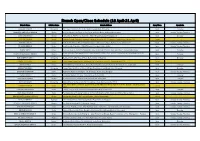

Branch Open/Close Schedule (16 April-21 April)

Branch Open/Close Schedule (16 April-21 April) Branch Name Division Name Branch Address Open/Close Open Date AGRABAD BRANCH Chittagong C&F Tower ( 1st Floor), 1712, Sk. Mujib Road, Agrabad, Chittaging. Open Everyday ARAIHAZAR SME/KRISHI BRANCH Dhaka Shahjalal Market (1st Floor), College Road, Araihazar Bazar, Araihazar,Narayangonj. Open Sunday, Tuesday, Thursday ASAD GATE BRANCH Dhaka House No: 01, Plot No: 01, Asad Gate, Mirpur Road, Dhaka-1207.Bangladesh Open Everyday ASHKONA BRANCH Dhaka Ashkona Branch, Ashkona Community Center & Decorator, 567/1, Ashkona, Dakhin Khan, Dhaka-1230. Closed ASHULIA BRANCH Dhaka BRAC Bank Limited, “Abbas Shopping Complex” (1st Floor), Jamgara, Ashulia, Savar, Dhaka-1341 Open Sunday, Tuesday, Thursday ATI BAZAR BRANCH Dhaka Hazi Nuruddin Plaza House#13,ATI Bazar, Keranigonj ,Dhaka -1312 Open Sunday, Tuesday, Thursday BADDA SMESC Dhaka The Pearl Trade Center (PTC),Holding No: Cha- 90/3,Progoti Shoroni Road, Ward No-21,Thana-Badda,Dhaka Open Everyday Shaikh Mansion, Holding# 226, Main road, Ward# 05, Rahater Mor, 1st floor, Pourashava & Thana# Bagerhat, Dist. BAGERHAT SME/KRISHI BRANCH Khulna Open Everyday Bagerhat BAHADDERHAT SMESC Chittagong Mamtaz Tower, 4540 Arakan Road, Bahaddarhat, Chittagong. Open Everyday BANANI - 11 BRANCH Dhaka South Breeze Center,Plot # 5, Building-G (1st & 2nd Floor), Road-11, Banani,Dhaka-1213 Closed BANANI BRANCH Dhaka Borak Mehnoor, Holding # 51/B, Kamal Ataturk Avenue, Banani C/A, Ward: 19; Dhaka-1213, Bangladesh Open Everyday BANDARTILA SMESC Chittagong Osman Plaza, 1st Floor, 800/new, MA Aziz Road, Airport road, Bondortila, Chittagong. Open Everyday BANIACHONG BRANCH Sylhet Hazi Harun Mansion, Holding No # 5, BoroBazar, Baniachong, Habigonj. Open Sunday, Tuesday, Thursday BARISALBRANCH Barisal S. -

BARGUNA District: AMTALI Upazila/Thana: Slno Eiin Name Of

Upazila/Thana Wise list of Institutes District: BARGUNA Upazila/Thana: AMTALI Slno Eiin Name of the Institution Vil/Road Mobile 1 134886 SOUTH BENGAL IDEAL SCHOOL AND COLLEGE AMTALI 01734041282 2 100022 MAFIZ UDDIN GIRLS PILOT HIGH SCHOOL UPZILA ROAD 01718101316 3 138056 PURBO CHAWRA GOVT. PRIMARY SCHOOL PATAKATA 01714828397 4 100051 UTTAR TIAKHALI JUNIOR GIRLS HIGH SCHOOL UTTAR TIAKHALI 01736712503 5 100016 CHARAKGACHIA SECONDARY SCHOOL CHARAKGACHIA 01734083480 6 100046 KHAGDON JUNIOR HIGH SCHOOL KHAGDON 01725966348 7 100028 SHAHEED SOHRAWARDI SECONDARY SCHOOL KUKUA 01719765468 8 100044 GHATKHALI HIGH SCHOOL GHATKHALI 01748265596 9 100038 KALAGACHIA YUNUS A K JUNIOR HIGH SCHOOL KALAGACHIA 01757959215 10 100042 K H AKOTA JUNIOR HIGH SCHOOL KALAGACHHIA 01735437438 11 100039 HALIMA KHATUN G R GIRLS HIGH SCHOOL GULISHAMALI 01721789762 12 100034 KHEKUANI HIGH SCHOOL KHEKUANI 01737227025 13 100023 GOZ-KHALI(MLT) HIGH SCHOOL GOZKHALI 01720485877 14 100037 ATHARAGACHIA SECONDARY SCHOOL ATHARAGACHIA 01712343508 15 100017 EAST CHILA RAHMANIA HIGH SCHOOL PURBA CHILA 01716203073,011 90276935 16 100009 LOCHA JUUNIOR HIGH SCHOOL LOCHA 01553487462 17 100048 MODDHO CHANDRA JUNIOR HIGH SCHOOL MODDHO CHANDRA 01748247502 18 100020 CHALAVANGA HIGH SCHOOL PRO CHALAVANGA 01726175459 19 100011 AMTALI A.K. PILOT HIGH SCHOOL 437, A K SCHOOL ROAD, AMTALI 01716296310 20 100026 ARPAN GASHIA HIGH SCHOOL ARPAN GASHIA 01724183205 21 100018 TARIKATA SECONDARY SCHOOL TARIKATA 01714588243 22 100014 SHAKHRIA HIGH SCHOOL SHAKHARIA 01712040882 23 100021 CHUNAKHALI HIGH -

Internship Report “Analysis of Banking Industry & Janata Bank Limited”

Internship Report On “Analysis of Banking Industry & Janata Bank Limited” “Analysis of Banking Industry & Janata Bank Limited”: An Internship Report Submitted to: Dr. Md. Mohan Uddin Professor Submitted by: Arup Saha ID- 111 143 003 October 9, 2018 UNITED INTERNATIONAL UNIVERSITY Letter of Transmittal October 9, 2018 Dr. Md. Mohan Uddin Professor School of Business & Economics United International University Subject: Submission of Internship report Dear Sir, It is indeed, an honor to deliver my internship report on “Analysis of Banking Industry & Janata Bank Limited”, as a prerequisite for the completion of my BBA program, as per your instructions. In preparing this report, I have tried my best to include all the related information to make the report magnificent and workable one and in doing so I have tried my outermost to live up to your criterion. It will be a happy moment for me if I hear further clarification from you. May I, Therefore, hope that you would be kind enough to accept my endeavor and oblige thereby. Yours Sincerely, ……………............ Arup Saha ID - 111 143 003 United International University Acknowledgement At first, I would like to express my profound gratefulness to almighty GOD for giving me strength and mobility to finish the report within time Then, I congratulated and lay my sincerest thankfulness to my honorable supervisor, Dr. Md. Mohan Uddin, Professor, United International University, for his help, encouragement, guidance, and valuable suggestions throughout the entire period of this study, within which it could not have been feasible to submit this report on time. It was an eminent scope for me to complete my internship program at Janata Bank Limited, Hazaribagh Branch.