Cover Sheet Cs 0 0 0 0 3 9 5 8 7

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

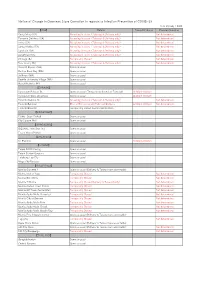

Notice of Change in Overseas Store Operation in Regards to Infection

Notice of Change in Overseas Store Operation in regards to Infection Prevention of COVID-19 As of 21/July / 2020 【USA】 Details Temp Biz Hours Planned Duration Costa Mesa (CA) No eating in-store(Take out & Delivery only) Not determined Torrance Del Amo (CA) No eating in-store(Take out & Delivery only) Not determined Irvine (CA) No eating in-store(Take out & Delivery only) Not determined Santa Monica (CA) No eating in-store(Take out & Delivery only) Not determined San Jose (CA) No eating in-store(Take out & Delivery only) Not determined San Diego (CA) No eating in-store(Take out & Delivery only) Not determined Chicago (IL) Temporarily Closed Not determined New Jersey (NJ) No eating in-store(Take out & Delivery only) Not determined Harvard Square (MA) Open as usual Boston Back Bay (MA) Open as usual Bellevue (WA) Open as usual Seattle University Village (WA) Open as usual Hawaii Kaheka (HI) Open as usual 【CANADA】 Vancouver Robson St. Open as usual (Temporarily closed on Tuesday) 11:00pm-8:00pm Vancouver West Broadway Open as usual 11:00pm-8:00pm Toronto Dandus St. No eating in-store(Take out & Delivery only) Not determined Toronto Eglinton Dine-in(Terrace seat)/Take out/Delivery 12:00pm-9:00pm Not determined Toronto Bloor St. Temporarily closed due to construction 【SINGAPORE】 Clarke Quay Central Open as usual City Square Mall Open as usual 【HONG KONG】 iSQUARE Tsim Sha Tsui Open as usual Tsuen Wan OP Mall Open as usual 【MALAYSIA】 KL Pavilion Open as usual 10:00pm-8:00pm 【TAIWAN】 Taipei SOGO Fuxing Open as usual Taipei Station Qsquare Open -

SEC Form 17A – 2019

June 18, 2020 PHILIPPINE STOCK EXCHANGE 9th Floor, Philippine Stock Exchange Tower 28th Street corner 5th Avenue, BGC Taguig City Attention: Ms. Janet A. Encarnacion Head, Disclosure Department Subject: Vistamalls Inc.: SEC 17A – December 31, 2019 Gentlemen: Please see attached SEC 17A Report. Thank you. Truly Yours, Brian N. Edang Officer-In-Charge COVER SHEET C S 0 0 0 0 3 9 5 8 7 S.E.C. Registration Number V I S T A M A L L S , I N C . ( F O R M E R L Y S T A R M A L L S , I N C . ) (Company’s Full Name) L O W E R G R O U N D F L O O R , B U I L D I N G B , E V I A L I F E S T Y L E C E N T E R , V I S T A C I T Y , D A A N G H A R I , A L M A N Z A I I L A S P I Ñ A S C I T Y (Business Address: No. Street/City/Province) Brian N. Edang 8571-5948 Contact Person Registrant Telephone Number 1 2 3 1 17 -A Month Day FORM TYPE Month Day Calendar Year Annual Meeting Secondary License Type, If Applicable Dept. Requiring this Doc. Amended Articles Number/Section Total Amount of Borrowings Total No. of Domestic Foreign Stockholders ---------------------------------------------------------------------------------------------------------- To be accomplished by SEC Personnel concerned File Number LCU Document I.D. Cashier 0 SECURITIES AND EXCHANGE COMMISSION SEC FORM 17-A ANNUAL REPORT PURSUANT TO SECTION 17 OF THE SECURITIES REGULATION CODE AND SECTION 141 OF THE CORPORATION CODE OF THE PHILIPPINES 1. -

Merchant Branch List

Merchant Branch List Anson’s at Landmark Sta. Lucia East Grand Mall Siklab SM City Lucena The Landmark, Makati The District Imus Greenbelt 3 SM City Marilao The Landmark, Trinoma UP Town Center Nuvali SM City Masinag Waltermart Makati SM City San Pablo Applebee’s T.G.I. Friday’s SM City Sta. Rosa Bonifacio Global City The Bistro Group Abreeza Mall, Davao City SM City Tarlac Eastwood City Baker and Cook Alabang Town Center SM City Taytay S Maison, Conrad Manila Ayala Center Cebu SM Fairview Arena Ayala Fairview Terraces SM Mall of Asia Alabang Town Center Buffalo Wild Wings Bonifacio High Street SM Megamall Shangri-La Plaza Mall Conrad Hotel Manila Boracay, Station 1 SM Southmall SM City North EDSA Estancia Mall Centrio Mall, CDO Sta. Lucia East Grand Mall - 2/F UP Town Center Glorietta 2 Eastwood City Walk 1 Sta. Lucia East Grand Mall - G/F Uptown Mall, BGC Evia Lifestyle Center, Las Piñas Sta. Lucia East Grand Mall 3/F The Athlete’s Foot Vista Mall, Sta. Rosa Glorietta 3 Visayas Avenue, Quezon City Abreeza Mall, Davao City Greenbelt 3 Waltermart - Pampanga Alabang Town Center Bulgogi Brothers Harbor Point, Subic West Avenue, Quezon City Ayala Center Cebu Alabang Town Center Marquee Mall, Angeles City Ayala Two Parkade, BGC Glorietta 2 Mckinley Hill, Venice Grand Canal Bizu Patisserie and Bistro Glorietta 2 Greenbelt 5 Robinsons Galleria Alabang Town Center Glorietta 3 Harbor Point Robinsons Place Manila Eastwood Mall Limketkai Mall, CDO Newport Mall SM Mall of Asia Greenbelt 2 Marquee Mall, Angeles City SM Lanang Premier SM Southmall One Rockwell Robinsons Bacolod SM Mall of Asia Solenad 3, Nuvali Robinsons Magnolia Robinsons Dumaguete Tomas Morato Avenue St. -

Intellectual Property Center, 28 Upper Mckinley Rd. Mckinley Hill Town Center, Fort Bonifacio, Taguig City 1634, Philippines Tel

Intellectual Property Center, 28 Upper McKinley Rd. McKinley Hill Town Center, Fort Bonifacio, Taguig City 1634, Philippines Tel. No. 238-6300 Website: http://www.ipophil.gov.ph e-mail: [email protected] Publication Date: 17 November 2020 1 ALLOWED MARKS PUBLISHED FOR OPPOSITION .................................................................................................... 2 1.1 ALLOWED NATIONAL MARKS ............................................................................................................................................. 2 Intellectual Property Center, 28 Upper McKinley Rd. McKinley Hill Town Center, Fort Bonifacio, Taguig City 1634, Philippines Tel. No. 238-6300 Website: http://www.ipophil.gov.ph e-mail: [email protected] Publication Date: 17 November 2020 1 ALLOWED MARKS PUBLISHED FOR OPPOSITION 1.1 Allowed national marks Application Filing No. Mark Applicant Nice class(es) Number Date 13 1 4/2018/00002788 February PRIMEA Aldex Realty Corporation [PH] 43 2018 24 April KITCHEN CITY 2 4/2018/00006872 Artemisplus Express, Inc. [PH] 43 2018 EXPRESS 26 June 3 4/2018/00010926 COCO TERO Eric Jison Ledesma [PH] 29; 30 and32 2018 8 October DELPHI Delphi Technologies IP 4 4/2018/00017889 1; 4; 7; 9 and12 2018 TECHNOLOGIES Limited [BB] 11 October Quantum Mobile Gears Corp. 5 4/2018/00018222 MOBILE MONKEY 9; 16 and35 2018 [PH] 23 January PT ANEKA KARYA KOPI 6 4/2018/00500280 JAVA JAZZ COFFEE 30 and43 2018 INDONESIA [ID] MEDTRIX HOSPITAL 8 October 7 4/2018/00504980 MANAGEMENT Duenas, John Dave [PH] 42 2018 SOFTWARE 4 January 8 4/2019/00000227 RAINBOW SANDALS Rainbow Sandals, Inc. [US] 25 2019 23 January 9 4/2019/00001242 MENQUADTT Sanofi Pasteur Inc. [US] 5 2019 COMMITTED TO 11 ASSIST Alburo Alburo and Associates 10 4/2019/00002129 February 45 ENTREPRENEURS TO Law Offices [PH] 2019 SUCCEED HUE-YOUR SOLE IDENTITY. -

List of Participating Restauraints Aind Shops A. Restauraints 1. Akira Sushi Teppanyaki 47. Ogetsu Hime 2. Akitaya Japanese Rest

List of Participating Restauraints aind Shops Click the name of Restaurant or Shop to view the branches. a. Restauraints 1. Akira Sushi Teppanyaki 47. Ogetsu Hime 2. Akitaya Japanese Restaurant 48. Ohsama Ramen 3. Asakusa 49. Omakase 4. Azami Restaurant 50. Ooedo Japanese Restaurant 5. Bon Chon 51. Ooma 6. Botejyu 52. Osaka Ohsho 7. Bulgogi Brothers 53. Oyasumi Ramen 8. Butamaru 54. Paper Moon Cafe 9. Chairman Wang 55. Pepper Lunch 10. Coco Ichibanya 56. Rai Rai Ken 11. Dohtonbori 57. Ramen Cool 12. Fuji Soba 58. Ramen Kuroda 13. Gen Korean BBQ House 59. Ramen Nagi 14. Genki Sushi 60. Ramen Yushoken 15. Hanamaruken 61. Saisaki 16. Healthy Shabu Shabu 62. Sakura Ko 17. Hokkaido Ramen Santouka 63. Sambokojin 18. Ichiban Mix Bufet 64. Samgyupsalamat 19. Ikkoryu Fukuoka Ramen 65. Sandaime 20. Ippon Yari Ramen House 66. Sandaya Japanese Restaurant 21. Ippudo 67. Seoul Garden 22. Isshin Japanese Restaurant 68. Shabu Shabu Ichiban 23. Japanfudo Street 69. Shabuway 24. Jin Joo Korean Grill 70. Shinzen Japanese Cuisine 25. Jipan 71. Sumo Sam 26. John And Yoko 72. Sushi Tsumura 27. Jyukai Japanese Restaurant 73. Tajimaya Charcoal Grill 28. K Pub Bbq 74. Tanabe Japanese Restaurant 29. Katsu 75. Tapella 30. Katsu Sora 76. Tempura Japanese Grill 31. Kaya Restaurant 77. Tenya 32. Kenji-Tei 78. Teppanya 33. Kichitora 79. Teriyaki Boy 34. Kimono Ken 80. Tetsu Teppanyaki 35. Kimpura 81. Tsukiji 36. Kojiro Restaurant 82. Tsuru Japanese Restaurant 37. Korean Garden Restaurant 83. UCC 38. Little Nonki Japanese Restaurant 84. Uma U ma Ramen 39. Maisen 85. Watami 40. -

SEC Form 17-C for Filing Today with the Securities and Exchange Commission

3rd Level Starmall Las Piñas, CV Starr Avenue, Philamlife Village, Pamplona, Las Piñas City Call (+632) 8714001 / Fax No. (+632) 8724697 June 18, 2012 PHILIPPINE STOCK EXCHANGE 3rd Floor Philippine Stock Exchange Plaza Ayala Triangle, Ayala Avenue Makati City Attention: Ms. Janet A. Encarnacion Head, Disclosures Department Subject: Polar Property Holdings Corporation: Corporate Disclosure Gentlemen: Please find attached SEC Form 17-C for filing today with the Securities and Exchange Commission. Thank you. Truly Yours, Jo L. Ilijay Officer-In-Charge 1 COVER SHEET C S 0 0 0 0 3 9 5 8 7 S.E.C. Registration Number P O L A R P R O P E R T Y H O L D I N G S C O R P O R A T I O N (Company’s Full Name) 3 R D L E V E L S T A R M A L L L A S P I N A S , C V S T A R R A V E N U E , P H I L A M L I F E V I L L A G E , P A M P L O N A , L A S P I N A S C I T Y (Business Address : No. Street/City/Province) Jo L. Ilijay 871-4001 Contact Person Company Telephone Number 1 2 3 1 17C 0 6 2 7 Month Day FORM TYPE Month Day Calendar Year Annual Meeting Secondary License Type, If Applicable Dept. Requiring this Amended Articles Doc. Number/Section Total Amount of Borrowings Total No. -

Sec Form 17-A

April 15, 2019 PHILIPPINE STOCK EXCHANGE 9th Floor, Philippine Stock Exchange Tower, 28th Street corner 5th Avenue, BGC Taguig City Attention: Janet A. Encarnacion Head, Disclosure Department Subject: Starmalls, Inc.: SEC 17A – December 31, 2018 Gentlemen: Please see attached SEC 17A Report. Thank you. Brian N. Edang Officer-in-Charge COVER SHEET C S 0 0 0 0 3 9 5 8 7 S.E.C. Registration Number S T A R M A L L S , I N C . (Company’s Full Name) L O W E R G R O U N D F L O O R , B U I L D I N G B , E V I A L I F E S T Y L E C E N T E R , V I S T A C I T Y , D A A N G H A R I , A L M A N Z A I I L A S P I Ñ A S C I T Y (Business Address: No. Street/City/Province) Brian N. Edang 571-5948 / 871-4001 Contact Person Registrant Telephone Number 1 2 3 1 17 -A Month Day FORM TYPE Month Day Calendar Year Annual Meeting Secondary License Type, If Applicable Dept. Requiring this Doc. Amended Articles Number/Section Total Amount of Borrowings Total No. of Domestic Foreign Stockholders ---------------------------------------------------------------------------------------------------------- To be accomplished by SEC Personnel concerned File Number LCU Document I.D. Cashier 0 SECURITIES AND EXCHANGE COMMISSION SEC FORM 17-A ANNUAL REPORT PURSUANT TO SECTION 17 OF THE SECURITIES REGULATION CODE AND SECTION 141 OF THE CORPORATION CODE OF THE PHILIPPINES 1. -

Max's Restaurant, Pancake House and Jamba Juice PARTICIPATING REDEMPTION STORES

Shop. Choose. Redeem with Max's Restaurant, Pancake House and Jamba Juice PARTICIPATING REDEMPTION STORES Max's Restaurant Location Name Address 10th Avenue 261 Delfina Bldg., corner Baltazar St 10th Avenue Abreeza 2/F Abreeza Mall J.P. Laurel Ave, Bajada Ayala Malls Manila Bay Ayala Malls Manila Bay Diosdado Macapagal Blvd, cor Aseana Ave. Balanga Aguirre St., Poblacion Caltex NLEX Valenzuela Caltex NLEX Valenzuela E1 Caltex Sct Borromeo Caltex Scout Borromeo St., Diliman Cauayan City Rivera St., Center Mall Tutuban G/F Tutuban Center Mall CM Recto Avenue, Divisoria Commonwealth Fairview Lot 6 Commonwealth Ave Olivarez Plaza 2/F Olivarez Plaza 4030 National Hwy Petron San Jose Nueva Ecija Petron San Jose Pan-Philippine Highway Shell C5-Heritage C5 Southbound, Carlos P. Garcia Ave Shell Don Antonio Don Antonio Dr, Diliman Silang Cavite Emilio Aguinaldo Hwy SM Puerto Princesa SM Puerto Princesa PPVQ+59 Barangay San Miguel Tanay R-5 RPL Valencia Courtyard L-140 Robinsons Place Bagontaas EDSA Borromeo Lot 1 Blk. S155 Edsa cor. Scout Borromeo, South Triangle Robinsons Galleria South 1/F Robinsons Galleria South Km. 31, National Highway, Brgy. Nueva Sto. Tomas Gateway Drive Maharika Highway, Lipa Town Center Lipa Town Center Brgy. Sico Vista Place Taguig G/F Vista Place Levi Mariano Ususan SM Olongapo Central SM Olongapo Central Rizal Ave Gapan 00 Greenwoods Ave., Brgy. Bayanihan Bacolor Pampanga Jose Abad Santos St., Macabacle EDSA Eats 537 EDSA Corner Main Avenue Bagong Lipunan ng Crame 4 Shell Don Antonio Shell Don Antonio Don Antonio Dr, Diliman Abreeza Mall 2nd Floor Abreeza, Ayala Mall J.P. -

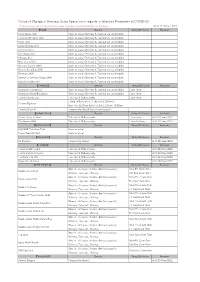

Notice of Change in Overseas Store Operation in Regards to Infection

Notice of Change in Overseas Store Operation in regards to Infection Prevention of COVID-19 *There may be a limit on the number of seats to prevent infection depending on the store. As of 17 /June / 2021 【USA】 Details Temp Biz Hours Remarks Costa Mesa (CA) Open as usual (Delivery & Takeout are accectable) Torrance Del Amo (CA) Open as usual (Delivery & Takeout are accectable) Irvine (CA) Open as usual (Delivery & Takeout are accectable) Santa Monica (CA) Open as usual (Delivery & Takeout are accectable) San Jose (CA) Open as usual (Delivery & Takeout are accectable) San Diego (CA) Open as usual (Delivery & Takeout are accectable) Chicago (IL) Open as usual (Delivery & Takeout are accectable) New Jersey (NJ) Open as usual (Delivery & Takeout are accectable) Harvard Square (MA) Open as usual (Delivery & Takeout are accectable) Boston Back Bay (MA) Open as usual (Delivery & Takeout are accectable) Bellevue (WA) Open as usual (Delivery & Takeout are accectable) Seattle University Village (WA) Open as usual (Delivery & Takeout are accectable) Hawaii Kaheka (HI) Open as usual (Delivery & Takeout are accectable) 【CANADA】 Details Temp Biz Hours Remarks Vancouver Robson St. Open as usual (Delivery & Takeout are accectable) 11am-9pm Vancouver West Broadway Open as usual (Delivery & Takeout are accectable) 11am-9pm Toronto Dandus St. Take out & Delivery only 11am-9pm Eating at Patio seat / Take out & Delivery) Toronto Eglinton Sun-Thu 11:30am-9pm/Fri-Sat 11:30am-10:30pm Toronto Bloor St. Temporarily closed due to construction 【SINGAPORE】 Details -

Alabang – the New Central Business District in the South

www.PreSelling.com.ph *FOR TRAINING PURPOSES ONLY Live Unlimited www.PreSelling.com.ph *FOR TRAINING PURPOSES ONLY LTS No. 033500 Artist’s Rendition of Anantara Square Building Live Unlimited Located in close proximity to progressive Alabang – the New Central Business District in the South www.PreSelling.com.ph A Central Business District or commonly referred to as “CBD” is an area that never ceases to evolve into a more dynamic cosmopolitan scene. It is positioned as a melting pot of top multinational and local corporations, commercial and residential establishments, as well as educational and medical institutions. *FOR TRAINING PURPOSES ONLY Alabang: The Next Central Business District in the South www.PreSelling.com.ph Alabang is the new CBD in Metro Manila, following the footsteps of Makati, Fort Bonifacio and Ortigas. Aside from serving as an alternate hub for some major multinational corporations, Alabang is known to be a commercial and residential hub in southern Metro Manila. *FOR TRAINING PURPOSES ONLY Alabang: The Next Central Business District in the South Due to it being a major thoroughfare in the south and being very accessible for the commuting public, it’s no surprise why a lot of today’s most popular supermalls are found within the part. SM Southmall, Robinson’s Place Las Pinas, Alabang Town Center and Festival Mall are all found in close proximity with each other in the area. Established business districts and techno parks like Spectrum Businesswww.PreSelling.com.ph District, Madrigal Business Park and Northgate Cyberzone also settled their operations in Alabang which further boosted its employment opportunities. -

Intellectual Property Center, 28 Upper Mckinley Rd

Intellectual Property Center, 28 Upper McKinley Rd. McKinley Hill Town Center, Fort Bonifacio, Taguig City 1634, Philippines Tel. No. 238-6300 Website: http://www.ipophil.gov.ph e-mail: [email protected] Publication Date: 19 August 2021 1 ALLOWED MARKS PUBLISHED FOR OPPOSITION .................................................................................................... 2 1.1 ALLOWED NATIONAL MARKS ............................................................................................................................................. 2 Intellectual Property Center, 28 Upper McKinley Rd. McKinley Hill Town Center, Fort Bonifacio, Taguig City 1634, Philippines Tel. No. 238-6300 Website: http://www.ipophil.gov.ph e-mail: [email protected] Publication Date: 19 August 2021 1 ALLOWED MARKS PUBLISHED FOR OPPOSITION 1.1 Allowed national marks Application Filing No. Mark Applicant Nice class(es) Number Date MISS & MRS. NOBLE 16 October 1 4/2019/00018073 QUEEN Sit Yow Ying [MY] 41 2019 INTERNATIONAL 8 January PERFORMANCE FOODS 2 4/2020/00500126 CINDYS HAMBURGER 43 2020 CORPORATION [PH] 14 May 3 4/2020/00503885 YES FOR PEACE INC. [PH] 16; 35 and45 2020 16 July CERES PHARMA- Ceres Summit Corporation 4 4/2020/00508792 1; 3 and5 2020 GALENICALS [PH] 1 August Javier Mondoñedo, Tanya 5 4/2020/00509471 DULCET SKIN 3 and5 2020 Katrina [PH] 2 August NAN PAO INTERNATIONAL 6 4/2020/00509492 NAN PAO 5 2020 BIOTECH. CO., LTD. [TW] 3 August 7 4/2020/00509558 BEYOND BUTTER Naked Foods Pantry, Inc. [PH] 29 2020 1 8 4/2020/00511528 September CITI FLEXI CASH Citigroup Inc. [US] 36 2020 9 9 4/2020/00512249 September Microsoft Corporation [US] 35 2020 18 10 4/2020/00513116 September GEARS D'OUTDOOR, INC. [PH] 12 2020 30 11 4/2020/00514217 September ALLGREEN ALLDAY MARTS, INC. -

Merchant Name ADDRESS Gong Cha - Alabang Town Centre 1014 G/F EXPANSION WING the GARDEN ALABANG TOWN CENTER BRGY

GONG CHA Merchant Name ADDRESS Gong Cha - Alabang Town Centre 1014 G/F EXPANSION WING THE GARDEN ALABANG TOWN CENTER BRGY. AYALA ALABANG, MUNTINLUPA CITY Gong Cha - Araneta Center 0068/0068 Shopwise Arcade Cubao, Quezon City Gong Cha - Araneta Cyberpark Unit P1UG002S, Cyberpark Tower 1, Araneta Center, General Aguinaldo Ave., Cubao, Q.C Gong Cha - Avenue of The Arts Residences ROXAS BLVD. CORNER STA. MONICA & L.M GUERRERO ST., ERMITA MANILA Gong Cha - Ayala Fairview Terraces L075 LG/F FAIRVIEW TERRACES QUIRINO HIGHWAY BRGY. PASONG PUTIK, QUEZON CITY Gong Cha - Ayala Mall Feliz Unit 543-545, 5/F, Ayala Malls Feliz, Marcos Hi-way, Brgy. De la paz, Pasig City Gong Cha - Ayala Mall Serin 1st Floor, Bldg. A, Food 43 Tagaytay- Nasugbo Highway Brgy., Crossing Silang East Tagaytay Gong Cha - Cardinal Unit 10 & 11 Steel Parking ConcessionaireCardinal Santos Medical Center, Wilson St.,Greenhills West San Juan City, Manila Gong Cha - Clover Leaf 429 4th Level Clover Leaf Balintawak, Quezon City Gong Cha - Evia Unit 3F-5C, 3/F, EVIA Lifestyle Center, Daang Hari Roa, Las Piñas City Gong Cha - Fastbytes Fastbytes Center, Northgate Cyberzone, Filinvest City, Alabang Muntinlupa City Gong Cha - Festival Mall Unit 3402 1, 2/F, Festival Supermall Expansion, Alaban, Muntinlupa City Gong Cha - Fishermall CT 002, G/F, Fisher Mall, 325 Quezon Avenue, Brgy. Sta. Cruz, Quezon City Gong Cha - Fort Bonifacio/ SM Aura UNIT 407-408 LEVEL 4 SM AURA PREMIER MCKINLEY PARKWAY BRGY. FORT BONIFACIO, TAGUIG CITY Gong Cha - Fort Victoria Unit 102 G/F Shoppesville@Victoria 5th Ave. cor. 23rd St. Fort Bonifacio Global city Taguig Gong Cha - Glorietta 4 FOOD CHOICES GLORIETTA 4 AYALA CENTER BRGY.