Annual Report 2019 Making an Impact

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

List of Clinics in Downtown Core Open on Friday 24 Jan 2020

LIST OF CLINICS IN DOWNTOWN CORE OPEN ON FRIDAY 24 JAN 2020 POSTAL S/N NAME OF CLINIC BLOCK STREET NAME LEVEL UNIT BUILDING TEL OPENING HOURS CODE 1 ACUMED MEDICAL GROUP 16 COLLYER QUAY 02 03 INCOME AT RAFFLES 049318 65327766 8.30AM-12.30PM 2 AQUILA MEDICAL 160 ROBINSON ROAD 05 01 SINGAPORE BUSINESS FEDERATION CENTER 068914 69572826 11.00AM- 8.00PM 3 AYE METTA CLINIC PTE. LTD. 111 NORTH BRIDGE ROAD 04 36A PENINSULA PLAZA 179098 63370504 2.30PM-7.00PM 4 CAPITAL MEDICAL CENTRE 111 NORTH BRIDGE ROAD 05 18 PENINSULA PLAZA 179098 63335144 4.00PM-6.30PM 5 CITYHEALTH CLINIC & SURGERY 152 BEACH ROAD 03 08 GATEWAY EAST 189721 62995398 8.30AM-12.00PM 6 CITYMED HEALTH ASSOCIATES PTE LTD 19 KEPPEL RD 01 01 JIT POH BUILDING 089058 62262636 9.00AM-12.30PM 7 CLIFFORD DISPENSARY PTE LTD 77 ROBINSON ROAD 06 02 ROBINSON 77 068896 65350371 9.00AM-1.00PM 8 DA CLINIC @ ANSON 10 ANSON ROAD 01 12 INTERNATIONAL PLAZA 079903 65918668 9.00AM-12.00PM 9 DRS SINGH & PARTNERS, RAFFLES CITY MEDICAL CENTRE 252 NORTH BRIDGE RD 02 16 RAFFLES CITY SHOPPING CENTRE 179103 63388883 9.00AM-12.30PM 10 DRS THOMPSON & THOMSON RADLINK MEDICARE 24 RAFFLES PLACE 02 08 CLIFFORD CENTRE 048621 65325376 8.30AM-12.30PM 11 DRS. BAIN + PARTNERS 1 RAFFLES QUAY 09 03 ONE RAFFLES QUAY - NORTH TOWER 048583 65325522 9.00AM-11.00AM 12 DTAP @ DUO MEDICAL CLINIC 7 FRASER STREET B3 17/18 DUO GALLERIA 189356 69261678 9.00AM-3.00PM 13 DTAP @ RAFFLES PLACE 20 CECIL STREET 02 01 PLUS 049705 69261678 8.00AM-3.00PM 14 FULLERTON HEALTH @ OFC 10 COLLYER QUAY 03 08/09 OCEAN FINANCIAL CENTRE 049315 63333636 -

Office Listing & Rental Price

Office Listing & Rental Price Subject to availability, survey, approval and contract Asking rents are subject to revision without any notice Francis Goh (65) 97305200 [email protected] CEA Reg. No: R041398H TYPE DISTRICT LOCATIONS ADDRESS SIZE (SQFT) PSF (S$) PRICE (S$) AVAILABLE REMARKS Retail (F&B) 1 Crown at Robinson 140 Robinson Road 068907 2,508 13.00 32,604 Immediate Fitted Office 1 Crown at Robinson 140 Robinson Road 068907 592 9.00 5,328 Immediate Bare Office 1 Crown at Robinson 140 Robinson Road 068907 592 9.00 5,328 Immediate Bare Office 1 Crown at Robinson 140 Robinson Road 068907 592 9.00 5,328 Immediate Partially fitted Office 1 Crown at Robinson 140 Robinson Road 068907 926 9.00 8,334 Immediate Partially fitted Office 1 Crown at Robinson 140 Robinson Road 068907 6,792 9.00 61,128 Immediate Fitted Office 1 Crown at Robinson 140 Robinson Road 068907 1,485 9.00 13,365 Immediate Penthouse office (Furnished and fitted) Office 1 UOB Plaza 1 No. 80 Raffles Place 1,862 11.00 20,482 Immediate Bare Office 1 UOB Plaza 1 No. 80 Raffles Place 5,253 11.00 1,500 Immediate Fitted Office 1 UOB Plaza 1 No. 80 Raffles Place 5,963 11.00 1,500 Immediate Bare Office 1 UOB Plaza 1 No. 80 Raffles Place 12,206 11.00 134,266 Immediate Bare Office 1 UOB Plaza 1 No. 80 Raffles Place 2,099 11.00 23,089 Immediate Fitted Office 1 UOB Plaza 1 No. 80 Raffles Place 2,454 11.00 26,994 1-May-21 Fitted Office 1 UOB Plaza 1 No. -

A Review of the Singapore Office Market

Singapore Q1/Q2 2019 Published 1st March 2019 Singapore | Hong Kong The Office A review of the Singapore office market Index P2 Building Rental Table (Islandwide) P3 Leasing Options – New Downtown & Economy Range P4 Demand – who is moving where P5 Featured New Development – 9 Penang Road P6 Special Feature – Co-working space P7 Leasing Options – Raffles Place & Tanjong Pagar P8 Supply / Rentals / Forecast Corporate Locations (S) Pte Ltd License No. L3010044A Marina One T +65 6320 8355 / [email protected] / www.corporatelocations.com.sg RENTAL GUIDE 1st March 2019 Summary of Asking Rates Raffles Place / New Downtown Bangkok Bank Building TBA City Hall / Marina Centre / Beach Rd Chinatown / River Valley Road BEA Building $7.50 18 Robinson $12.00 Capital Tower $10.00 11 Beach Road Full Central Mall $7.00 20 Collyer Quay $11.00-$13.00 Cecil Court $5.80 30 Hill Street Full CES Centre $5.50+ 55 Market Street $7.00 China Square Central $8.50 Beach Centre $7.80 Chinatown Point $6.50 6 Battery Road $14.00 City House $7.80+ Bugis Junction Towers $7.80 Great World City $7.00 Asia Square T1 & T2 $14.00 Far East Finance Bldg $7.00 Centennial Tower $14.80 Kings Centre $7.00 Bank of China Building Full Far Eastern Bank Bildg Full Duo Tower $10.50 The Central $9.80 Bank of Singapore Centre $9.50 GB Building $6.00+ Funan $9.00 UE Square $8.00 Bharat Building $6.50 Keck Seng Tower $6.00 Manulife Centre $10.00+ Valley Point $7.00 CapitaGreen $13.50 Manulife Tower $9.50 Millenia Tower $14.80 Capital Square Full MYP Plaza $7.00 Odeon Tower -

Capitaland Retail China Trust Annual Report 2017 Optimising Growth

OPTIMISING GROWTH CAPITALAND RETAIL CHINA TRUST ANNUAL REPORT 2017 OPTIMISING GROWTH At CapitaLand Retail China Trust (CRCT), we strive to enrich lives through high- quality real estate products and services. Inspired by CapitaLand’s credo of ‘Building People. Building Communities.’, the design for this year’s annual report employs the creative use of mosaic to recreate Rock Square – a new addition to our portfolio. Just as different mosaic pieces come together to form a big picture, this is symbolic of how CRCT will continue to build on our strengths to propel our growth journey and create greater value for the future. We continue to build on the momentum from our milestone decade of growth by sharpening our competitiveness, extracting value and strengthening the quality of our portfolio. Through our strategy of investing in high-quality income-producing retail assets, coupled with proactive asset management and disciplined capital management, we remain focused in creating sustainable long-term value for our Unitholders. VISION MISSION Sustainable and resilient REIT with a Deliver sustainable income growth to our professionally managed portfolio of quality Unitholders and value-add to the community retail real estate across China. and stakeholders by enhancing organic growth through proactive asset management; creating new value through innovative asset enhancement strategies; and capitalising on yield-accretive acquisitions growth. 1 ANNUAL REPORT 2017 CORPORATE PROFILE OVERVIEW FIRST CHINA SHOPPING MALL REAL ESTATE INVESTMENT TRUST IN SINGAPORE CapitaLand Retail China Trust (CRCT) is the first China shopping mall real estate investment trust (REIT) in Singapore. Listed on the Singapore Exchange Securities Trading Limited (SGX-ST) on 8 December CORPORATE GOVERNANCE & TRANSPARENCY GOVERNANCE CORPORATE 2006, CRCT is established with the objective of investing on a long-term basis in a diversified portfolio of income-producing real estate used primarily for retail purposes and located primarily in China, Hong Kong and Macau. -

MUSLIM VISITOR GUIDE HALAL DINING•PRAYERHALAL SPACES • CULTURE • STORIES to Singapore Your FOREWORD

Your MUSLIM VISITOR GUIDE to Singapore HALAL DINING • PRAYER SPACES • CULTURE • STORIES FIRST EDITION | 2020 | ENGLISH VERSION EDITION | 2020 FIRST FOREWORD Muslim-friendly Singapore P18 LITTLE INDIA Muslims make up 14 percent of Singapore’s population As a Muslim traveller, this guide provides you and it is no surprise that this island state offers a large with the information you need to enjoy your stay variety of Muslim-friendly gastronomic experiences. in Singapore — a city where your passions in life MASJID SULTAN P10 KAMPONG GLAM Many of these have been Halal certified by MUIS, are made possible. You may also download the P06 ORCHARD ROAD also known as the Islamic Religious Council of MuslimSG app and follow @halalSG on Twitter for Singapore (Majlis Ugama Islam Singapura). Visitors any Halal related queries while in Singapore. can also consider Muslim-owned food establishments throughout the city. Furthermore, mosques and – Majlis Ugama Islam Singapura (MUIS) musollahs around the island allow you to fulfill your P34 ESPLANADE religious obligations while you are on vacation. TIONG BAHRU P22 TIONGMARKET BAHRU P26 CHINATOWN P34 MARINA BAY CONTENTS 05 TIPS 26 CHINATOWN ORCHARD 06 ROAD 30 SENTOSA KAMPONG MARINA BAY & MAP OF SEVEN 10 GLAM 34 ESPLANADE NEIGHBOURHOODS This Muslim-friendly guide to the seven main LITTLE TRAVEL P30 SENTOSA neighbourhoods around 18 INDIA 38 ITINERARIES Singapore helps you make the best of your stay. TIONG HALAL RESTAURANT 22 BAHRU 42 DIRECTORY Tourism Court This guide was developed with inputs from writers Nur Safiah 1 Orchard Spring Lane Alias and Suffian Hakim, as well as CrescentRating, a leading Singapore 247729 authority on Halal travel. -

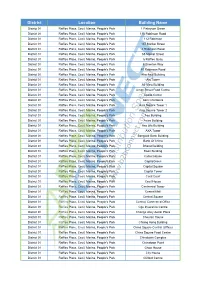

District Location Building Name

District Location Building Name District 01 Raffles Place, Cecil, Marina, People's Park 1 Finlayson Green District 01 Raffles Place, Cecil, Marina, People's Park 110 Robinson Road District 01 Raffles Place, Cecil, Marina, People's Park 112 Robinson District 01 Raffles Place, Cecil, Marina, People's Park 137 Market Street District 01 Raffles Place, Cecil, Marina, People's Park 4 Robinson Road District 01 Raffles Place, Cecil, Marina, People's Park 55 Market Street District 01 Raffles Place, Cecil, Marina, People's Park 6 Raffles Quay District 01 Raffles Place, Cecil, Marina, People's Park 6 Shenton Way District 01 Raffles Place, Cecil, Marina, People's Park 80 Robinson Road District 01 Raffles Place, Cecil, Marina, People's Park Afro-Asia Building District 01 Raffles Place, Cecil, Marina, People's Park Aia Tower District 01 Raffles Place, Cecil, Marina, People's Park Air View Building District 01 Raffles Place, Cecil, Marina, People's Park Amoy Street Food Centre District 01 Raffles Place, Cecil, Marina, People's Park Apollo Center District 01 Raffles Place, Cecil, Marina, People's Park Asia Chambers District 01 Raffles Place, Cecil, Marina, People's Park Asia Square Tower 1 District 01 Raffles Place, Cecil, Marina, People's Park Asia Square Tower 2 District 01 Raffles Place, Cecil, Marina, People's Park Aso Building District 01 Raffles Place, Cecil, Marina, People's Park Aviva Building District 01 Raffles Place, Cecil, Marina, People's Park Axa Life Building District 01 Raffles Place, Cecil, Marina, People's Park AXA Tower District 01 -

2.-Hi-Life-March-2014-Issue-2.Pdf

Hi Life! March 2014 (Issue 2) A Hong Leong Group e-newsletter March 2014 (Issue 2) HIGHLIGHTS Libra Fridge Clinches Merit Award Galloping Around The World Chairman Kwek Clinches REDAS at Design For Asia Award Into The Year Of The Horse Lifetime Achievement Award Millennium Resort Hangzhou: CDL Management Changes Acquisition Puts M&C Our First China Resort On Road To Rome PLUS! • Getting To Know Kwek Leng Beng • The St. Regis Singapore’s Receptionist Gwendolyn Chia Wins International Receptionist We want to hear from you! Of The Year Tell us about your projects, executive • Indulge In A Relaxing Hot Spring At Millennium appointments, awards and accolades, latest Hotel Wuxi promotions, charity and community outreach programmes, etc. • CDL Listed As One Of The Global 100 Most Sustainable Corporations In The World For Fifth If you have interesting photos to go along Year Running with them, all the better! • Ringing In The New Year With A Countdown At Email your stories and pictures to Group Orchard Hotel Singapore Corporate Affairs at [email protected] • Holiday Choices That Create Happy Memories ...and more in this issue of Hi Life! file:///C|/Users/jefferylim/Downloads/feb_2014/pdf.html[11/3/2014 10:09:51 AM] Hi Life! March 2014 (Issue 2) Galloping Around The World Into The Year Of The Horse The Chinese Lunar New Year marks a time of celebration and prosperity. That’s what some of the members of the Hong Leong Group did to celebrate this auspicious event. Here’s we present some of the highlights as we gallop into the year of the horse: The formatting for this photo is still not correct, can help try to rearrange it so the comes to the top of the photo? In Singapore: In Xiamen, China: Guests enjoying the breathtaking lion dance performance at a Chinese Staff at Millennium Hotel Harbourview Xiamen pose with Cai Shen Ye, the New Year lunch at The St. -

Singapore Office Market Review

Q2 2021 Published 8 April 2021 Singapore Office Market Review DEMAND Pg 3 SUPPLY Pg 4 Special Feature: Guoco Midtown Pg 6 New Developments: B1/2 Category Pg 7 Rentals Forecasts Top prime rates for premium Grade A buildings have softened from a • Market still dominated by tech firms and the financial services high of $14.00 per sq ft a year ago, to around $11.50 - $12.00 per sq ft. / investment sector, as well as displaced tenants looking for new Average prime rates in the Raffles Place area are in the region of office premises. $9.50 per sq ft. Office rates in theRobinson Road / Shenton Way area are in the $7.00 - $8.50 per sq ft bracket. • Demand for co-working space to continue with hybrid solutions proving popular. There is not much difference in the rental costs for Tanjong Pagar, which averages around $7.50 per sq ft. City Hall ranges from $7.00 to • Ample choice of supply at the moment and the amount of shadow $9.00 per sq ft and Beach Road averages around $7.25 per sq ft. space is increasing, due to companies rightsizing. There has been little movement on Orchard Road, and as such this • Supply will begin to tighten later in the year. location still enjoys a relatively high occupancy rate. Rents range from $7.50 to $9.50 per sq ft in this district. • Only two sizeable office developments due for completion this year in the CBD (CapitaSpring and Afro-Asia iMark). Edge of CBD like Novena, River Valley Road and decentralized locations like Harbourfront Centre and Paya Lebar Square range from • Rates to soften by 7% across the board, but rate of decline will $6.00 to $7.00 per sq ft. -

Swedish and Swedish Related Companies in Singapore COMPANY ADDRESS ADDRESS COUNTRY POSTAL HOME PAGE

Swedish and swedish related companies in Singapore COMPANY ADDRESS ADDRESS COUNTRY POSTAL HOME PAGE ABB Pte Ltd 2 Ayer Rajah Crescent Singapore 139935 www.abb.com.sg Absortech Asia Pacific Pte Ltd 2 Soon Wing Road #07-12 Singapore 347893 www.absortech.com Accedo http://www.accedo.tv/company AdvanIDe Pte Ltd (Assa Abloy) 111 Somerset Road #05-08 Tripleone Somerset Singapore 238164 www.advanide.com Adxto Holding Pte. Ltd 321 Orchard Road #06-06 Orchard Shopping Centre Singapore 238866 www.adxto.com Akers Pacific Pte Ltd #03-01C Sime Darby Centre Singapore 589472 www.akersrolls.com Akzo Nobel Surface Chemistry Pte Ltd 40 Jurong Island Highway Singapore 627830 www.akzonobel.com Alfa Laval Singapore Pte Ltd 11 Joo Koon Circle Jurong Singapore 629043 www.alfalaval.sg/ Alimak Hek Pte. Ltd. 18 Boon Lay Way, Tradehub 21 #03-123/124/125 Singapore 609966 www.alimakhek.sg ANDA Pacific Pte Ltd 2 Queen Astrid Park Singapore 266794 Apples & Spears The HUB Singapore 128 Prinsep Street Singapore 188655 http://www.applesandspears.com/ Apply Emtunga AB http://www.emtunga.com APSIS 111 Somerset Road #16-06 TripleOne Somerset Singapore 238164 www.apsis.com Asian Tigers Mobility Pte Ltd 6 Lok Yang Way Jurong Singapore 628625 www.asiantigers-mobility.com/singapore Assa Abloy Pte Ltd 10 Arumugam Road #06-00 Lion Building A Singapore 409957 www.assaabloy.se ASSAB Pacific Pte Ltd 171 Chin Swee Road #07-02 Singapore 169877 www.assab.com ASSAB Steels Singapore (Pte) Ltd 18 Penjuru Close Singapore 608616 www.assab-singapore.com Atlas Copco (South East Asia) Pte Ltd -

Office Rental Guide Official Asking Rates

Office Rental Guide MYP Plaza $6.50 Singapore Pools Building Full OUE Downtown 1 & 2 $9.00 Sunshine Plaza $6.50 Official Asking Rates PIL Building $6.50 Tanglin Shopping Centre Full Robinson 77 $9.00 The Bencoolen $5.50 S$ per sq ft per month – Robinson 112 $6.80 The Heeren $10.50 inclusive of service charge Robinson Centre $10.50 Thong Teck Building $7.00-$8.00 Robinson Point $8.00-$8.50 Tong Building $9.00 1 July 2020 SBF Centre $8.50+ TripleOne Somerset $8.50-$8.80 SGX Centre 1 & 2 $9.50 Visioncrest Commercial $9.00 Raffles Place/New Downtown Shenton House TBC Wheelock Place $11.50 6 Battery Road $14.00 SIF Building Full Wilkie Edge $9.00 6 Raffles Quay $7.00+ The Globe $7.00 Winsland House I & II $9.50 18 Robinson $12.00 The Octagon $5.80 Wisma Atria $9.80-$11.00 20 Collyer Quay $9.00-$13.00 Tokio Marine Centre Full 30 Raffles Place $11.00 Tong Eng Building $5.60+ Chinatown/River Valley Road 55 Market Street $10.50 UIC Building Full Central Mall $7.00 AIA Tower Full CES Centre $5.80 Asia Square Tower 1 $14.00+ Tanjong Pagar Chinatown Point $6.20-$8.00 Asia Square Tower 2 $13.50 78 Shenton Way Tower 1 $7.00-$8.20 Great World City $7.50 ASO Building $6.20 79 Shenton Way Tower 2 $9.20 Havelock II $7.50 Bank of China Building Full 79 Anson Road $8.50 King’s Centre $6.50 Bank of Singapore Centre $11.00 100AM $7.30-$8.30 The Central $8.80+ Bharat Building $6.30 ABI Plaza Full UE Square $8.50 CapitaGreen $13.50 Anson Centre $4.50 Valley Point $6.50 CapitaSpring TBC Anson House $9.00 Capital Square $11.50 AXA Tower $8.80 Edge of CBD Clifford -

Raffles Place Information Kit

Raffles Place Information Kit Version 2.0 November 2014 1 Table of Content Table of Content Page A. General - Table of Content 2 - System map 3 B. Station Information - Station Contacts & Overview 4 - Taxi & General Contacts 5 - Station Layout 6-10 - Locality Map 11 - Bus Services (By Bus Stop) 12 - Places of Interest 13-14 - Train Service Disruption Leaflet 15-17 2 3 Station Overview Station Contact Points Duty SM Hand phone 9663 4982 Passenger Service Center 6767 3301 EXIT: Exit A: Raffles Square Exit F: Cecil Street Exit B: Raffles Square Exit G: UOB Plaza Exit C: Ocean Financial Exit H: Chartered Bank Centre (Shopping Level) Building Exit D: Republic Plaza Exit I: AIA Tower Exit E: Ocean Financial Exit J: Marina Link Mall Centre (Street Level) LIFT: Lift 1: Remote Fare Gate Lift 2: Paid Area PLATFORM Upper Platform: - East Bound (towards Pasir Ris) : Line 1 – Platform A - North Bound (towards Jurong East): Line 4 – Platform B Lower Platform: - West Bound (towards Joo Koon): Line 2– Platform C - South Bound (towards Marina Bay / Marina South Pier): Line 5– Platform D 4 Taxi & General Contacts Nearby Taxi Stand Road Via Singapore Land Tower Battery Road Exit B Taxi Services Booking number SMRT Taxis 6555 8888 Comfort & City Cab 6552 1111 Trans Cab 6555 3333 Premier Taxis 6363 6888 Hotline Contact SMRT Hotline 1800 3368 900 SMRT Press Contact 9822 0902 TransitLink Hotline 1800 2255 663 Transcom Hotline 1800 8420 000 SMRT Online Feedback: www.smrt.com.sg/feedback.aspx 5 3. Notices and manpower deployment at Concourse RAFFLES PLACE GTM S TSO Concourse Free Area S S Wide Gate S S S S S S S S Service S S SHOP Gate PSC S Concourse Paid Area LEGEND 6 Escalator Planter Info Booth – Station staff - CST member Route from concourse (free area) to platform level via the wide gate & service gate 6 3. -

Capitaland Limited S$1,000,000,000 2.95 Per Cent

CapitaLand Limited S$1,000,000,000 2.95 per cent. CapitaLand Limited (Incorporated in the Republic of Singapore) Company Registration Number 198900036N S$1,000,000,000 2.95 per cent. Convertible Bonds due 2022 Issue price: 100 per cent. The S$1,000,000,000 2.95 per cent. Convertible Bonds due 2022 (the “Bonds”) will be issued by CapitaLand Limited (the “Issuer” or “CapitaLand”). Interest on the Bonds will be payable semi-annually in arrear on the interest payment dates falling on 20 June and 20 December of each year (each an “Interest Payment Date”). The first interest payment will be made on 20 December 2007. The Bonds are convertible by holders into ordinary shares of the Issuer (the “Shares”) at any time on or after 20 June 2008 and prior to the close of business (at the place the Bond is deposited for conversion) on 10 June 2022, unless previously redeemed, converted, or purchased and cancelled and except during a Closed Period (as defined herein). The conversion price (subject to adjustment in the manner provided herein) (the “Conversion Price”) will initially be S$13.8871 per Share. The Shares are listed on the Singapore Exchange Securities Trading Limited (the “SGX-ST”) and application has been made for the listing of the Shares to be issued on conversion of the Bonds on the SGX-ST. On 15 June 2007, the closing price of the Shares on the SGX-ST was S$8.10 per Share. See “Terms and Conditions of the Bonds — Conversion” and “Information Concerning the Shares”.