Hochschild Mining Plc

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

COVID-19 Proxy Governance Update

COVID-19 Proxy Governance Update 2020 AGM mid-season review FROM EQUINITI 01 Looking back and planning ahead It is incredible to note that it has been over 12 weeks since the official announcement on 23 March of the UK Government’s Stay at Home Measures, and nearly seven months since the severity of the pandemic became apparent in China. Over the said period, PLC boards, company secretaries and investor relations officers have kept their corporate calendars going thanks to rapid adoption of modified regulatory guidelines and inventive modes of engagement with investors. With annual general meetings being an obvious highlight in the corporate calendar, we take stock of the progress made so far over the 2020 AGM season, as well as using what we learned to plan ahead. Now that we are over the first ‘hump’ with the busy period of May AGMs out of the way, we are readying for the second ‘peak’ of June and July AGMs, and then an ‘easing’ until the second ‘mini’ season in the early autumn. As such, in this update, we look at: • 2020 AGM season statistics…so far • Proxy adviser engagement and ISS recommendations review • High-level assumptions for Q3 and Q4 • Relevant updates from the regulators, industry bodies and proxy advisers • Communications in the COVID-19 world – special commentary by leading financial PR firm,Camarco • How has COVID-19 impacted activism – special commentary by international law firm,White & Case 02 2020 AGM Season Statistics…so far Scope of data To assess progress and forecast what is to come, we look at the key statistics for the UK AGM season 2020 thus far. -

2019 Sustainability Report

SUSTAINABILITY REPORT OUR PURPOSE REFLECTS OUR COMMITMENT TO RESPONSIBILITY Hochschild is defined by its approach to responsible and innovative mining committed to a better world. 40% REDUCTION IN ACCIDENT FREQUENCY INDEX (OR LTIFR) (2019: 1.05 – 2018: 1.74) $9.3m AMOUNT SPENT OR DONATED TO BENEFIT LOCAL COMMUNITIES (2018: $8.3m) OUR AREAS OF FOCUS Safety PAGE 42 Health & Hygiene PAGE 44 Our people PAGE 45 Our communities PAGE 47 Environmental management PAGE 48 40 Hochschild Mining PLC / Annual Report & Accounts 2019 STRATEGIC REPORT STRATEGIC DEAR SHAREHOLDER programmes and initiatives during 2019 Our people has brought about impressive year-on- Hochschild would not be able to achieve year reductions in the accident frequency its current successes without its people index and accident severity rates of 40% and, in this report, we have set out how and 94% respectively. These results are the Group’s Human Resources (“HR”) testament to the efforts of all involved, team have contributed to strengthening and I can assure you of our commitment employee relations. I would like to to continue on this path as we proceed to highlight two aspects in particular. Firstly, roll out the action plan for the current year, the Attributes’ Weeks where employees GOVERNANCE known as “Safety 2.0”. across the Group participated in a week-long series of events that were Our communities thematically designed around a key value Our Community Relations team has which underlines our corporate purpose. had an equally active year. As part of our Secondly, the Gender Diversity project strategy of supporting projects targeting which was launched with the aim of education, health and socio-economic redressing the imbalance in the make-up development, we launched a new of our workforce, which is regrettably scholarship programme for young people representative of the sector. -

Parker Review

Ethnic Diversity Enriching Business Leadership An update report from The Parker Review Sir John Parker The Parker Review Committee 5 February 2020 Principal Sponsor Members of the Steering Committee Chair: Sir John Parker GBE, FREng Co-Chair: David Tyler Contents Members: Dr Doyin Atewologun Sanjay Bhandari Helen Mahy CBE Foreword by Sir John Parker 2 Sir Kenneth Olisa OBE Foreword by the Secretary of State 6 Trevor Phillips OBE Message from EY 8 Tom Shropshire Vision and Mission Statement 10 Yvonne Thompson CBE Professor Susan Vinnicombe CBE Current Profile of FTSE 350 Boards 14 Matthew Percival FRC/Cranfield Research on Ethnic Diversity Reporting 36 Arun Batra OBE Parker Review Recommendations 58 Bilal Raja Kirstie Wright Company Success Stories 62 Closing Word from Sir Jon Thompson 65 Observers Biographies 66 Sanu de Lima, Itiola Durojaiye, Katie Leinweber Appendix — The Directors’ Resource Toolkit 72 Department for Business, Energy & Industrial Strategy Thanks to our contributors during the year and to this report Oliver Cover Alex Diggins Neil Golborne Orla Pettigrew Sonam Patel Zaheer Ahmad MBE Rachel Sadka Simon Feeke Key advisors and contributors to this report: Simon Manterfield Dr Manjari Prashar Dr Fatima Tresh Latika Shah ® At the heart of our success lies the performance 2. Recognising the changes and growing talent of our many great companies, many of them listed pool of ethnically diverse candidates in our in the FTSE 100 and FTSE 250. There is no doubt home and overseas markets which will influence that one reason we have been able to punch recruitment patterns for years to come above our weight as a medium-sized country is the talent and inventiveness of our business leaders Whilst we have made great strides in bringing and our skilled people. -

FT UK 500 2011 A-Z Company UK Rank 2011 3I Group 94 888 Holdings 485 Abcam 250 Aberdeen Asset Management 109 Admiral Group 72 A

FT UK 500 2011 A-Z UK rank Company 2011 3I Group 94 888 Holdings 485 Abcam 250 Aberdeen Asset Management 109 Admiral Group 72 Advanced Medical Solutions 488 Aegis Group 127 Afren 138 African Barrick Gold 118 African Minerals 131 Aggreko 69 Albemarle & Bond 460 Allied Gold 306 Amec 75 Amerisur Resources 426 Amlin 124 Anglo American 11 Anglo Pacific Group 327 Anglo-Eastern Plantations 370 Anite 445 Antofagasta 29 Aquarius Platinum 136 Archipelago Resources 346 Arm Holdings 42 Ashley (Laura) 476 Ashmore 112 Ashtead Group 206 Asian Citrus 263 Asos 171 Associated British Foods 41 Assura 449 Astrazeneca 12 Atkins (WS) 240 Aurelian Oil & Gas 334 Autonomy 76 Avanti Communications 324 Aveva 192 Avis Europe 326 Aviva 31 Avocet Mining 287 Axis-Shield 469 AZ Electronic Materials 199 Babcock International 117 Bae Systems 35 Bahamas Petroleum 397 Balfour Beatty 111 Barclays 16 Barr (AG) 289 Barratt Developments 197 BBA Aviation 209 Beazley 257 Bellway 216 Bellzone Mining 292 Berendsen 222 Berkeley 160 Betfair Group 202 BG Group 8 BHP Billiton 7 Big Yellow Group 308 Blinkx 344 Bodycote 259 Booker 213 Boot (Henry) 478 Borders & Southern Petroleum 378 Bovis Homes Group 268 Bowleven 220 BP 4 Brammer 351 Brewin Dolphin 319 British American Tobacco 9 British Land 61 British Sky Broadcasting 27 Britvic 210 Brown (N) 237 BT Group 28 BTG 235 Bunzl 107 Burberry 59 Bwin Party Digital Entertainment 223 Cable & Wireless Communications 181 Cable & Wireless Worldwide 158 Cairn Energy 49 Caledon Resources 380 Camellia 389 Cape 270 Capita 66 Capital & Counties Properties -

Description Holding Book Cost Market Price Market Value £000'S £000'S

DORSET COUNTY PENSION FUND VALUATION OF PORTFOLIO AT CLOSE OF BUSINESS 31 March 2017 Book Market Description Holding Market Value Cost Price £000's £000's UK EQUITIES MINING ACACIA MINING 33,000 147.93 4.502 148.57 ANGLO AMERICAN ORD USD0.54 270,390 2,804.18 12.27 3,317.69 ANTOFAGASTA ORD GBP0.05 74,500 151.50 8.355 622.45 BHP BILLITON ORD USD0.50 436,926 2,401.54 12.395 5,415.70 CENTAMIN EGYPT LTD 226,000 349.07 1.732 391.43 FRESNILLO 35,500 88.20 15.52 550.96 GLENCORE XSTRATA 2,412,543 5,662.91 3.141 7,577.80 HOCHSCHILD MINING ORD GBP0.25 49,000 108.90 2.765 135.49 KAZ MINERALS 53,600 89.80 4.551 243.93 PETRA DIAMONDS 106,900 169.67 1.329 142.07 POLYMETAL INT'L 53,800 514.30 9.945 535.04 RANDGOLD RESOURCES ORD USD0.05 19,250 485.32 69.7 1,341.73 RIO TINTO ORD GBP0.10 (REG) 250,150 2,876.49 32.185 8,051.08 VEDANTA RESOURCES ORD USD0.10 18,500 75.07 8.11 150.04 Total MINING 15,924.89 28,524.69 OIL & GAS PRODUCERS AFREN PLC 218,000 215.93 0 0.00 BP ORD USD0.25 3,948,100 13,177.95 4.5885 18,115.86 CAIRN ENERGY ORD GBP0.06153846153 119,207 236.32 2.048 244.14 NOSTRUM OIL & GAS 17,700 84.36 4.796 84.89 ROYAL DUTCH 'B' ORD EUR0.07 1,642,961 20,190.09 21.945 36,054.78 TULLOW OIL ORD GBP 0.10 188,500 789.92 1.99026 375.16 Total OIL & GAS PRODUCERS 34,694.58 54,658.45 CHEMICALS CRODA INTL ORD GBP0.10 26,995 211.15 35.77 965.61 ELEMENTIS 99,000 130.23 2.899 287.00 JOHNSON MATTHEY ORD GBP1.00 40,357 446.31 30.82 1,243.80 SYNTHOMER 57,665 118.87 4.751 273.97 VICTREX ORD GBP0.01 17,000 111.61 19.02 323.34 Total CHEMICALS 1,018.16 3,087.91 CONSTRUCTION -

21 August 2008 Hochschild Mining Acquires 50% of Liam

________________________________________________________________________ 21 August 2008 Hochschild Mining acquires 50% of Liam Regional Joint Venture Hochschild Mining plc (“Hochschild”) is pleased to announce that it has consolidated its position in southern Peru through the acquisition of a 282,000 hectare land package in southern Peru, in very close proximity to Hochschild’s four existing operations; Arcata, Ares, Selene and Pallancata. Hochschild acquired a 50% interest in the Liam Regional Joint Venture (“Liam JV”) from Newmont Peru SRL and Newmont Mining Peru Limited, both subsidiaries of Newmont Mining Corporation, for a total cash consideration of $33.3 million. The transaction closed on 20 August 2008 and was funded entirely through existing cash. The Liam JV enables the Group to leverage its existing infrastructure and knowledge of the regional geology. Hochschild will be the operator in a joint venture with Southwestern Resources Corp., a Vancouver based mineral exploration company. The Liam JV consists of over 282,000 hectares in the Tertiary Volcanic Belt of southern Peru, a region with significant mineral potential approximately 170 kilometres northwest of Arequipa. The acquisition has significant strategic importance for Hochschild and exemplifies its cluster consolidation strategy. It is currently one of the largest single claim blocks in Peru and is in close proximity to Hochschild’s four existing operations; Arcata, Ares, Selene and Pallancata. Under the terms of the Liam JV agreement, Hochschild and Southwestern Resources Corp. will each contribute 50% of the exploration funding. In addition, Hochschild can earn a 70% interest in each designated property within the project by producing a positive feasibility study and financing 100% of the costs to commercial production. -

FTSE Russell Publications

2 FTSE Russell Publications 19 August 2021 FTSE 250 Indicative Index Weight Data as at Closing on 30 June 2021 Index weight Index weight Index weight Constituent Country Constituent Country Constituent Country (%) (%) (%) 3i Infrastructure 0.43 UNITED Bytes Technology Group 0.23 UNITED Edinburgh Investment Trust 0.25 UNITED KINGDOM KINGDOM KINGDOM 4imprint Group 0.18 UNITED C&C Group 0.23 UNITED Edinburgh Worldwide Inv Tst 0.35 UNITED KINGDOM KINGDOM KINGDOM 888 Holdings 0.25 UNITED Cairn Energy 0.17 UNITED Electrocomponents 1.18 UNITED KINGDOM KINGDOM KINGDOM Aberforth Smaller Companies Tst 0.33 UNITED Caledonia Investments 0.25 UNITED Elementis 0.21 UNITED KINGDOM KINGDOM KINGDOM Aggreko 0.51 UNITED Capita 0.15 UNITED Energean 0.21 UNITED KINGDOM KINGDOM KINGDOM Airtel Africa 0.19 UNITED Capital & Counties Properties 0.29 UNITED Essentra 0.23 UNITED KINGDOM KINGDOM KINGDOM AJ Bell 0.31 UNITED Carnival 0.54 UNITED Euromoney Institutional Investor 0.26 UNITED KINGDOM KINGDOM KINGDOM Alliance Trust 0.77 UNITED Centamin 0.27 UNITED European Opportunities Trust 0.19 UNITED KINGDOM KINGDOM KINGDOM Allianz Technology Trust 0.31 UNITED Centrica 0.74 UNITED F&C Investment Trust 1.1 UNITED KINGDOM KINGDOM KINGDOM AO World 0.18 UNITED Chemring Group 0.2 UNITED FDM Group Holdings 0.21 UNITED KINGDOM KINGDOM KINGDOM Apax Global Alpha 0.17 UNITED Chrysalis Investments 0.33 UNITED Ferrexpo 0.3 UNITED KINGDOM KINGDOM KINGDOM Ascential 0.4 UNITED Cineworld Group 0.19 UNITED Fidelity China Special Situations 0.35 UNITED KINGDOM KINGDOM KINGDOM Ashmore -

ACXW Avantis International Small Cap Value

American Century Investments® Quarterly Portfolio Holdings Avantis® International Small Cap Value ETF (AVDV) May 28, 2021 Avantis International Small Cap Value ETF - Schedule of Investments MAY 28, 2021 (UNAUDITED) Shares/ Principal Amount ($) Value ($) COMMON STOCKS — 99.4% Australia — 8.0% Adairs Ltd. 64,691 233,414 Adbri Ltd. 444,216 1,141,164 Aeris Resources Ltd.(1) 238,800 31,179 Alkane Resources Ltd.(1)(2) 152,741 103,278 Alliance Aviation Services Ltd.(1) 50,306 171,065 Asaleo Care Ltd. 212,115 229,790 Aurelia Metals Ltd. 716,008 245,064 Austal Ltd. 283,491 520,718 Australian Finance Group Ltd. 186,297 400,567 Australian Pharmaceutical Industries Ltd. 419,111 373,258 Bank of Queensland Ltd. 555,800 3,869,929 Beach Energy Ltd. 2,204,143 2,167,414 Bendigo & Adelaide Bank Ltd. 252,445 2,042,517 Boral Ltd.(1) 116,988 619,401 Calix Ltd.(1) 39,671 84,060 Cedar Woods Properties Ltd. 8,294 45,011 Champion Iron Ltd.(1) 492,380 2,502,893 Collins Foods Ltd. 16,697 160,894 Coronado Global Resources, Inc.(1) 453,537 242,887 CSR Ltd. 651,143 2,799,491 Dacian Gold Ltd.(1) 129,467 28,363 Deterra Royalties Ltd. 179,435 579,460 Eclipx Group Ltd.(1) 432,641 710,525 Emeco Holdings Ltd.(1) 476,645 332,757 EML Payments Ltd.(1) 327,130 862,970 Galaxy Resources Ltd.(1) 3,318 9,808 Genworth Mortgage Insurance Australia Ltd.(1) 442,504 945,096 Gold Road Resources Ltd. 660,222 763,347 GrainCorp Ltd., A Shares 347,275 1,343,019 Grange Resources Ltd. -

Schroder Investment Management North America Inc

Schroder Investment Management North America Inc. Bay County Employees’ Retirement System Matthew Dobbs, Head of Global Small Cap Equities, Portfolio Manager Hannah Piper, Pan-European Small Cap Analyst June 2018 For professional advisers only. This material is not suitable for retail clients Investment Philosophy and Team Investment philosophy Philosophical beliefs Deduction Process Stock selection is key source of Inefficiency higher for small stocks Stock selection predominant value-added Small stocks have higher specific Seek quality and growth – at the Embedded in screens and in-house risks wrong price stock research Low liquidity an opportunity and a Seek long-term, not short-term Long-term time horizon challenge valuation anomalies Opportunity set is global Need for on the ground presence Extensive, dedicated global team The views and forecasts contained herein are those of the International Small Cap team and are subject to change. 2 Resources International small cap team – A fully resourced and focused team – 20 specialists in international small Lead Portfolio Manager company research Matthew Dobbs 36 (36) and investment – Core team of Lead Portfolio Japan Pacific x Jap Pan Europe Manager and Regional Specialists Small Cap Specialist Small Cap Specialist Small Cap Specialist have an average of 25 years Takuya Furutani 14 (23) Richard Sennitt2 24 (24) Jean Roche 2 (18) investment experience and an Paul Rathband 6 (26) Andrew Lynch 19 (19) average of 17 years tenure at Small Cap Analyst Small Cap Analyst Small Cap Analyst Schroders -

Trendrating Momentum Alpha United Kingdom (50) September 2020 Trendrating Momentum Alpha United Kingdom (50) Sep 01, 2020 Chart

Trendrating Momentum Alpha United Kingdom (50) September 2020 Trendrating Momentum Alpha United Kingdom (50) Sep 01, 2020 Chart Page 2 of 8 Trendrating Momentum Alpha United Kingdom (50) Sep 01, 2020 Key facts Performance Key ratios Trendrating Benchmark Difference Trendrating Benchmark Difference Cumulative +109.71% -9.18% +118.88% One way yearly 262% average turnover Annualized +13.46% -1.63% +15.09% Sharpe ratio 0.8080 -0.1763 +0.9843 Yearly average +14.93% -0.70% +15.63% Sterling ratio 0.8210 -0.1461 +0.9671 Max consecutive 7 5 +2 positive weeks Sortino ratio 1.5977 -0.3221 +1.9198 Beta 0.7964 Tracking error 0.1136 Risk Information ratio 0.4119 Trendrating Benchmark Difference Treynor ratio 0.3257 Max drawdown -36.54% -36.61% +0.07% % positive weeks 63.24% 57.35% +5.88% Average yearly -15.09% -15.40% +0.31% drawdown Monthly standard 4.36% 4.90% -0.54% deviation Max consecutive 4 3 +1 negative weeks Page 3 of 8 Trendrating Momentum Alpha United Kingdom (50) Sep 01, 2020 Analytics Historical statistics Yearly performance Max drawdown Monthly return stdDev One way turnover Year Trendrating Benchmark Added value Trendrating Benchmark Added value Trendrating Benchmark Added value 2015 20.15% -4.93% 25.08% -8.08% -17.31% 9.23% 3.83% 4.90% 1.06% 44.16% 2016 13.55% 14.43% -0.88% -13.31% -11.30% -2.01% 4.81% 4.77% -0.04% 95.22% 2017 38.34% 7.63% 30.71% -4.48% -4.40% -0.08% 2.75% 2.43% -0.33% 37.01% 2018 -11.91% -12.48% 0.57% -20.83% -16.41% -4.42% 3.88% 3.60% -0.28% 139.89% 2019 38.13% 12.10% 26.03% -7.30% -8.06% 0.76% 2.90% 3.33% 0.43% 90.36% -

Interim Results for the Six Months Ended 30 June 2013

___________________________________________________________________________ 21 August 2013 Hochschild Mining plc Interim Results for the six months ended 30 June 2013 H1 2013 Financial highlights1 Revenue of $308.6 million (H1 2012: $354.5 million) Adjusted EBITDA of $90.4 million (H1 2012: $168.4 million) Pre-exceptional EPS of $(0.10) (H1 2012: $0.08) which includes $15.4 million ($0.05 per share) foreign exchange loss on cash deposits in Peru - more than offset by positive effects on unit costs and capital expenditure Exceptional items of $(13.2) million include: o $45.9 million net gain resulting from reclassification of Gold Resource Corp holding from investment in associate to available-for-sale financial asset o $59.1 million of impairment charges and severance payments net of taxes2 Interim dividend suspended Strong balance sheet with total cash of approximately $275 million as at 31 July 2013 Minority investments valued at $103.8 million as at 31 July 2013 Undrawn $140 million loan facility to finance Inmaculada project Cashflow optimisation programme Implemented in H1 2013 - approximately $200 million of initiatives identified o Unit cost increases in Peru revised down to 0-5% for 2013 o Unit cost increase in Argentina revised down to 5-10% for 2013 o 2013 sustaining capex further lowered to $150 million from original 2013 guidance of $180 million o 2013 exploration budget further reduced to $50 million from original $77 million o 2013 administration expenses reduced by $20 million o Reduction in Board size, Directors’ -

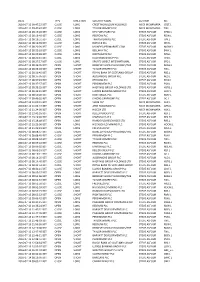

Date Type Direction Security Name Author Ric 2016-07-11

DATE TYPE DIRECTION SECURITY NAME AUTHOR RIC 2016-07-11 09:47:22 BST CLOSE LONG CREST NICHOLSON HOLDINGS MICK MCNAMARA CRST.L 2016-07-11 09:47:47 BST CLOSE LONG TAYLOR WIMPEY PLC MICK MCNAMARA TW.L 2016-07-12 08:19:26 BST CLOSE LONG DFS FURNITURE PLC STEVE ASFOUR DFSD.L 2016-07-12 08:19:40 BST CLOSE LONG REDROW PLC STEVE ASFOUR RDW.L 2016-07-12 08:19:51 BST CLOSE LONG TRAVIS PERKINS PLC STEVE ASFOUR TPK.L 2016-07-12 08:19:59 BST CLOSE LONG IBSTOCK PLC STEVE ASFOUR IBST.L 2016-07-12 08:20:09 BST CLOSE LONG MONEYSUPERMARKET.COM STEVE ASFOUR MONY.L 2016-07-12 08:20:18 BST CLOSE LONG BELLWAY PLC STEVE ASFOUR BWY.L 2016-07-12 08:20:28 BST CLOSE LONG NORTHGATE PLC STEVE ASFOUR NTG.L 2016-07-12 08:20:41 BST CLOSE LONG HALFORDS GROUP PLC STEVE ASFOUR HFD.L 2016-07-12 08:27:17 BST CLOSE LONG SPORTS DIRECT INTERNATIONAL STEVE ASFOUR SPD.L 2016-07-12 08:36:05 BST OPEN SHORT BERKELEY GROUP HOLDINGS/THE STEVE ASFOUR BKGH.L 2016-07-12 08:36:28 BST OPEN SHORT TAYLOR WIMPEY PLC STEVE ASFOUR TW.L 2016-07-12 08:36:45 BST OPEN SHORT ROYAL BANK OF SCOTLAND GROUP STEVE ASFOUR RBS.L 2016-07-12 08:37:05 BST OPEN SHORT ALDERMORE GROUP PLC STEVE ASFOUR ALD.L 2016-07-12 08:37:43 BST OPEN SHORT REDROW PLC STEVE ASFOUR RDW.L 2016-07-12 08:37:57 BST OPEN SHORT PERSIMMON PLC STEVE ASFOUR PSN.L 2016-07-12 08:38:25 BST OPEN SHORT HASTINGS GROUP HOLDINGS LTD STEVE ASFOUR HSTG.L 2016-07-12 08:42:41 BST OPEN SHORT LLOYDS BANKING GROUP PLC STEVE ASFOUR LLOY.L 2016-07-12 08:50:28 BST OPEN SHORT RIGHTMOVE PLC STEVE ASFOUR RMV.L 2016-07-12 09:49:35 BST OPEN SHORT DIXONS CARPHONE