The Intelligent Investor

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

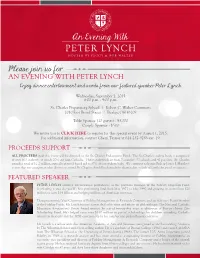

Please Join Us for an EVENING with PETER LYNCH Enjoy Dinner, Entertainment and Words from Our Featured Speaker, Peter Lynch

Please join us for AN EVENING WITH PETER LYNCH Enjoy dinner, entertainment and words from our featured speaker, Peter Lynch. Wednesday, September 2, 2015 6:00 p.m. - 9:00 p.m. St. Charles Preparatory School | Robert C. Walter Commons 2010 East Broad Street | Bexley, OH 43209 Table Sponsor (10 guests) - $5,000 Couple Sponsor - $500 We invite you to CLICK HERE to register for this special event by August 1, 2015. For additional information, contact Cherri Taynor at 614-252-9288 ext. 19. PROCEEDS SUPPORT ALL PROCEEDS from this event will be directed to the St. Charles Endowment Fund. The St. Charles student body is comprised of over 600 students, of which 20% are non-Catholic. These students draw from 7 counties, 53 schools and 42 parishes. St. Charles awards a total of $1.2 million annually in need-based aid to 37% of our student body. We continue to honor Bishop James J. Hartley’s vision that no young man who desires to attend St. Charles should be denied the chance due to lack of family financial resources. FEATURED SPEAKER PETER LYNCH attained international prominence as the portfolio manager of the Fidelity Magellan Fund, developing it into the world’s best performing fund from May 1977 to May 1990 and growing its assets from $20 million to over $14 billion and helping millions of American investors. Though currently Vice Chairman of Fidelity Management & Research Company and an Advisory Board Member of the Fidelity Funds, Mr. Lynch focuses a great deal of his time and efforts on philanthropy. The National Catholic Education Association’s Seton Award winner, he served twenty-five years as chairman of Boston’s Inner City Scholarship Fund. -

The Mecca of Value Investing

The mecca of Value Investing Subject: The mecca of Value Invesng From: CSH Investments <[email protected]> Date: 6/18/2019, 1:44 PM To: Randy <[email protected]> View this email in your browser Some of you know I'm a big believer in lifetime learning. It wasn't always the case. My early academic years were less than stellar. But I caught on fairly quickly and made do. By my late 20's I knew I wanted to be in finance. I had studied finance and economics in college but it didn't really grab me. Looking back partly it was me but also it was the way it was taught. Stodgy old theories that really didn't make any sense to me. The Efficient Market Theory for instance. EMT says basically that the markets are fully efficient. That stocks are perfectly priced therefore there aren't any bargains. You have absolutely nothing to gain from fundamental analysis and if you do it you are wasting your time. Yeah I thought but I knew there were guys who did exactly that. They did 1 of 5 6/18/2019, 4:48 PM The mecca of Value Investing their own research and found things that were mispriced. Most of them were quite wealthy. If the market is perfectly efficient as you say then how can they do it? And almost every theory had a list of assumptions you had to make. Here's one I love, every investor has the same information. Well, let's just be logical every investor doesn't have the same information and even if they did they would interpret differently. -

The Intelligent Investor

THE INTELLIGENT INVESTOR A BOOK OF PRACTICAL COUNSEL REVISED EDITION BENJAMIN GRAHAM Updated with New Commentary by Jason Zweig An e-book excerpt from To E.M.G. Through chances various, through all vicissitudes, we make our way.... Aeneid Contents Epigraph iii Preface to the Fourth Edition, by Warren E. Buffett viii ANote About Benjamin Graham, by Jason Zweigx Introduction: What This Book Expects to Accomplish 1 COMMENTARY ON THE INTRODUCTION 12 1. Investment versus Speculation: Results to Be Expected by the Intelligent Investor 18 COMMENTARY ON CHAPTER 1 35 2. The Investor and Inflation 47 COMMENTARY ON CHAPTER 2 58 3. A Century of Stock-Market History: The Level of Stock Prices in Early 1972 65 COMMENTARY ON CHAPTER 3 80 4. General Portfolio Policy: The Defensive Investor 88 COMMENTARY ON CHAPTER 4 101 5. The Defensive Investor and Common Stocks 112 COMMENTARY ON CHAPTER 5 124 6. Portfolio Policy for the Enterprising Investor: Negative Approach 133 COMMENTARY ON CHAPTER 6 145 7. Portfolio Policy for the Enterprising Investor: The Positive Side 155 COMMENTARY ON CHAPTER 7 179 8. The Investor and Market Fluctuations 188 iv v Contents COMMENTARY ON CHAPTER 8 213 9. Investing in Investment Funds 226 COMMENTARY ON CHAPTER 9 242 10. The Investor and His Advisers 257 COMMENTARY ON CHAPTER 10 272 11. Security Analysis for the Lay Investor: General Approach 280 COMMENTARY ON CHAPTER 11 302 12. Things to Consider About Per-Share Earnings 310 COMMENTARY ON CHAPTER 12 322 13. A Comparison of Four Listed Companies 330 COMMENTARY ON CHAPTER 13 339 14. -

Benjamin Graham: the Father of Financial Analysis

BENJAMIN GRAHAM THE FATHER OF FINANCIAL ANALYSIS Irving Kahn, C.F.A. and Robert D. M£lne, G.F.A. Occasional Paper Number 5 THE FINANCIAL ANALYSTS RESEARCH FOUNDATION Copyright © 1977 by The Financial Analysts Research Foundation Charlottesville, Virginia 10-digit ISBN: 1-934667-05-6 13-digit ISBN: 978-1-934667-05-7 CONTENTS Dedication • VIlI About the Authors • IX 1. Biographical Sketch of Benjamin Graham, Financial Analyst 1 II. Some Reflections on Ben Graham's Personality 31 III. An Hour with Mr. Graham, March 1976 33 IV. Benjamin Graham as a Portfolio Manager 42 V. Quotations from Benjamin Graham 47 VI. Selected Bibliography 49 ******* The authors wish to thank The Institute of Chartered Financial Analysts staff, including Mary Davis Shelton and Ralph F. MacDonald, III, in preparing this manuscript for publication. v THE FINANCIAL ANALYSTS RESEARCH FOUNDATION AND ITS PUBLICATIONS 1. The Financial Analysts Research Foundation is an autonomous charitable foundation, as defined by Section 501 (c)(3) of the Internal Revenue Code. The Foundation seeks to improve the professional performance of financial analysts by fostering education, by stimulating the development of financial analysis through high quality research, and by facilitating the dissemination of such research to users and to the public. More specifically, the purposes and obligations of the Foundation are to commission basic studies (1) with respect to investment securities analysis, investment management, financial analysis, securities markets and closely related areas that are not presently or adequately covered by the available literature, (2) that are directed toward the practical needs of the financial analyst and the portfolio manager, and (3) that are of some enduring value. -

The Intelligent Investor: the Definitive Book on Value Investing. a Book of Practical Counsel by Benjamin Graham and Jason Zweig

The Intelligent Investor: The Definitive Book on Value Investing. A Book of Practical Counsel by Benjamin Graham and Jason Zweig Security Analysis: Sixth Edition, Foreword by Warren Buffett by Benjamin Graham and David Dodd Contrarian Investment Strategies: The Psychological Edge by David Dreman Margin of Safety: Risk-Averse Value Investing Strategies for the Thoughtful Investor by Seth A. Klarman What Has Worked In Investing: Studies of Investment Approaches and Characteristics Associated with Exceptional Returns by Tweedy, Browne Company LLC Value Investing: From Graham to Buffett and Beyond by Bruce C. N. Greenwald and Judd Kahn The Little Book That Builds Wealth: The Knockout Formula for Finding Great Investments by Pat Dorsey The Five Rules for Successful Stock Investing: Morningstar's Guide to Building Wealth and Winning in the Market by Pat Dorsey Common Stocks and Uncommon Profits and Other Writings by Philip A. Fisher The Investment Checklist: The Art of In-Depth Research by Michael Shearn Financial Statements: A Step-by-Step Guide to Understanding and Creating Financial Reports by Thomas R. Ittelson Active Value Investing: Making Money in Range-Bound Markets by Vitaliy N. Katsenelson The Little Book of Sideways Markets: How to Make Money in Markets that Go Nowhere by Vitaliy N. Katsenelson The Art of Value Investing: How the World's Best Investors Beat the Market by John Heins and Whitney Tilson The Art of Short Selling Hardcover by Kathryn F. Staley The Most Important Thing Illuminated: Uncommon Sense for the Thoughtful Investor by Howard Marks and Paul Johnson Financial Shenanigans: How to Detect Accounting Gimmicks & Fraud in Financial Reports, 3rd Edition by Howard Schilit and Jeremy Perler Quality of Earnings by Thornton L. -

Our Firm and Fidelity. Working Together for You. Helping to Serve Your Best Interests

Our Firm and Fidelity. Working Together for You. Helping to serve your best interests. 31822.indd A 9/20/07 10:52:30 AM 331822.indd1822.indd B 99/12/07/12/07 11:56:14:56:14 PPMM A powerful combination As your financial advisor, we’re expected to make decisions about your money based on the highest degree of scrutiny. You can be assured that we use the same approach when choosing the service providers we employ to help meet your financial objectives. This is why we’ve selected Fidelity Investments as our custodian. What is a custodian? A custodian is a financial institution that has legal responsibility for a customer’s securities. Custodianship includes management as well as safekeeping, and this service incurs additional fees. Our firm, like all investment managers, is required to have a custodian. Investments that you entrust to our firm are placed in custody with Fidelity’s clearing firm, National Financial Services LLC (NFS) — one of the largest clearing providers in the industry. A clearing firm is an organization that works with financial exchanges to handle the confirmation, delivery, and settlement of transactions. When you’re selecting your financial advisor, it can be a critical factor to consider who your advisor uses to custody your investments, as this will help to determine the level of service, support, and protection that you can expect from your financial advisor. OUR FIRM AND FIDELITY 1 331822.indd1822.indd C 99/20/07/20/07 33:06:50:06:50 PPMM How does our relationship with Fidelity benefit you? An experienced, reputable firm helping to (SIPC). -

Ebook Download the Little Book of Stock Market Cycles Ebook Free Download

THE LITTLE BOOK OF STOCK MARKET CYCLES PDF, EPUB, EBOOK Jeffrey A. Hirsch,Douglas A. Kass | 240 pages | 07 Sep 2012 | John Wiley & Sons Inc | 9781118270110 | English | New York, United States The Little Book of Stock Market Cycles PDF Book KO , Lowe's Companies Inc. Fearing that they will lose all of their investment, they hastily sell their shares, often at a loss. The author of another great investment book, "Beating the Street," Peter Lynch's "One Up On Wall Street" is a go-to for investors who want to draw on their own common sense and knowledge to make smart investments. Investing in the Market. Morgan Stanley. In general, they believe that price increases and profit margin expansion are likely to decelerate, given a decline in commodity prices. We only partner with companies we believe offer the best products and services for small business owners. What method do you use to place your stop? Compare Accounts. One of the most common mistakes in stock market investing is trying to time the market. Receive full access to our market insights, commentary, newsletters, breaking news alerts, and more. Nicole Dieker Posts. The Stock Market and Your Life. The second type is the index tracking fund, which typically has lower costs and is more effective in matching the growth of the stock market. Financial Ratios. We sometimes make money from our advertising partners when a reader clicks on a link, fills out a form or application, or purchases a product or service. Her expertise is featured throughout Fit Small Business in personal finance , credit card , and real estate investing content. -

Learn from Investing Legends for 2020 & Beyond

Learn from Investing Legends for 2020 & Beyond Investors can learn a tremendous amount from studying philosophies and disclosed strategies of great investors. presented by Justin Carbonneau of Validea The Big Idea 163 Words Holding individual stocks remains a vital piece of long-term wealth creation. Sourcing and analyzing specific ideas, however, can be time-consuming, risky & complicated. With over 15,000 stocks, mutual funds and ETFs in the U.S. alone, you could spend a lifetime analyzing the set of investable ideas. In today's fast-paced world, many people lack the time to even sit down for dinner, so finding sound, efficient methods for stock analysis and idea generation is essential for today’s active stock investor. So, how do you effectively and systematically identify and research good opportunities? We believe proven, time-tested methodologies from legendary investors like Warren Buffett, Peter Lynch, Ben Graham and others with demonstrable approaches extracted from publicly disclosed writings provide a useful framework for sourcing and analyzing stocks that can play an important role in long-term wealth accumulation. The following presentation is dedicated to how we leverage and emulate these strategies to find sound investments ideas and what active investors like yourself can learn from them. Today’s Presentation • Opening insights from a legendary stock-picker; • Identification of the Gurus/Strategies; • Who are the Gurus/Strategies; • An overview of 5 different strategies – evidence, strategy & investment thesis behind each for today’s environment and the active fundamental investor; • Detailed investment methodologies & stock specific examples; • Key lessons and other tips to help the stock selection process; • Q&A Recent Thoughts on Stock-Picking from Market Master, Peter Lynch Barron’s, Dec. -

The Intelligent Investor: 100 Page Summary Ebook, Epub

THE INTELLIGENT INVESTOR: 100 PAGE SUMMARY PDF, EPUB, EBOOK Preston Pysh,Stig Brodersen | 108 pages | 19 Feb 2014 | 100 Page Summaries | 9781939370112 | English | United States The Intelligent Investor: 100 Page Summary PDF Book The truth is some will not live up to expectations. The outcome is definitely not desirable. To reach long-term success, every active investor has to evaluate each investment very carefully and above all diversify its portfolio among the most profitable industries. However, armed with this knowledge concerning the fallibility of mutual funds, the intelligent investor is better equipped to discern a more solid mutual fund from a more volatile one. However, some defensive investors do enjoy the intellectual challenge of picking some individual stocks. Fair to assume that outstandingly successful company has unusually good management. He said that if we pay special attention to those 2 chapters, we will not get a poor result from our investments. Go to Top. His principles of investing safely and successfully continue to influence investors today. He ended up being the professor for Warren Buffett. And I also wanted something that had that compared a stock to stock but it was also taking into account the risk appetite. Graham suggests 20 years. Always have a margin of safety. That way, you have to rely on your intuition. Ultimately, Graham states that the only thing an investor can be sure about when attempting to forecast future stock returns, is that they will probably turn out to be wrong. Or how much they should be saving to meet their financial goals. One is giving you double the return of the other, but you have a lot more risk associated with one versus the other. -

Notes from Security Analysis Sixth Edition Hardcover

Ronald R. Redfield CPA, PFS Notes to book “Security Analysis” 6th edition Written by: Benjamin Graham and David Dodd I thought these quotes from Security Analysis Sixth Edition Hardcover might be food for thought. Benjamin Graham and David Dodd first wrote security Analysis in 1934. The first edition was described by Graham as a “book that is intended for all those who have a serious interest in securities values.” The book was not designed for the investment novice. One must have an intermediate to advanced understanding of financial statements, accounting and finance for the book to be understood. The book emphasizes logical reasoning. Graham wrote, “It is the conservative investor who will need most of all to be reminded constantly of the lessons of 1931 –1933 and of previous collapses.” On Page [xiv] Seth Klarman wrote: ”Losing money, as Graham noted, can also be psychologically unsettling. Anxiety from the financial damage caused by recently experienced loss or the fear of further loss can significantly impede our ability to take advantage of the next opportunity that comes along. If an undervalued stock falls by half while the fundamentals – after checking and rechecking – are confirmed to be unchanged, we should relish the opportunity to buy significantly more “on sale.” But if our net worth has tumbled along with the share price, it may be psychologically difficult to add to the position.” On Page [xviii] Klarman wrote: ”Skepticism and judgment are always required.” “Because the value of a business depends on numerous variables, -

What Would Benjamin Graham Write Today?

What would Benjamin Graham write today? In a new foreword to the 1949 classic The“ Intelligent Investor“, by Benjamin Graham, noted investor John Bogle wrote a brilliant piece which investor would do well to read and re-read. He is as incisive as Ben Graham himself. “THE FIRST EDITION of The Intelligent Investor was published in 1949. It quickly became a classic, endorsed by Warren Buffett as “by far the best book on investing ever written.” Over the years, the slim 304 page initial edition was revised and expanded. By the fourth edition, published in 1973, it had grown to 340 pages. In that final edition, Benjamin Graham acknowledged that he was “greatly aided by my collaborator, Warren Buffett, whose counsel and practical aid have proved invaluable.” By curious coincidence, my own long investment career also began in 1949, when an articleFortune in magazine introduced me to the mutual fund industry. My first encounter with the Graham book didn’t take place until 1965, when I bought (for $5.95, new!) the third revised edition. There, Graham recognized the extraordinary changes that had taken place in the investment environment over the previous half century, yet took comfort in the fact that “through all its vicissitudes and casualties, as earthshaking as they were unforeseen, it remained true that sound investment principles produced generally sound results. We must act on the assumption that they will continue to do so.” As an eyewitness to the earthshaking vicissitudes and casualties ofthis past half century, coincident with the life of Graham’s investment classic, I’m honored to contribute this foreword, for it gives me the opportunity to reflect on my own experience with sound investment principles during thislong span. -

GEICO: the “Growth Company” That Made the “Value Investing” Careers of Both Benjamin Graham and Warren Buffett

GEICO: The “Growth Company” that made the “Value Investing” careers of both Benjamin Graham and Warren Buffett In 1948, we made our GEICO investment and from then on, we seemed to be very brilliant people. Benjamin Graham, 1976 Becky Quick (CNBC): “If you could keep one company that Berkshire owns, either a wholly- owned subsidiary, or that Berkshire owns a common equity in, which one would you keep and why?” Warren Buffett: “I would keep GEICO. It goes back to the -- 62 years ago it changed my life. It's also a wonderful company. I would have both things going for me, but that if I hadn't of gone to GEICO when I was 20 years-old and had a fellow there explain the insurance business to me, my life would be vastly different. So I just have to - - I'd have to choose GEICO.” CNBC interview March 13, 2013 Two of the greatest "Value" investors of all-time owe a substantial part of their wealth and public reputations – and deserved accolades - to a singular great “Growth” company, the Government Employees Insurance Company (GEICO). In the vernacular of investing, “Value” and “Growth” are most often associated with competing, mutually exclusive investing styles. It shouldn’t be so, but as a +30-year veteran in the investing “business” I can assure you that this investing-style division is deeply embedded in the investment management industry. Benjamin Graham’s deserved sobriquets include the “Father of Security Analysis” and the “Dean of Value Investing.” Of course Warren Buffett is known around the globe as the “Oracle of Omaha,” as well as Benjamin’s Graham’s greatest student.